The healthcare industry, one of the largest, most complex, and truly essential industries in the world, finds itself constantly challenged to improve quality and lower costs while delivering value. Consequently, the role of cost management, led by management accountants (i.e., accountants and financial professionals in business), and the need for innovative costing practices have become critical to the healthcare industry’s sustainability and positive contribution to people, society, and the economy.

Heightened demand for greater value delivery by finance and accounting teams in healthcare prompts finance functions in healthcare to walk a tightrope between their evolving role and challenges faced with cost management innovation. Understanding the current healthcare cost management landscape, acknowledging challenges faced, and preparing for the finance function’s expanded role are integral to the healthcare industry’s future.

THE INTERSECTION OF COST AND VALUE

Of all the transformations shaping healthcare in the United States, none is more profound than the shift toward value. Quality and patient satisfaction are being factored into Medicare payment models, while private payers are incorporating performance and risk-based payment structures into their contracts. At the same time, rising healthcare costs are creating more price sensitivity among healthcare purchasers, including government agencies, employers, and, of course, patients themselves, who are being asked to pay higher premiums, copayments, and deductibles for their care. Hospitals have always focused on quality because they’re fundamentally dedicated to patient well-being. But recent pressures make it financially imperative to develop collaborative approaches that combine strong clinical outcomes with effective cost management.

For providers to deliver value in healthcare, they must have accurate, actionable data on the two elements driving the value equation: the quality of the care delivered and the cost of providing the care (the basis for the price that purchasers should be asked to pay for care). They must also be able to link quality and cost metrics to quantify the value of care provided. To build this business case, healthcare organizations must have capabilities to perform several functions:

- Accurately and consistently report cost and other financial data on appropriate metrics developed in collaboration with clinicians

- Drive information sharing throughout the organization by linking dashboards and individual measures to strategic goals

- Report quality results to both internal and external stakeholders

The need for better costing and other business analytics in healthcare is both recognized and real. Many providers readily acknowledge the inadequacies of their current systems. They’re working to enhance their organizational competencies enabling optimal data utilization and to develop the systems that will lay the foundation to succeed under value-based care models and other risk arrangements. In comparison to the investments in information and analytics for clinical quality, however, investments in business intelligence on the finance side have lagged. As a result, tying cost implications to performance on quality metrics often requires a considerable amount of time-consuming, manual work. Providers also struggle to precisely quantify the financial impact of quality initiatives, although the effects of quality initiatives on metrics such as length of stay and other indirect macro indicators demonstrate when initiatives are working to reduce costs.

Costing information is clearly recognized as important as providers facilitate linking clinicians and staff throughout the organization, produce data that can verify the outcomes and financial implications of performance improvement efforts, and enable the creation of patient information repositories that will become increasingly important as providers assume risk contracts.

INNOVATING COSTING PRACTICES

Providers recognize the significance of the link between quality improvement and cost management efforts. They’re measuring the impact of quality and waste on their organizations and contemplating moving beyond traditional methods of cost accounting.

IMA® (Institute of Management Accountants) and the Healthcare Financial Management Association (HFMA) hosted roundtable discussions during which participants shared their perspectives on (1) how healthcare costing information is utilized to set healthcare pricing (from a patient’s perspective) and improve transparency and (2) how costing practices impact overall healthcare costs in the U.S. (see “About Our Study”). Key takeaways from this discussion include:

- Recognition that the U.S. healthcare industry’s pricing strategy is driven by the market rather than costs, and

- A lack of consensus with respect to the impact of costing methodologies and practices on overall healthcare costs because of the great variation in costing approaches across organizations and sometimes among different divisions within a single organization.

Despite these circumstances, there was consensus among participants that more innovative costing approaches would be incrementally beneficial to the finance function’s delivery of value to the healthcare organizations that they support. Thus, a deeper discussion emerged around activity-based costing (ABC).

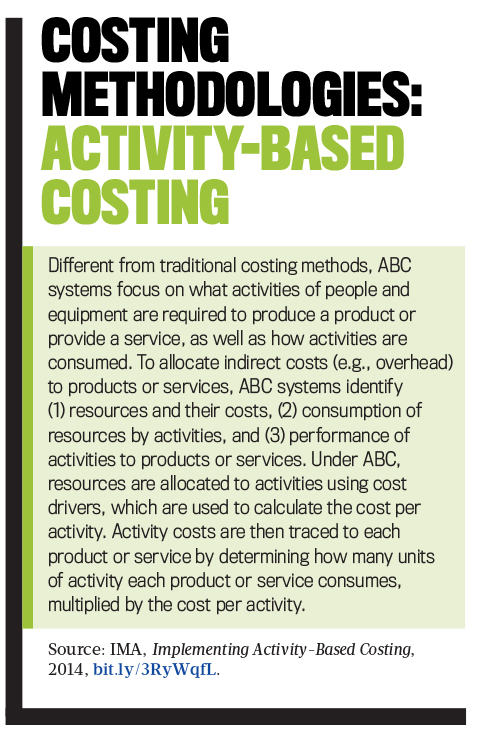

Yet, as found in a 2017 study on the adoption of ABC in the healthcare industry conducted by IMA and the HFMA, healthcare organizations generally recognize the problems associated with their current accounting systems, but most choose not to implement ABC systems despite the potential benefits (see “Costing Methodologies: Activity-Based Costing” for a detailed definition). Figure 1 summarizes the top five reasons for not adopting ABC as documented in the 2017 study.

Most roundtable participants confirmed that the adoption of ABC or other advanced costing systems such as time-driven activity-based costing (TDABC) was out of the realm of possibilities within their organizations for the foreseeable future. When asked to identify the drivers for nonadoption, participants pointed to the complexity of deploying these systems, constraints of internal resources, and others. For example, a common issue for a healthcare system with various services in multiple locations but sharing the same integrated information system data hosting is that, given that each service might use the system differently than others within the same organization, analyzing the level of details to achieve like-kind comparison across service lines using ABC or TDABC becomes increasingly challenging.

KEY CHALLENGES IN COSTING PRACTICES IMPROVEMENT

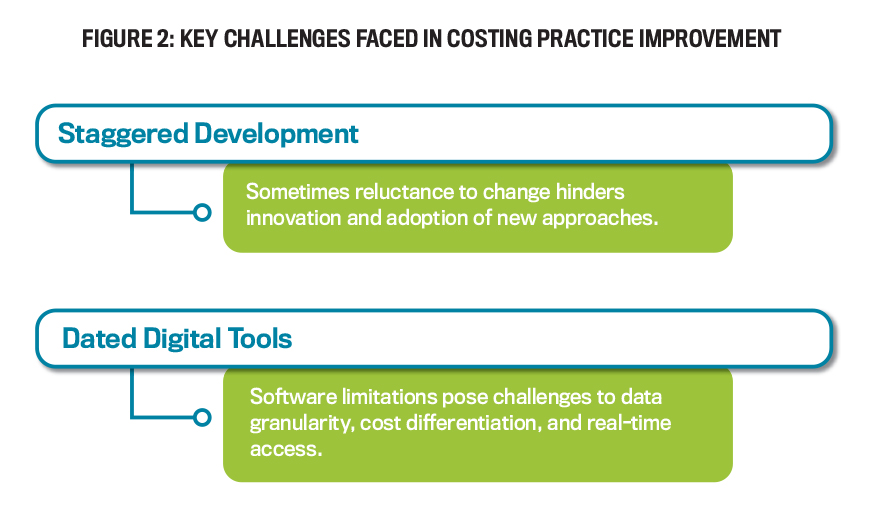

While the benefits of adopting a sound and reliable costing system are obvious, barriers to achieving it can’t be overlooked. Key examples of such challenges are staggered development in healthcare and the inadequacy of internal resources needed for execution (see Figure 2).

Staggered development in healthcare. One study participant, who previously worked in the manufacturing industry, said that when he started in healthcare, he was surprised that the industry seemed to be lagging in many aspects, including costing, from a quality reporting and technology perspective. Although tremendous strides have been made in catching up in the past two decades, there’s still room for considerable improvement in healthcare, especially in facilitating real-time, data-driven decision making supported by advanced data science and technologies.

Yet, based on the observations of our study participants, the industry often feels slow-moving, risk averse, and reluctant to change as it pertains to innovation and the adoption of new approaches—even as improvements in technology have made more data available. Furthermore, some participants note that the existence of information analytical data silos within organizations prohibits leaders from making informed decisions in an efficient manner because they’ll have to approach different teams to obtain a small portion of a holistic solution.

Dated digital tools. Some participants emphasized the constraints they face internally in achieving better costing measurements. For instance, due to the limitations of software currently in place in some participants’ organizations, their finance teams were unable to account for costs by providers. Even though they were fully aware that Medicare patients typically incur higher costs due to higher utilization of many resources and functions than younger commercial patients do, the current software doesn’t provide the necessary functionality for them to capture the information that presents the differences.

For example, two patients placed in hospital rooms with the same room rate (i.e., price charges per day) can have completely different severity of illness or medical conditions (known as patient acuities), a parameter generally used in determining staff allocation and justification of budgeting projections. Because the software doesn’t differentiate between the resources these two patients consume, there’s no difference in room rate charges and average cost per patient, which is usually used for major decision making. This causes imprecision in costing measurement. The lack of such functionality also prohibits the organization from deploying advanced costing systems such as ABC.

Other participants also shared concerns about the hurdles their software systems create in processing and generating real-time data. For instance, one participant mentioned that, on certain costing calculation and allocation procedures, their system tends to be fast early in the year and slow and sluggish toward the end of the year when more data is loaded into the system, making it more difficult to perform enhancements at the same time as processing data.

BEYOND COSTING

In addition to the well-established focus on cost management, it’s important to acknowledge that the management accountant’s role in value delivery extends beyond costing to revenue and profitability analysis. To understand the role the finance function plays in revenue and profitability initiatives within the organization, we invited study participants to share their experiences as well as those of their teams. Key findings emerged in the areas of revenue management, performance analysis and measurement, and capital investment decisions.

Revenue management. Price charge modeling has been adopted as an effective tool to manage revenue in the healthcare industry. The finance function engages in the modeling of price increases by, for example, examining the acquisition costs of supplies and monitoring price fluctuations of these supplies in accordance with changes in charge codes and other pricing factors.

Performance analysis and measurement. Finance and accounting teams are regularly engaged in the measurement and analysis of profitability. As one participant shared, whether and how to use the word “margin” in accounting reports is heavily influenced by the finance function given the differences in definition and calculation of various margins that capture different aspects of performance. For instance, the margin calculated as revenue minus direct costs presents distinctive information not fully captured by contribution margin, which is the difference between revenue and variable costs. The finance function is in a unique position to advise on the utilization of appropriate performance measures in accounting reports. Other participants also highlighted that their teams were consistently involved in profitability analysis at the division level (e.g., hospitals at various locations) within their healthcare systems.

Capital investment decisions. According to several study participants, their finance functions are involved in the decisions of all capital investment projects, including building a new hospital site, starting a new clinic, purchasing new equipment or machinery, and so on. The finance and accounting teams are invited to discuss, for example, whether there’s demand in the market for the new site to be built, if the reimbursement is appropriate to cover the costs, what the true costs will be, or what changes are needed to existing operations to enable the success of the new business or initiative. Insights from the finance function have proven invaluable in these strategic decisions.

STRATEGIC BUSINESS PARTNERING

All roundtable participants concurred with the notion that the demand of the finance and accounting function in healthcare organizations extends beyond the traditional financial reporting and planning role that finance and accounting teams have historically played. In addition to reporting and planning, the finance function plays a significant role in financial analysis and operations management (e.g., supply chain management), driven by an increased demand for informed strategic decisions enabled by advanced data analytics.

According to one of the roundtable participants, in the past few years, their organization’s finance function has been engaged in supporting groups across the organization on the interpretation of financial data and the utilization of such data for various operational decisions. In the healthcare industry, there’s also a tendency to split the finance function into two parts. While one part still focuses on traditional accounting and reporting, the other part is more strategy-oriented and emphasizes the prediction and forecast of future scenarios.

Other participants shared that the finance function has been deeply involved in the intelligence side by, for instance, developing tools to capture and manage real-time labor cost data during the COVID-19 pandemic when there was a shortage of care providers in their hospital system. Often, the finance and accounting team is required to generate and provide insights efficiently, sometimes in real time, rather than on a monthly or quarterly basis through standard reports. This value delivery is achieved by being agile, ensuring the accessibility of data, and translating data into true insights that senior leadership and other teams can leverage.

When asked whether the role of the finance function has evolved, most participants did confirm that the finance function now “has a seat at the table” and is viewed as a strategic business partner. For instance, as stated by one of the roundtable participants, their finance function has been involved in strategically directing care services to the right population informed by data and advanced analytics.

As we sought to identify specific ways in which healthcare finance and accounting teams could step more into their role as strategic business partner, we identified three key opportunities: increasing focus on revenue and profitability initiatives in the ways our roundtable participants are currently doing (as described earlier), contributing to lowering healthcare costs, and contributing to improved health equity outcomes.

Lowering healthcare costs. Roundtable participants discussed opportunities to contribute to healthcare costs (to the patient) in two contexts: (1) lowering drug prices through the 340B Drug Pricing Program and (2) bringing attention to cost-effectiveness.

The U.S. federal government’s 340B Drug Pricing Program aims to provide more affordable care by requiring manufacturers to supply eligible healthcare organizations and covered entities with drugs at significantly lower prices. Several study participants acknowledged that their organizations are participants of this program. They highlighted the importance and effectiveness of utilizing the 340B program to lower healthcare costs to patients in general and suggested that the finance function bring visibility of such opportunities to doctors, physicians, and other care providers in their systems to continue to drive patient savings. Through this opportunity, management accountants would play an influential role in adoption and implementation of strategy that benefits the end user of the organization’s products and services—the patient.

When it comes to bringing attention to cost-effectiveness, finance and accounting teams have access to an abundance of financial and nonfinancial data and are increasingly serving in decision-support roles. Some participants recommended that the finance function bring to the attention of senior leadership teams cost-effectiveness as it pertains to, for instance, in which location to conduct certain procedures (e.g., performing a minor procedure in a major academic medical center that’s heavily staffed will incur higher costs, which is not considered cost-effective). Others suggested a more patient-focused approach to classify indirect costs, as opposed to allocating them to overhead, to improve information transparency and subsequently achieve cost-effectiveness.

Improving health equity outcomes. According to the Centers for Disease Control and Prevention (CDC), health equity is defined as “the state in which everyone has a fair and just opportunity to attain their highest level of health.” Health equity can be achieved by eliminating health disparities attributable to social and economic determinants, such as race or ethnicity, sexual identity, age, disabilities, socioeconomic status, or geographic location. How can management accountants contribute to improving health equity outcomes?

Although this is a relatively new and under-explored area among finance functions, some organizations have started initiatives and provided training to leadership teams on health equity issues, and there is a role management accountants can play in addressing health disparities. One participant working for a large healthcare organization said their finance function helps support initiatives to establish freestanding clinics in a major metropolitan city. As in other major cities in the U.S., a large Medicaid and self-paid population exists in the inner city where there are food deserts and a lack of accessible care. Their organization partnered with places that are willing to establish clinics in their sites to help manage front-level care, including dental services, flu shots, wellness checks, and other basic screenings.

The finance and accounting team has played an important role in these endeavors by supporting the decision from a data-driven finance perspective, such as quantifying the investment and donation needs for these initiatives, illustrating their financial benefits, and optimizing the choice of sites based on the data of population health, demands for quality care, and so on.

Other initiatives toward health equity shared by participants include a street nurse program, in which nurses are paid to provide care to the homeless, and a small pilot program that allows patients to receive care in their homes. Both programs are rewarding because they’re implementing a path to maintaining the health of the population in the community—at relatively lower costs—while preventing critical illnesses that could be extremely expensive to treat. In these instances, management accountants played integral roles in evaluating the feasibility of establishing the programs; developing and maintaining fiscal plans; and quantifying the financial, economic, and societal value of these programs relative to alternatives.

DRIVING CHANGE

Our research reveals growing business demand for finance functions to deliver greater value through efficient data analysis and strategic insight generation. Some finance teams meet this demand by playing leading roles in cost and revenue management, performance analysis and measurement, and investment decisions. Yet many healthcare finance and accounting teams face limited resources within, underpinning, and surrounding their functions to deliver this value well beyond the traditional accounting, costing, control, and reporting scope. Outdated systems, data integrity and access, scarce human resources, and limited leadership bandwidth pose challenging barriers to modernization initiatives. Further, even in instances during which finance functions are meeting demands, broader contributions to macro-level initiatives such as lowering healthcare costs to patients and health equity remain largely untapped by finance functions.

While there remain prevailing challenges with respect to costing practice improvements, the finance function’s seat at the table alongside the opportunity and demand to deliver value persists. Healthcare financial management professionals are encouraged to consider adopting approaches employed by some of their peers as described herein, commence digital modernization journeys, upskill teams to ensure they’re equipped with necessary data analytics competencies, and embrace their role as strategic leaders—stepping beyond the bounds of financial data toward societal impact. In such a critical industry, management accountants are playing an important role in the tightrope walk between costing and value delivery to society.

April 2023