2024 STUDENT CASE COMPETITION

The Student Case Competition is sponsored annually by IMA® to provide an opportunity for students to interpret, analyze, evaluate, synthesize, and communicate a solution to a management accounting problem.

Unbekannt, Inc., is a food distributor that specializes in foreign events. While headquartered in the United States, it does business around the world, shipping specialized food, beverages, and decor from one nation to another in order to host special events. For example, it provides German beverages, sausages, and costumes to venues in the U.S. as part of Oktoberfest events. The company also ships Mexican foods, horchata, sombreros, and other traditional items to Japanese hotels wishing to host Cinco de Mayo celebrations.

Overall, the business has been very successful, especially with its respectful focus on sharing cultural traditions. It has low production costs, since it purchases food, beverages, and decorations from established vendors in the countries where the traditions originate and rents shipping space from large airlines. Most of its costs are driven by labor, since it hires experts in linguistics and local traditions and customs. Because specialty suppliers, not the company, host the events, Unbekannt doesn’t take on much risk. In other words, it gets paid whether or not the event is a success. That said, Unbekannt’s employees take pride in their work and do everything they can to help the different venues around the world plan and execute successful events that will become local traditions, providing Unbekannt with continuing markets for its services.

Unfortunately, the company faced challenges during a recent economic downturn as venues closed and shipping became more difficult. The company was able to leverage its existing connections and continue to operate by modifying its services. Instead of supplying large gatherings, Unbekannt would provide party boxes for individuals and outdoor decorations. The result was a series of small, more reasonably priced events that kept the company solvent and its employees paid. As the downturn continued, Unbekannt was able to provide some exciting opportunities for clients looking to host parties and other activities to reinvigorate communities or advertise their products.

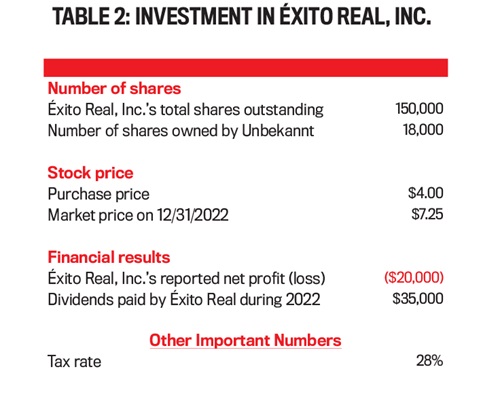

By the end of last year, in fact, Unbekannt’s finance team was in the unusual position of having extra cash and no readily available investment opportunities. After long consultations, the team decided that its best option was to purchase stock in some of its suppliers, especially a company named Éxito Real, Inc. Éxito is headquartered in Mexico City and provides most of the food and costumes Unbekannt uses for its popular Cinco de Mayo events. Éxito’s shares on Nasdaq dropped significantly during the downturn, and Unbekannt’s finance team felt that purchasing stock in Éxito would not only give Unbekannt a chance to help support a key supplier but would also give it a way to ensure that Éxito continued to provide Unbekannt with the same services it had offered in the past. At the time of its initial investment, Unbekannt became the largest single shareholder in Éxito other than the company’s founder, who owned 25%.

Finance Leadership Meeting

During the downturn, Unbekannt’s finance team held daily meetings to address cash needs, financing options, reporting requirements, and, more recently, investment opportunities. The meetings were led by Azul, the company’s CFO, with support from Beslau, the controller, and Kendi, the director of finance.

Other team members were invited as needed, but today’s meeting included only the three leaders. They needed to make some decisions about their recent investment in Éxito Real, and Azul felt the meeting would be more effective with just the leadership team.

“Good afternoon, Beslau,” Kendi said as they entered the boardroom for the day’s meeting. “How are you doing?”

“I’m doing well, danke,” Beslau replied, with a light German accent. Beslau was born in Munich but migrated to the U.S. with family at age 11. Most of the time, Beslau’s accent was barely recognizable, but it did tend to come out late in the day as he got tired. “And you?”

“I’m doing just fine, although I wish this meeting were over.” Kendi was an immigrant from the Ivory Coast but came to the U.S. as a baby. There was no accent to give away Kendi’s origin.

“Really?” Beslau asked. “Why’s that?”

“Because this isn’t going to be a good meeting, and you know it.” Kendi slouched into a chair and looked out the window. “It’s going to be all about GAAP [Generally Accepted Accounting Principles] rules as we get ready for the annual financial statements.”

Kendi held up a hand. “Don’t tell me. You’re all excited about it, but some of us, believe it or not, find it kind of boring.”

Beslau just chuckled and found a seat that also had a good view of the nearby lake. “You finance people don’t know fun when you see it! This is going to be a great meeting.”

“Of course it is!” Both Kendi and Beslau jumped as Azul came in. Azul was born in south Texas and had a deep southern drawl, despite being raised by Mexican parents and speaking Spanish fluently. “We’re gonna have us a great time this afternoon. I mean, who doesn’t love figuring out how to share good news with our investors?”

Kendi sighed. “Can’t you at least pretend to be a finance person still?”

Azul laughed. “I’m the CFO, Kendi. I can’t afford to play favorites between accounting and finance. I have to work both sides, so of course I’m excited to be here. Let’s get started.”

Azul sat down between the two other senior members of Unbekannt’s finance department. “I’ll keep it quick, since some of you have unreasonable prejudices.”

Kendi sighed. It was going to be one of those meetings.

“We’re comin’ up on year-end, like Kendi said. How’re our books looking?” Azul asked.

Beslau shrugged. “Given what’s going on in the world, they look pretty good. Actually, they look much better than last year. The increases in prices across the board haven’t helped, so our margins aren’t as good as they were before the economy tanked, but we’re doing okay. I think we’ll just meet analysts’ forecasts.”

Kendi smiled. “Excellent. Everything looks good, we’re going to meet our targets, and everyone’s happy. Meeting adjourned!”

Azul frowned. “Kendi,” he said reprovingly.

“All right. I’m sorry. What’s up?” Kendi said.

“I think we need to decide what to do with our investment in Éxito,” Azul answered.

Beslau frowned. “Why? Do you want to buy more shares? Or maybe you want to sell a few. I haven’t seen the current market price for their stock.”

“No, no. I’m happy with our stake,” Azul said.

Kendi frowned. “Then what do we need to decide?”

“How to treat it for accounting purposes,” Azul said.

“It’s a stock investment, and we’re using the fair value method. That’s really our only option, since Éxito’s stock is publicly traded and the price is easy to find,” Beslau said.

“No,” Azul disagreed. “It’s not our only option. We could use the equity method.”

“Why would we want to do that?” Beslau asked.

“Have you looked at Éxito’s current stock price?” Azul asked.

“I know it has fluctuated the last few weeks. That’s why I thought, like Kendi, that you might be thinking of adjusting our holdings,” Beslau said.

“I don’t want to buy more; we need our cash for other things right now,” Azul said.

“It’s not a big change in value, so it won’t have a big effect on our financials. I mean, our EPS [earnings per share] is going to meet analysts’ expectations regardless of what happens with Exito’s stock price,” Beslau replied.

Azul nodded. “As long as there isn’t a big bump between now and year-end, but what if something happens in this last week, or what if, heaven forbid, the auditors find something in our financials that has to be corrected? Wouldn’t it be better to use the equity method for the investment? That will give us an income effect that’s easier to forecast than market prices.”

“What are you talking about?” Kendi asked. “I don’t remember much about the equity method from my college accounting classes, but I do remember you can’t use it unless you own at least 20% of the outstanding stock, and we aren’t even close.”

“Wait,” Beslau objected. “Azul might be right. We might have a case for using the equity method. I haven’t looked at the rules in a while since we don’t own any other investees, but I believe the term the FASB [Financial Accounting Standards Board] uses is ‘significant influence’ over the investee company to switch to the equity method, and the FASB presumes that you have significant influence once you own at least 20% of the outstanding stock.”

“But we don’t own 20% of the outstanding stock,” Kendi started to say, but Azul jumped in.

“No, but we’re the second biggest stockholder, and the founder doesn’t have a controlling vote.”

“But we don’t have a seat on the board,” Kendi countered.

“But they did offer us one,” Beslau said with a slight frown. “We just didn’t like the conditions they put on us.”

“Oh, yeah,” Kendi nodded. “Didn’t they say that we couldn’t buy any more stock for like 12 months or something?”

Azul nodded. “Which suggests that they’re afraid that we own too much of the stock and supports us having a significant influence.”

“And we’re one of their biggest customers,” Beslau added. “That also indicates some influence.”

“I don’t know,” Kendi said. “Aren’t we pushing here? And for what? Just to switch from a market-based adjustment to an investee profit-based adjustment? That doesn’t seem worth the hassle. And we aren’t even sure about the rule. For all we know, GAAP may require that we do have to own a full 20%. We need to find out.”

“That’s a good point,” Beslau agreed. “This can’t be about our projections. It needs to be about following GAAP. That’s what our investors expect and what the auditors are looking for. I agree that a more stable prediction would be nice, especially since we’re having a good year. But it isn’t worth a fight with the auditors.”

Azul nodded. “Which means we should switch.”

“Which means,” Beslau disagreed, “that we need to dig a little deeper, reread the rules, look at the entries, and see which option would provide the best information for our investors and other stakeholders.”

“Oh, sure,” Azul said, “and I’m sure that will be to use the equity method.”

Kendi sighed. “I’m sure you do feel that way. But for now, maybe Beslau and the accounting team can run some numbers and do some more research for us.”

“Good idea. Let’s meet again in two days,” Azul decided. “Beslau, please bring the information about both options and a recommendation so we can get the change made.”

Case Questions

1. Make the necessary adjusting entries to account for Unbekannt, Inc.’s investment in Éxito Real, Inc., at the end of the fiscal year, assuming that Unbekannt’s finance team decides to use the fair value method to account for the investment.

2. Update Unbekannt, Inc.’s financial statements to incorporate the effects of the adjusting entries for the fair value method.

3. Make the necessary adjusting entries to account for Unbekannt, Inc.’s investment in Éxito Real, Inc., at the end of the fiscal year, assuming that Unbekannt’s finance team decides to use the equity method to account for the investment.

4. Update Unbekannt, Inc.’s financial statements to incorporate the effects of the adjusting entries for the equity method.

5. Find the financial accounting standards that a company should use to determine when to use the equity method of accounting. If you’re studying in the U.S., please use U.S. GAAP, available at FASB.org, for your research. If you’re studying outside of the U.S., please use International Financial Reporting Standards (IFRS), available at IFRS.org, for your research. Note: You’ll need to register for a free account to access the IFRS database if you don’t already have one.

6. Using your answers to the previous questions, determine the correct classification for Unbekannt’s investment in Éxito Real, Inc. Defend your answer sufficiently to convince the finance team to follow your recommendation.

August 2023