Since it first appeared in late 2019, COVID-19 has caused an incomprehensible amount of suffering and disrupted lifestyles, work routines, and the global economy, including supply chains. Reflecting on the cascading effects of the pandemic, seven CFOs speak about how their use of technology and data analytics, as well as their views on risk management, have changed in the face of COVID-19 and how their company’s finance function and overall organization have had to adapt to overcome the various challenges presented by the shifting business landscape.

Given so much uncertainty, many C-suite executives report having a more intense focus on shorter-term plans. CFOs in particular place a renewed priority on variable costs. With the potential for sales and other types of revenue-generating activities to decrease, many finance executives stress the need to be nimble to ensure that their company can react to budget pressures and reduce costs as necessary.

“An outsize focus on team cohesiveness has modified the responsibilities of the CFO,” says Ron Oertell, CFO of Purchasing Power, an employee payroll-deduction purchase program provider. “With the subdued interaction between employees across company functions, as well as within each department, the CFO and all accounting and finance professionals need to ensure everyone is aligned on projects, budgets, goals, and deliverables.”

In the case of Trintech, a financial-close software provider, the finance team creates and distributes a series of financial models and reports on key performance indicators more frequently now. During the height of the pandemic, teams became accustomed to getting all that data, information, and insight to the point where it has now become expected whether there’s a pandemic or not.

“When the pandemic was initially declared, leadership teams were anxious and looked to near-real-time financial data to help them guide their company through a highly uncertain time—now they want to sustain that level of data insight to support ongoing planning and goal setting,” says Omar Choucair, CFO of Trintech.

“As the CFO of a SaaS [software-as-a-service] company working with internal accounting and finance teams, I know digital transformation is a huge part of meeting these needs,” he says. “To the extent that these companies have already invested in digital transformation of the back office, all that has made it much easier and more efficient to do.”

Quovant, a legal-spend-management service provider, was already processing many customer payments via automated clearing house (ACH) before the pandemic and paying many vendors by either corporate purchasing card or ACH. From a finance and accounting perspective, the company’s work in the past few years to move to cloud-based systems and technologies—such as enterprise risk management, customer relationship management, Zoom, and DocuSign—allowed Quovant’s finance team to make the necessary transitions relatively seamlessly.

“Simple things, such as getting the mail to the right staff to process transactions, have been a new burden for many finance teams,” says Scott Craighead, CFO of Quovant.

Planful, a cloud-based financial planning and analysis (FP&A) platform provider, implemented more one-on-one check-ins and virtual team meetings to foster a sense of community, even from a distance. Technology and automation have played an important part in ensuring its employees don’t feel overworked or burned out.

“By providing them with the right tools that make their lives easier, we’re prioritizing efficiency during a time when reporting has increased,” says Shane Hansen, CFO of Planful. “Finance teams quickly realized that they needed a cloud platform to do their work, including FP&A, in a remote environment if they wanted to operate in an agile manner.”

Pandemic-induced changes exposed the inefficiencies of some finance teams that relied on manual processes and outdated systems to complete their activities each month. Many organizations have considered adopting or ramping up automation, including robotic process automation (RPA).

“Finance teams with a high degree of automation and defined methods were able to adapt to this sudden change over the last year and continue to execute their responsibilities in a timely manner,” says Brandon Grinwis, CFO of Ascentis, a workforce management and HR software provider.

ADOPTION OF TECHNOLOGY

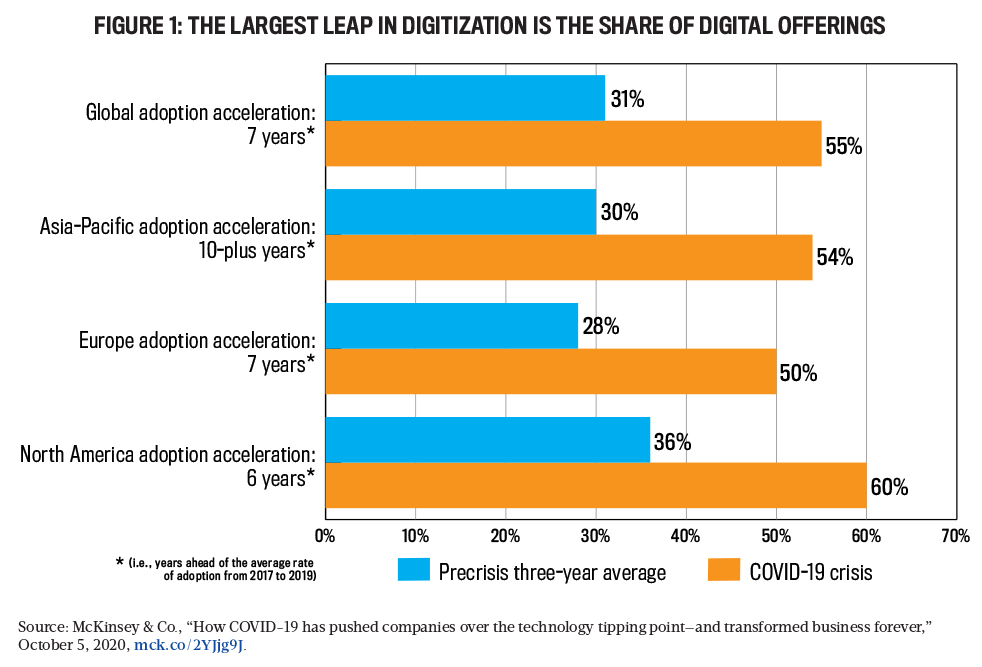

Software platforms enabling virtual communications such as Microsoft Teams, Skype, Zoom, Cisco Webex, and LogMeIn’s GoToMeeting have become an integral part of all companies’ basic workstream. And the pandemic has accelerated many companies’ adoption of other types of technology as well. See Figure 1 (Source: McKinsey & Co.) for an overview of global digitization trends.

Click to enlarge.

“The comms part is connecting with your team and making sure that we’ve got sufficient technology, whether it’s via applications or the internet,” says Choucair. “Given what we do in terms of automating the financial close in the cloud, we’ve already made that investment, and so we were well-equipped to do that.

“Now as we move into another new normal, with a sustained hybrid work model, we’ve continued to reassess our policies, procedures, and action plans, and the continued emphasis on cybersecurity, including cloud security, access controls, and phishing attempts, is a real big point for us,” he says.

Since executives at Bankers Healthcare Group (BHG), a financial services company specializing in loans, financing, and credit cards for healthcare professionals, have collaborated historically across three geographic locations, many of its personnel were already used to communicating over video. They found virtual meetings to be extremely productive.

“Adopting this across the company is something that wouldn’t have happened this quickly if we hadn’t already been utilizing it,” says Dan McSherry, CFO of BHG. “We were also able to invest in digital identity technology that allows us to complete fraud checks without being physically intrusive to the borrower.”

Apart from the ubiquitous videoconferencing, the biggest change is the focus on much faster product development, Oertell says. The pandemic has significantly increased the speed of new financial services and other products being offered to consumers and businesses as behaviors change and the significant amount of capital available from investors is allocated to product development.

“We estimate products are being developed and offered at two times the speed vs. prior to the pandemic,” Oertell says. “In turn, we have increased our investment in new product development in terms of priority, time, and money.”

Ephesoft, a document capture and processing platform provider, has been introducing newer relevant technologies to most aspects of running the business over the last few years, but the pandemic has accelerated its adoption of additional technologies within finance and other functional groups.

“We’re currently evaluating tools to accelerate accounting close, sales tax compliance, budgeting, and planning,” says Naren Goel, CFO of Ephesoft.

Many organizations’ adoption and usage of software have evolved significantly over the past several years. Before the pandemic, Quovant had employed cloud-based user activity monitoring software ActivTrak for a small subset of its employees who were already remote. The pandemic forced the company to move all employees to fully remote, so it implemented ActivTrak across the entire organization.

“This online tool has helped our managers ensure a greater understanding of where our staff is spending their time and if we can be helpful with workload balancing or giving them more insights on personal productivity,” Craighead says.

Manual processes are challenging when everyone is working remotely, and communication is limited to message chats and teleconference calls. Automation of processes allows organizations to mitigate risk by updating the systems and processes on which the business operates and provides information and tools necessary for the organization’s leaders to make sound business decisions. To be able to drive automation across its finance team sooner, Ascentis pulled forward some investment that was planned for 18 to 24 months into the future.

“We’ve also noticed this with our clients concerning their investment in a system for critical business functions such as workforce management and payroll,” Grinwis says. “Automation provides efficiencies but also creates a culture of compliance across the organization. And it’s much more effective to be proactive and take advantage of the opportunity to revamp systems and processes necessary for regulatory compliance, all while improving overall performance and visibility.”

SUPPLY CHAIN DISRUPTIONS

The pandemic forced CFOs to contend with the potential for a global event to impact their company’s entire business in a short amount of time. According to a survey from Proxima, 96% of finance leaders in the United States indicated that procurement was a significant part of their strategy in facing the challenges of the COVID-19 pandemic. Further, the large majority agreed that procurement will continue to play a relevant role for the recovery of their business this year and beyond (see Kent Mahoney, “Leverage Procurement to Build Resilience,” Strategic Finance, September 2021).

The pandemic’s global impact has caused CFOs to have several different scenarios that they update and monitor regularly. Shutdowns and labor constraints due to COVID-19 breakouts at factories and surrounding communities can suddenly alter timelines for parts and inventory.

“We meet with our vendors monthly to understand their situation, spending considerable time modeling different demand forecasts to understand our inventory needs and ways to mitigate potential risks,” Grinwis says.

If ever there were a time to reimagine supply chains, this era of backlogs is that moment. Contract manufacturing, also known as outsourced manufacturing, is one type of supply-chain link that takes many forms. CFOs and other finance executives must be ready to support their organization in outsourcing decisions (see John MacInnes, “Contract Manufacturing for OEM CFOs,” Strategic Finance, June 2021).

Purchasing Power’s leadership remains focused on mitigating supply-chain disruptions to ensure that the company can continue to provide a large variety of products to its customers. In the face of procurement challenges, for the first time in a meaningful way, it preordered high-demand products and held products in inventory.

“Similarly, we expanded the number of vendors as well as increased the catalog of products to minimize any disruptions,” Oertell says. “Nevertheless, delays in available products and shipping delays had an impact on Q4 sales.”

FOCUS ON RISK MANAGEMENT

The pandemic forced many senior executives, including CFOs, to reevaluate the primary risks to their company. Many companies decided to hire a chief information security officer (CISO), and as the world gets more complicated and the various threats become more of a concern, companies will look to invest in hiring more people dedicated to compliance and enterprise risk management.

“Risk management is really important, and it’ll probably grow in importance as the pandemic and its impacts remain,” Choucair says.

Ephesoft executives are executing against their “most likely” plan scenario. Goel says that he and other company leaders have added focus on contingency planning and risk mitigation even going into 2022.

The 2017 framework, Enterprise Risk Management—Integrating with Strategy and Performance, from the Committee of Sponsoring Organizations of the Treadway Commission highlights the importance of integrating risk management in setting strategy as well as in driving performance (see Mark L. Frigo and Richard J. Anderson, “The CFO and Strategic Risk Management,” Strategic Finance, January 2021). For most finance executives, risk management will be top of mind for at least the next 12 to 18 months, Craighead predicts.

“I believe that the CFO’s crisis management role is temporary; however, I believe a higher level of risk management is a more permanent function of the role,” he says.

Risk management has moved front and center in many organizations during the pandemic and probably will remain a key priority for most organizations going forward. CFOs are going to be expected to manage compliance and risk mitigation for their respective organizations, Grinwis says.

“The ability to successfully identify risk factors will require CFOs to have a deep understanding of the regulatory, legal, and environmental changes to continually evaluate ongoing risk factors and work across their organizations to ensure they are mitigated,” he says.

McSherry agrees that risk management policies that focus on mitigating current risks, as well as avoiding potential risks, are as important as they’ve ever been. Risk management and technology adoption should be top of mind and high on the meeting agenda for any executive team today, he says.

“Operating a diversified business portfolio will always require reassessing solutions and continually scanning for possible business threats,” McSherry says. “This has become even more important as workforces have gone remote and global trends, both COVID-related and not, greatly impact regulatory shifts, business-model evolution, and more.”

Purchasing Power’s risk management at the beginning of the pandemic was different than it is today. At the beginning, like many companies, it pulled back across the board and adopted a wait-and-see approach. As everyone gained more understanding, risk management focused more on specific areas.

“We’re focused on the mental health of our employees and [the needs of] groups of customers who were adversely impacted by the pandemic,” Oertell says. “We’re also focused on our capital base and have increased our reserve capital.”

FORECASTING BASED ON ANALYTICS AND RESEARCH

Most CFOs and other finance professionals have been using basic enterprise technology and data analytics for some time already. That said, a large segment of the accounting and finance profession falls short when it comes to knowledge of newer technologies such as advanced AI and machine learning, blockchain, prescriptive and adaptive analytics, and data visualization. The pandemic has increased the urgency of getting up to speed on such advancements. Forecasting both profitability and risk has always been high on the priority list at BHG, McSherry says.

“[Our] data analytics team spends a significant amount of time in this area,” he says. “I believe that the pandemic has forced other businesses to place the same priority on stress-testing their business model.”

The pandemic has necessitated that companies increase the frequency of their forecasting efforts. That requires automation and reliable data, including labor costs and sales forecasts that can be integrated into big-picture forecasts accurately, according to Grinwis.

“The concept of rolling forecasts has always been a buzzword within finance, but I think when things are changing so quickly in the market, it benefits organizations to update forecasts quickly to understand the impact,” he says.

Another effect of the pandemic is more finance professionals using data analytics to achieve a solid understanding of the critical drivers for their organization, such as bookings, the sales pipeline, and pricing trends, and how those drivers are changing for better or worse.

“This means having dashboards to rely on for visibility that can show daily changes in these drivers and organizations’ different plans to react as needed,” Grinwis says.

Agility; flexibility; and a continuous cycle of planning, modeling, and forecasting are required not just to sustain your business, but also to beat expectations, Hansen says. Scenario planning has become a key element of reporting and forecasting for his team, and he says we’ll continue to see finance leaders embracing this in the future.

“We used to have a good and bad scenario planned out, but now CFOs have to think broader and plan for a larger variety of scenarios,” he says.

A well-designed process of continuous planning, where the team is constantly updating models and reforecasting based on current actuals, lets the CFO course-correct immediately, if need be. It also gets the CFO closer to data across the business by collaborating with all budget holders on decisions that benefit the entire company, not just a single department.

“Access to this data brings finance, HR, sales, and other teams into a conversation where everyone understands the goals, sees the progress, and is able to strategize collaboratively, with more unified thinking,” Hansen says.

Most finance professionals have already realized the importance of good forecasting and data analysis, but the pandemic has certainly shined a brighter light on this critical role. Many organizations will invest in better tools and staff that will allow this function to thrive and provide more clarity and accuracy to the business so that strategic planning can be more effective, Craighead says.

“At Quovant, we are currently implementing a robust BI [business intelligence] reporting platform for our internal team and our clients,” he says. “For our finance team specifically, we pay much closer attention now on a weekly basis to client invoice volumes and invoices’ size to better predict our future revenues and our clients’ health.”

There’s additional focus on scenario planning and “what-if” models and plans, Goel says. Most of his company’s board, investor, and management meetings now typically have a discussion around readiness for worst-case scenarios.

Before the pandemic, most CFOs were becoming increasingly focused on data, visibility, efficiency, speed, and transparency so that companies’ senior executives could make quicker decisions. And if you look at the last nearly two years, all that has accelerated.

“The demand on the CFO has increased significantly because the business needs all that data, but they need it faster and they need it more accurately, whether it’s liquidity, your 13-week working cash flow models, your budgets, or your due diligence on M&A [mergers and acquisitions], which has exploded,” Choucair says. “If you take into account what’s going on with your own company and what a CFO has to do, then layer on top of that the M&A piece, and then with that comes all the due diligence, bank financing, and raising equity.

“Businesses that have invested and continue to invest in digital transformation; automating reconciliations, journal entries, and the financial close process; and expanding to include products like FP&A and CPM [corporate performance management] tools, those finance departments are in much better shape to weather storms and achieve better efficiency and scale,” he says. “Investing in technology enables the CFO to be in the best position to respond quickly and accurately and report all the historical financials on time.”

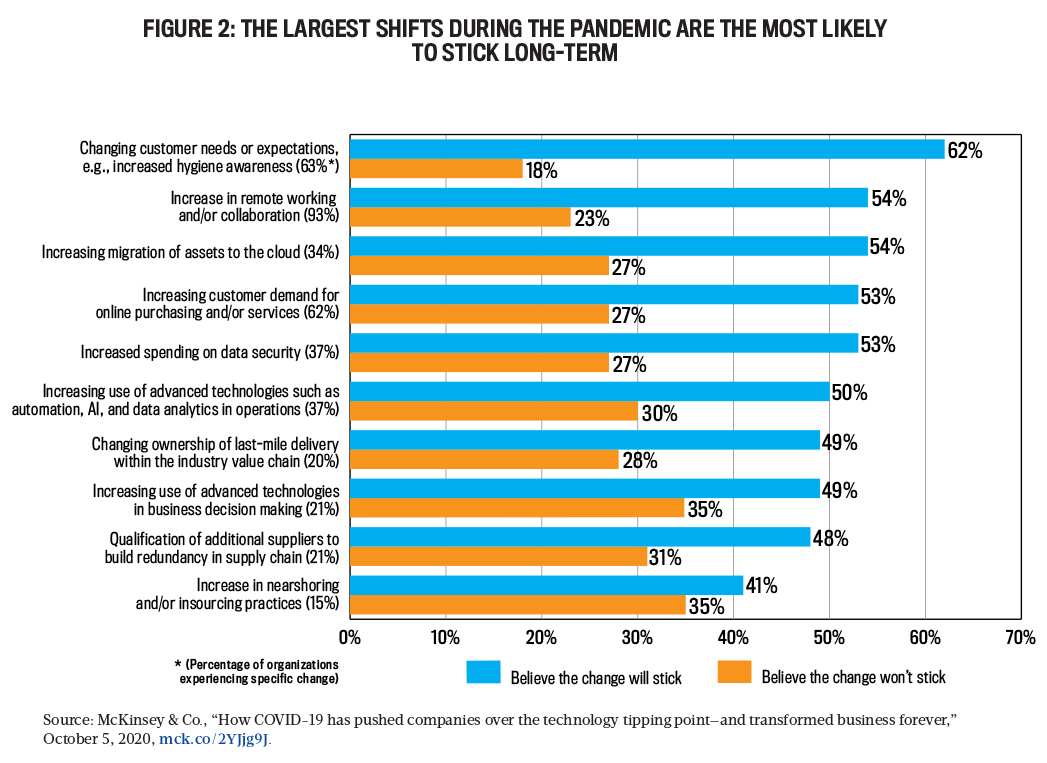

Goel says he thinks some of the increased focus on risk management will normalize over time, but technology adoption will remain steady or even accelerate. The overall adoption of cloud-based platforms, machine learning and other AI-based technologies, and blockchain is likely to continue as a focus for organizations to help drive productivity improvements and to be competitive in the marketplace, he says. See Figure 2 (Source: McKinsey & Co.) for a review of technology adoptions and other pandemic-driven changes expected to stick.

Click to enlarge.

“The introduction of core elements of hyperautomation like RPA, iPaaS, and IDP is likely to accelerate within forward-thinking organizations,” Goel says (see “What Is Hyperautomation?” at end of article).

Choucair says CFOs have also realized that the continued pressure on retaining top finance talent requires an acceleration of the automation of financial processes. This kind of technology not only fills talent gaps but also ensures that teams are enabled to focus on value-additive work as opposed to routine, manual tasks that tend to drive lower levels of employee engagement and satisfaction, he says.

“I also think the cadence of work will diminish over time, but the good habits we developed will remain,” Hansen says. “We may no longer need a weekly cash forecast, but we’ll have the tools to do that when needed—continuous planning will be the new name of the game.

“We’ll continue to see a reliance on cloud technology and companies embracing tools that make FP&A easier in a virtual environment,” he says.

Further, CFOs will look at technology investments that can automate processes and ensure a high level of compliance for their organizations. That will hopefully make management accounting and finance professionals’ jobs easier as their organization makes strategic plans for the post-pandemic competitive landscape.

“These investments will provide efficiencies to their employees while also scaling with their organizations for the future,” Grinwis says.

What Is Hyperautomation?

Organizations use hyperautomation to cut costs and optimize operations by identifying inefficiencies, redundancies, and repetitive tasks; vetting third-party software and services; and automating as many business and IT processes as possible. It helps with the implementation of various technologies, tools, and platforms to run in conjunction without human intervention, and according to Gartner, it includes:

- RPA

- AI, machine learning, deep learning, natural language processing, expert systems, robotics, machine vision, optical character recognition, and/or speech recognition

- Event-driven architecture, where event notifications trigger a software component to automatically execute a programmed response

- Process mining, business process management (BPM), and intelligent BPM suites, consisting of models for the discovery, definition, design, implementation, monitoring, and analysis of processes for optimization and collaboration

- Integration platform as a service (iPaaS), which connects

- on-premises and cloud-based processes, services, applications, and data, developing, executing, and governing integration flows within a single organization or across a consortium

- Intelligent document processing (IDP) or integrated document management, network-based middleware services that integrate critical business-process applications with library services, document manufacturing, and document-interchange technologies

- Low-code/no-code platforms, packaged software, and other types of tools to automate decision making, processes, and tasks

A CISO’s Primary Responsibilities

The chief information security officer (CISO, aka the chief security officer, chief security architect, security manager, corporate security officer, or information security manager) is a senior executive with expertise in IT, cybersecurity, risk management, and auditing who can communicate complicated technical concepts to nontechnical leaders and employees. The CEO or chief information officer typically delegates tasks related to data security to the CISO, including:

- Developing and implementing an information security program with procedures, policies, and practices designed to manage enterprise risks and protect the organization’s communications, systems, and assets from both internal and external threats;

- Procuring cybersecurity products and services, mitigating the various risks that security threats pose to the organization’s mission and goals, and managing disaster recovery and business continuity plans;

- Anticipating, assessing, and actively managing new and emerging threats, as well as responding to data breaches and other security incidents;

- Coordinating with the chief legal officer, general counsel, head of risk management, and/or chief compliance officer to ensure that the company is in legal and regulatory compliance; managing the computer security incident response team; and conducting electronic discovery and digital forensic investigations;

- Ensuring the data privacy and overall corporate security of the organization, its employees, and its facilities; conducting employee security awareness training; and enforcing adherence to security practices.

Source: CIO Council, Chief Information Security Officer Handbook; TechTarget.

February 2022