This article is based on research funded by a grant from the IMA® Research Foundation.

Whistleblowers have traditionally been employees within an organization who lack the authority to stop fraudulent activities but choose to report them nonetheless. But in today’s business environment, whistleblowers can also include individuals outside the organization, as functions like IT, human resources, and accounting are often outsourced.

As individuals and external parties gain access to sensitive information, they possess the ability to expose unethical or illegal activities through whistleblowing. This includes situations where buyers, suppliers, or business partners become aware of misconduct and choose to report such wrongdoing. Given that business partnerships rely on trust, any perceived breach of that trust may lead the affected party to blow the whistle. In addition, consumers may also have the potential to report wrongdoing, such as questioning sustainability claims or ethical production practices. These external factors increase the need for businesses to establish and maintain a strong ethical control function, showcasing their commitment to addressing misconduct and meeting the expectations of investors, regulators, customers, and consumers.

Previous research indicates that the type of wrongdoing significantly influences an individual’s decision to blow the whistle. For instance, misconduct involving physical harm, such as sexual assault, is more likely to be reported compared to misconduct involving economic or psychological harm, like discrimination. Furthermore, the severity of the fraud plays a role in the decision to blow the whistle. Instances of material financial reporting fraud are more likely to be reported than cases of immaterial fraud. Moreover, there’s a perception that certain types of fraudulent activities are viewed as more severe. Accepting bribes or stealing company funds is viewed as more severe than position abuses, unfair advantages, or discrimination.

Factors of Whistleblowing

Fraud encompasses a broad range of actions, including financial reporting fraud, tax evasion, bribery, discrimination, sexual harassment, false advertising, pollution, occupational health and safety violations, unjust dismissal, mobbing, aggressive behavior, unjust career advancements, nepotism, and more (see Barbara Culiberg and Katarina Katja Mihelič, “The Evolution of Whistleblowing Studies: A Critical Review and Research Agenda,” Journal of Business Ethics, 2017, pp. 787-803). To promote effective whistleblowing, practitioners must recognize the diverse nature of fraudulent activities and acknowledge the varying likelihood of their disclosure.

Other factors can also influence the decision to blow the whistle, including individual characteristics and situational factors, but the findings related to individual characteristics like gender, age, education, and pay are often inconclusive. Some studies suggest that men are more likely to report misconduct (see also Marcia P. Miceli and Janet P. Near, “Characteristics of organizational climate and perceived wrongdoing associated with whistle‐blowing decisions,” Personnel Psychology, September 1985, pp. 525-544), while others indicate that women are more inclined to blow the whistle (see also Jessica R. Mesmer-Magnus and Chockalingam Viswesvaran, “Whistleblowing in Organizations: An Examination of Correlates of Whistleblowing Intentions, Actions, and Retaliation,” Journal of Business Ethics, 2005, pp. 277-297). There are also studies that have found no significant relationship between gender and whistleblowing (see also Julia Zhang, Randy Chiu, and Liqun Wei, “Decision-Making Process of Internal Whistleblowing Behavior in China: Empirical Evidence and Implications,” Journal of Business Ethics, April 2009, pp. 25-41).

On the other hand, situational factors have been found to have greater explanatory power and consistency. A robust ethical culture within an organization that promotes and supports whistleblowing can enhance the intention to report misconduct. Moreover, the broader national culture can also impact the inclination to blow the whistle. For instance, if the legal environment provides protections for whistleblowers, individuals may be more inclined to report wrongdoing.

When deciding whether to blow the whistle, employees also need to choose a reporting channel, which can be either internal or external. Internal whistleblowing involves reporting misconduct to individuals within the organization, usually through a confidential hotline or other designated channels. On the other hand, external whistleblowing entails reporting wrongdoing to entities outside of the organization, such as the media, governmental agencies, or professional organizations.

Internal whistleblowing hotlines play a crucial role in organizations’ efforts to detect fraud. According to a survey conducted by the Association of Certified Fraud Examiners in 2022, employee tips accounted for 42% of fraud detections, making it the most common method for uncovering fraudulent activities. Other methods included internal audit (16%), management review (12%), document examination (6%), and accidents (5%). These findings underscore the significance of internal whistleblowing programs in identifying and addressing fraudulent behavior. The implementation of regulations such as the Dodd-Frank Wall Street Reform and Consumer Protection Act has further emphasized the importance of strengthening internal whistleblowing programs. These regulations have increased the pressure on organizations to enhance their internal reporting mechanisms in order to effectively address and remediate misconduct or fraudulent behavior. In the current regulatory environment, distinguishing between unethical conduct and unlawful behavior is often challenging. Therefore, organizations must take a proactive approach to identify and address misconduct to avoid potential investigations, fines, and reputational damage from regulatory bodies like the U.S. Securities & Exchange Commission (SEC) (see also Bill Libit, Todd Freier, and Walt Draney, Elements of an Effective Whistleblower Hotline).

Effect of Social Identity

While maintaining effective internal whistleblowing programs is vital, recent research has highlighted the significance of organizational context, particularly group identification, in influencing these programs. Internal whistleblowing often requires employees to report misconduct by their colleagues or teammates because they’re most familiar with the behaviors of those they interact with regularly. This raises the question of whether factors related to group dynamics, such as identification with the group, impact an employee’s willingness to blow the whistle. Understanding these dynamics can help organizations create a supportive environment that encourages reporting while addressing potential barriers to reporting within group settings.

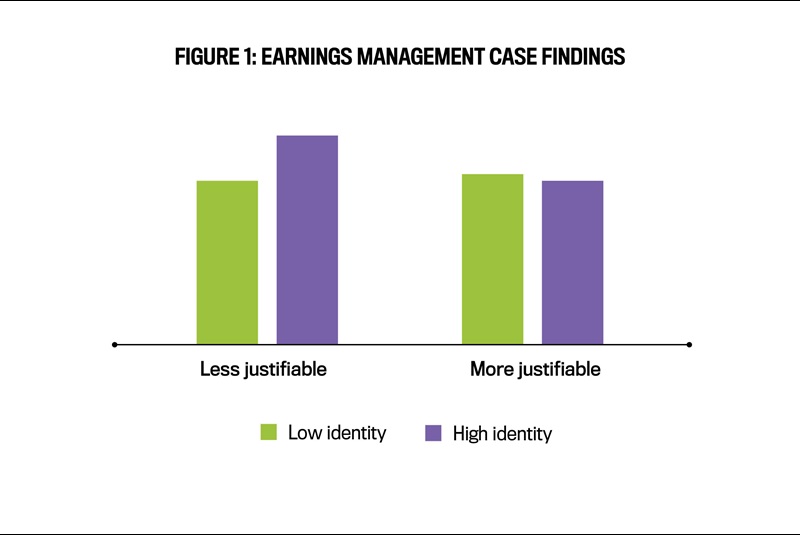

In a recent study, Yuebing Liu and Hui Xu investigated the influence of social identity and the perceived justifiability of questionable behavior on individuals’ willingness to blow the whistle (“The Effects of Social Identity and Justifiability of Questionable Behavior on Whistleblowing,” Journal of Forensic and Investigative Accounting Research, July-December 2021, pp. 302-318). The study involved presenting two hypothetical business scenarios to a group of accounting students. In both scenarios, the focal person engaged in questionable practices to meet earnings targets: one by arbitrarily changing accounting estimates without a legitimate reason and the other by excessively producing products. The findings, presented in Figure 1, revealed intriguing insights. When the focal person arbitrarily changed accounting estimates to inflate earnings, the students were more likely to report the misconduct if they shared the same social identity with the focal person. But when the focal person inflated reported earnings through overproduction, there was no significant difference in the likelihood to report the questionable behavior, regardless of social identity.

These results indicate that social identity can indeed influence the reporting of fraudulent activities, but it may not have the same impact when questionable behavior is perceived as somewhat justifiable. This study sheds light on the complex interplay between social identity, justifiability, and whistleblowing, highlighting the importance of considering these factors when designing interventions to encourage reporting and deter unethical behavior within organizations.

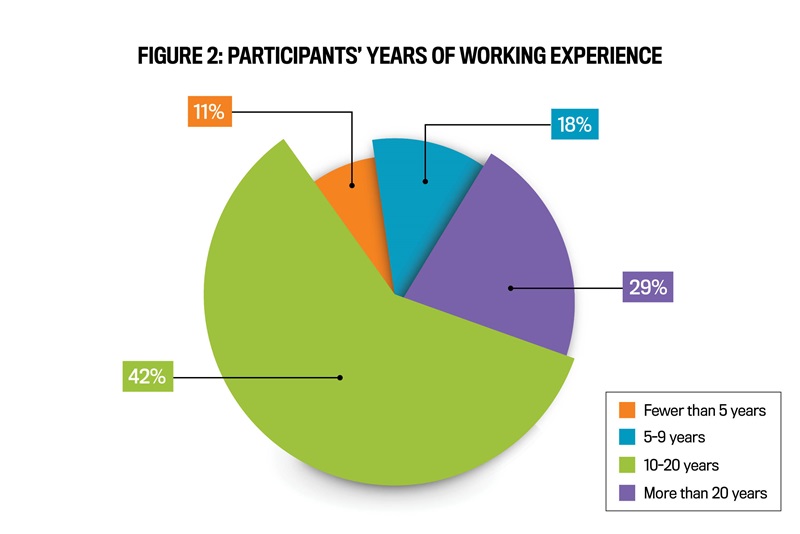

The authors further validated their initial findings through a second study involving experienced participants who were presented with potential scenarios of consumer data breaches. Figure 2 displays the distribution of participants’ years of working experience, with a majority having more than 10 years of experience and approximately 29% having more than 20 years of experience.

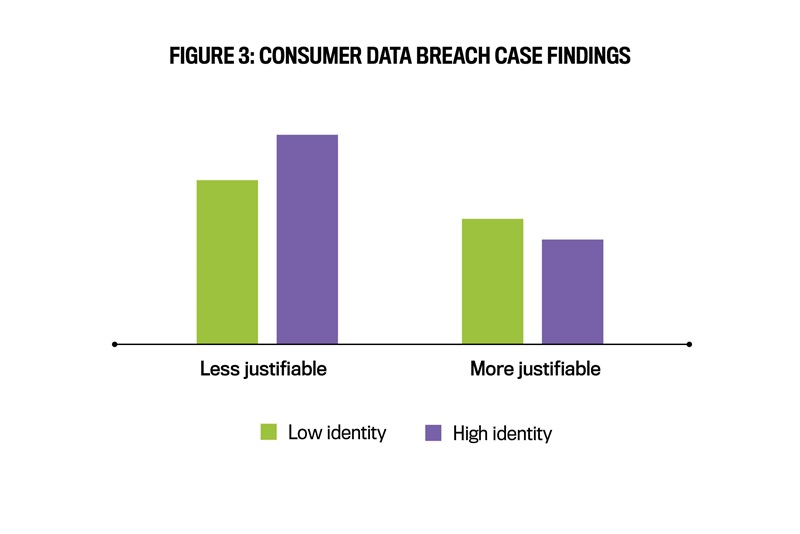

In one scenario, the vendor’s credentials for the focal company were accidentally exposed, but the consumers’ private information remained secure and wasn’t accessed. In the other scenario, the consumers’ private information was accessible due to a successful hack of the company’s system. In both cases, the focal person took action to address the immediate security concern by removing the exposed account but didn’t take additional measures to enhance the overall infrastructure security or report the incident to upper management. The behavior of the focal person in the former case can be seen as somewhat justifiable since the consumers’ private information remained secure. But the behavior in the latter case, where the company’s system was hacked, is more difficult to justify.

The results, depicted in Figure 3, mirror the findings of the first study. When the questionable act was less justifiable (i.e., the company’s system was hacked, and consumer private information was accessible), the participants were more likely to report the incident if they shared the same social identity with the focal person. But when the questionable act was more justifiable (i.e., the vendor’s credentials were accidentally exposed, but consumer private information remained secure), this tendency was either attenuated or reversed. In such cases, participants who shared the same social identity with the focal person were less likely to report the incident compared to those who didn’t share the same social identity.

The authors propose that the findings of the two studies can be explained by social identity theory, which suggests that individuals derive a sense of belonging, pride, and self-esteem from their perceived membership in social groups. This theory indicates that individuals are motivated to maintain a positive image of themselves and the social groups they identify with. This motivation can lead to biased judgment and behavior toward individuals from different social groups, favoring those within their own group, a phenomenon known as in-group favoritism.

Interestingly, under certain circumstances, an in-group member may be judged more negatively than an out-group member, known as the “black sheep” effect. This finding may seem to contradict social identity theory, which generally predicts that in-group members are favored over out-group members. But the black sheep effect can be seen as a more nuanced expression of in-group favoritism. When a group member engages in deviant behavior that threatens the group’s image, other group members may attempt to distance themselves from that individual by portraying them in a negative light. This strategy ultimately serves to protect and maintain a positive image for the rest of the group.

Under what circumstances does in-group favoritism or the black sheep effect occur? How do individuals determine the acceptability of questionable behavior? These questions depend on various factors, including the alignment of the behavior with laws, codes of conduct, social norms, and ethical principles. Individuals are more likely to blow the whistle when they perceive the behavior of an in-group member as clearly wrong because they view the wrongdoer as a threat to the group’s reputation and feel an obligation to protect the group’s positive image. In this case, the black sheep effect dominates the judgment. If the wrongdoer is punished and excluded from the group, the group’s image can be restored.

On the other hand, when the questionable behavior is ambiguous and potentially justifiable, it may not pose a threat to the group’s positive image. In such cases, in-group favoritism dominates judgment, leading to a lower likelihood of whistleblowing when the behavior is committed by an in-group member compared to an out-group member. Observers may be more inclined to rationalize such behavior, consciously or unconsciously, when it’s performed by an in-group member. Furthermore, if the questionable behavior isn’t perceived as threatening, individuals may not feel a sense of obligation to report it. This argument is supported by the findings of Liu and Xu, who assessed participants’ perceived obligation to report questionable behavior in a post-experimental questionnaire.

In summary, the study suggests that while a strong social identity can enhance the ability of internal whistleblowing programs to identify severe fraud, it may also hinder the ability to identify potential fraudulent activities at an early stage when they aren’t yet illegal and may be more justifiable. As a result, companies must carefully consider the costs and benefits of using social identity in their management control systems and weigh the potential risks and rewards.

What Should Management Do?

Management may consider two approaches inspired by the research findings: fostering stronger bonding among employees and enhancing employees’ moral standards. Strengthening the bonding among employees can lead to a higher level of social identity, resulting in improved team outcomes such as enhanced coordination, knowledge sharing, and creativity. Recognizing the significance of team identity in shaping employee attitudes and behaviors, it’s crucial for managers to proactively establish and nurture a strong team identity. To achieve this, we propose the following 4C approach for managers aiming to build a robust team identity:

1. Clarity: A manager must engage in a collaborative process with team members to establish a clear and mutually agreed-upon mission and vision for the team. This involves defining specific team goals and clarifying the roles and responsibilities of each team member. Providing a clear sense of purpose and structure fosters a greater sense of belonging and cohesion among team members, leading to improved productivity and performance. Having a shared mission and vision aligns individual efforts and motivations with overall team objectives, promoting a sense of ownership and accountability.

2. Commitment: Cultivating a strong sense of commitment among team members is essential for fostering a cohesive and productive team. One way to achieve this is by promoting a culture of mutual accountability, where everyone is responsible for upholding the team’s goals and standards. Such a culture creates a shared sense of purpose and motivates teamwork. In addition, it’s vital to recognize and value each team member’s contributions as a way to build pride and ownership in their work.

3. Contribution: To maximize the team’s potential, managers should carefully assess the unique strengths and weaknesses of each team member. This involves conducting a thorough analysis of their skills, experience, and expertise to determine the most effective ways to delegate responsibilities and optimize their contributions. Understanding individual working styles and needs enables managers to make well-informed decisions and allocate resources efficiently, leading to increased productivity and success for the team.

4. Communication: Effective communication is critical for any successful team, and managers play a crucial role in promoting open and honest communication among team members. Encouraging open dialogue, setting aside dedicated time for discussions, and ensuring transparency in decision making are essential strategies. By fostering an environment where team members feel comfortable expressing their thoughts and concerns, managers can facilitate the timely resolution of problems and issues, ultimately creating a more positive and productive working environment.

Using these 4C tips, managers can effectively establish and cultivate a strong team identity that promotes teamwork, commitment, and a sense of belonging among employees, ultimately leading to better outcomes for the team and organization. To enhance employees’ moral standards, we propose the following 5C approach for managers:

1. Culture: To enhance employees’ moral standards, organizations must cultivate a pervasive ethical culture that emphasizes integrity, transparency, and ethical conduct. Managers play a key role in establishing this culture by defining a robust ethical framework and core values embedded in the organization. These values should serve as guiding principles for employees, shaping their actions and decisions. By celebrating and reinforcing ethical behavior, promoting open discussions about ethical dilemmas, and providing ethical training and resources, managers can foster an environment where employees are dedicated to upholding high ethical standards throughout the organization.

2. Code of conduct: Managers should establish a comprehensive code of conduct that clearly outlines the organization’s ethical standards and expectations for all employees. The code of conduct should provide specific guidelines on appropriate behavior, address potential ethical dilemmas employees may encounter, and highlight the consequences of misconduct. Ensuring that employees are well-versed in and adhere to the code of conduct creates a consistent and ethical work environment, fostering trust and integrity. Regular communication and training on the code of conduct further reinforce its significance and encourage ethical decision making among employees.

3. Compliance training: It’s critical for managers to provide comprehensive compliance training to all employees to ensure a clear understanding of their legal and ethical obligations. The training program should encompass relevant laws, regulations, industry standards, and company policies, enabling employees to make informed and ethical decisions while taking appropriate actions. Regularly scheduled training sessions and workshops can reinforce the importance of compliance and ethics, nurturing a culture of responsibility and accountability across the organization. In addition, managers should actively engage with employees during the training process, encouraging open discussions and addressing any questions or concerns that may arise, thereby nurturing a strong commitment to ethical conduct at all levels of the organization.

4. Communication: Managers should foster a culture of open and transparent communication within the organization, encouraging employees to voice their ethical concerns, provide feedback, and report any misconduct through confidential reporting mechanisms. Moreover, it’s essential to establish and promote communication channels that facilitate ethical dialogue, ensuring that employees feel comfortable and supported in expressing their views. By valuing and respecting ethical communication, the organization can create an environment of trust and accountability, facilitating the prompt and effective resolution of ethical issues.

5. Continuous improvement: To optimize the impact of ethical practices, continuous evaluation and improvement of the organization’s ethical practices and compliance efforts are essential. Conducting regular audits, assessments, and reviews helps identify areas of improvement, address gaps or weaknesses, and adapt policies and procedures to evolving ethical standards and legal requirements. Emphasizing the value of learning from past experiences and utilizing insights gained drives positive changes, strengthening the organization’s commitment to ethics and compliance.

By implementing the 5C approach, organizations can enhance their employees’ morale and cultivate a robust ethical culture throughout the organization. The concept of social identity offers significant advantages in driving team outcomes within organizations. But it’s crucial for organizations to be mindful of its potential negative implications for internal whistleblowing programs. By adopting the recommended 4C and 5C approaches, organizations can harness the productivity benefits of a strong social identity while proactively mitigating its potential drawbacks. These approaches not only enhance team cohesion and productivity but also fortify the organization against fraud and misconduct, safeguard its reputation, and foster a more ethical work environment. Striking this balance will lead to a healthier and more sustainable organizational culture, where employees are empowered to uphold high ethical standards and contribute to the overall success of the organization.

For more on this subject, check out the Count Me In podcast Ep. 190: Gordon Graham - The Ethics and Risks of Whistleblowing.

September 2023