What is the financial value of a brand? How can companies find better ways to measure and manage this financial value? How does a brand create value for both its customers and for the company? These are important questions CFOs and management accounting professionals can address by understanding the latest thought leadership about the financial value of brand.

BRAND AS A BUSINESS ASSET

There’s a move underway to change how companies treat the financial value of brand. Several organizations, including the International Organization for Standardization (ISO), the Marketing Accountability Standards Board (MASB), the International Trademark Association (INTA), the Licensing Executives Society International (LES), the American National Standards Institute (ANSI), and, to a lesser extent, accounting and regulatory bodies, are all seeking to address a long-standing need: to better understand and measure the financial value of brand.

The strategic role of the finance organization is to deploy assets and resources for the best business returns and to manage risk. Marketing strives to make the case for an increasing array of marketing activities. These have grown from traditional functions such as sales, distribution, advertising, and sales promotion to also include social media, content marketing, partnerships, customer relationship management (CRM) systems, websites, mobile apps, and more.

It’s the responsibility of the finance department to bring a skeptical eye to marketing expenditures and to question their value for the enterprise. This can sometimes result in a somewhat adversarial relationship. Finance and marketing don’t speak the same language. Whereas a marketer might point to a “Net Promoter Score,” finance is more concerned with cash flow, return on investment (ROI), margins, and asset turns. CEOs are left suspecting that half their marketing funds are unnecessary, but as the old John Wanamaker quote goes, they just don’t know which half. So they become frustrated with the marketing function.

MARKETING’S STRATEGIC ROLE

As much as marketers try to justify expenditures with things like marketing mix and multi-attribution models, trying to determine financial returns is inherently difficult. It may be time to try another approach. Rather than treating marketing only as a set of functional activities to be justified separately, we should view some of these activities in terms of their strategic and financial contribution to the value of the business as a whole. The strategic role of marketing is to create brands that add value for consumers.

Finance should recognize that brand is about value creation. Brands exist in the minds of targeted customers. They aren’t something a company owns. A brand is the value that a customer adds to the intrinsic value of a product. Any product will have some intrinsic value due to the quality of the product. This can be thought of as the product’s objective or productive value. But the way consumers perceive the product and think about the product can add subjective value to this intrinsic value. A diamond is a rock, but for consumers it can be a symbol that a relationship is “forever.” This added value translates into a price premium above what the consumer would pay for an unbranded product.

Marketers often speak of brand value as “brand equity.” This can be misleading, however, in that it might be taken to imply that the “equity” belongs to the company. But the equity is the consumer’s idea of the product, their associations with it, the story they tell themselves about the product, and their experience of engagement with it. Marketing helps the consumer create this equity, but it resides with the consumer. Although marketers can own things like a trademark, the trademark is only a legal protection; it isn’t the brand.

BRINGING FINANCE AND MARKETING INTO ALIGNMENT

Although the company doesn’t own the brand, it has substantial control over it. And having control of something as a result of past events that leads to the expectation of future economic benefits is the International Accounting Standards Board (IASB) accounting definition of a business asset.

To be sure, a brand is an intangible asset in that it has no physical substance, including not becoming cash in a year. Nonetheless, a strong brand has value to the consumer and accordingly can be expected to generate financial value to the company over time. Thus, the brand is an intangible financial asset for the business that controls it.

Once viewed in this way, finance and marketing can achieve strategic alignment. Yet determining the asset value of the brand is a knotty issue. We shouldn’t let this technical difficulty obscure the important insight that viewing brand as a financial asset can give marketing and finance a common strategic focus.

ACCOUNTING TREATMENT OF BRAND

Accountants have long resisted treating brand, as well as other intangibles, as an asset because of the difficulty of relying on the “fair value” of a market transaction. In the case of an acquisition, the price of the acquired company can be used for brand valuation. In the case of a brand created internally, however, valuation becomes difficult. Accountants have preferred to expense marketing activities with the possible exception of trademarks and the ever-nebulous “goodwill.”

The ISO 10668 standard in 2010 (“Brand Valuation—Requirements for Monetary Brand Valuation,” available at www.iso.org) did outline some accounting-based methods, but in the face of resistance from traditional accounting practices, this standard hasn’t received much attention. What is needed is an empirical way of going from the strength of a brand for consumers to the financial value of the brand to a company. Marketers have many metrics to assess brand (awareness, etc.), but these don’t fully indicate how strong the brand is in affecting consumer choice. Performing well on these metrics doesn’t necessarily translate into a brand that performs as an economic resource to the benefit of a company.

BRAND STRENGTH

A number of consulting companies have developed models for going beyond traditional marketing metrics to evaluate brand strength. Kantar Millward Brown, for instance, uses its BrandZ model, which is based on marketing research surveys of consumers, to estimate the percentage of consumers who are highly behaviorally committed to the brand. This “brand contribution” is applied to a forecast of future discounted earnings to determine the value of the brand. As with the models of other companies, such as Interbrand, these models aren’t very straightforward and are based only on publicly available data. Nor do the rankings of brands in their different published lists of top brands agree very well.

A new standard, ISO 20671 (“Brand Evaluation—Principles and Fundamentals,” available at www.iso.org), provides a simpler framework for evaluating brand. Although a number of specific methods could be used, the key principle is to compare choices between a brand and a comparable unbranded or weakly branded product where the choices also vary on price and possibly other factors. This allows the contribution of brand to be evaluated relative to an unbranded benchmark. Ideally this evaluation would be conducted over time in order to assess change. The vision behind such a straightforward and transparent evaluation process is that it could become part of the movement to integrated reporting (IR).

Initially a company could experiment with different methods. After a company settles on a specific method, the contribution of the brand could periodically be publicly reported. Such reporting would have many advantages. First, it could provide marketing and finance with a common focus. Second, treating the brand as a financial asset could play a role in corporate governance without having to be part of any traditionally U.S. Securities & Exchange Commission (SEC)-related reporting.

An increase or decrease in brand value would be a matter of accountability. Evaluating brand value would also be useful for risk management in guarding against brand and reputation risks. Third, investors would have access to an important piece of financial information that they presently can only guess at. This might help both companies and investors move away from earnings calls. Market caps might better reflect identified business assets. Over time, standards could be developed to make it easier for investors to compare companies. As intangible assets become more and more important, this would help investors distinguish leading companies from those not investing in brand as a valuable business asset.

A BRAND VALUE SYSTEM MAP

A brand value system map can be useful in creating an ongoing brand evaluation and valuation process (see Figure 1). Using this approach, brand value should be considered in terms of specific steps in the value creation-value capture process. There are three main steps. The first two are internal and are about running the business. The third is external.

Click to enlarge.

- Brand value for consumers is created, and marketers assess the health of the brand using metrics and key performance indicators (KPIs) such as awareness, favorability, purchasing intentions, engagement, etc.

- Brand intangible asset value is where the consumer brand value needs to be translated into a financial value for the company. This step shouldn’t be confused with brand valuation. As called for by ISO 20671, brand evaluation methods are required for this step. There is growing recognition of its importance.

- Brand valuation is about establishing the worth of the brand for external purposes such as selling or licensing trademarks and IP. Traditional brand valuation methods are most relevant to this step.

To move forward with systematically organizing a brand evaluation process, discussion of the specific steps in the map could improve understanding and avoid confusion.

THE NECESSITY OF CHANGE

Changing the long-standing culture differences between finance and marketing relative to brand value is challenging. At the same time, the forces compelling change can’t be ignored. Brands will only increase in their importance for competitive advantage. Companies can’t simply depend on large expenditures for advertising to create strong brands. Ad avoidance and skepticism are decreasing the effectiveness of conventional advertising. Symptomatic of this is increased competition of consulting firms such as Accenture Interactive and Deloitte Digital with traditional ad agencies.

Brian Whipple, CEO of Accenture Interactive, was recently quoted in The Wall Street Journal as saying that Accenture wouldn’t pitch advertising to an automobile company, but it would help the company reinvent the car-buying experience. This is precisely because consumers increasingly value brands that engage them with experiences that connect to higher-order social values or life goals rather than merely promising different product-related benefits. It’s only by treating brand as a financial asset and investing in it accordingly that companies can meet the true challenge to competitive growth in the future: building a strong brand through meaningful actual and mediated consumer experiences.

KEY TERMS ABOUT BRAND

These key terms can help CFOs and management accountants speak the same language as the marketing department when analyzing the financial value of a brand.

Brand: Distinctive images and associations in the minds of stakeholders that generate economic benefit to an organization.

Brand Equity: The value of the brand in the consumer’s mind. There is no universally accepted way to define this, but it can be taken to refer to any (one or more) metrics that marketers use to define the meaning of the brand in the hearts and minds of consumers (e.g., awareness, favorability, purchase intention). As described in ISO 20671, “Brand Evaluation—Principles and Fundamentals,” these metrics or indicators can cross a variety of dimensions—consumer, market, consumer financial, legal, and economic/political—all assessing the underlying health of the brand.

Brand Strength: Sometimes referred to as brand preference or brand performance. It’s a nonmonetary, point-in-time measure of how brand equity is reflected in the actual choice of branded offerings. It can be taken as a benchmark comparison between the choice of the branded product over an unbranded or weakly branded product in the same category.

Brand Evaluation: A monetary estimate of the contribution of the brand to some aggregate financial metric such as revenue or cash flow. It’s intended to reflect the worth of the brand from an internal perspective reflecting the brand’s contribution to running the business.

Brand Valuation: A monetary estimate of the worth of the brand from an external perspective often reflecting the market value of the brand.

Brand Value: Any monetary estimate that translates consumer brand equity into the worth of the brand as a financial asset for an organization. It’s important to specify whether this is from the internal perspective of operating the business or from the external perspective of market valuation, as with M&A activity or licensing.

A CONVERSATION ABOUT BRAND VALUE

Bobby J. Calder and Mark L. Frigo offer a closer look at the financial value of brand from the marketing and finance/accounting perspectives, respectively.

Strategic Finance (SF): Marketing and finance speak different languages. How can we define key terms that would help with communication between the two functions?

Marketing/Calder: Different marketers use terms differently, and many common terms are often vaguely defined. Starting with some definitions might help (see “Key Terms about Brand” above). These draw on the Common Language in Marketing Project, an effort to promote consistent terminology (available at www.marketing-dictionary.org), and on my own thoughts about using terms in a way that corresponds to the brand value system map.

Finance/Frigo: Understanding the key terms underlying the financial value of brand is a first step for CFOs in this area. Shared terminology would allow CFOs and management accountants to use their financial acumen to work with CMOs in increasing brand value.

SF: There are a number of well-publicized brand rankings published yearly by BrandZ, Interbrand, Brand Finance, Forbes, and others. What are some of the limitations of these rankings that CFOs and management teams should consider when reviewing them?

Marketing/Calder: Rankings are published by a number of organizations besides BrandZ. Interbrand, which is affiliated with Bloomberg, bases its rankings on a number of brand “drivers” such as market share, customer loyalty, share of advertising voice, and level of legal protection. Brand Finance also employs consumer research and considers factors related to marketing investment, stakeholder equity, and business performance.

The European Brand Institute, located in Austria, uses factors such as competition, market position, investment, and potential. Every company has its own proprietary model of brand value, and each one is different. In all, there have been 40 or so of these models developed. On the positive side, the rankings stimulate interest in brand value. Their limitation is that none of the models stand out as more valid than the others.

Finance/Frigo: CFOs are certainly aware of the various brand rankings but are reluctant to use them. From a financial and accounting point of view, it makes more sense to get out ahead of the growing interest in measuring brand value and take the lead in developing this capability internally.

SF: ISO 10668 “Brand Valuation” presents a number of approaches for valuing brand. How can those be used by CFOs and CMOs?

Marketing/Calder: This standard covers three main approaches to brand valuation. One is the market approach that values a brand against the price of a comparable brand. Another is the income approach that uses the present value of future cash flows that a company would receive due to using the brand. A hybrid approach is royalty relief. It’s based on the royalties a company would have to pay if it had to license the brand from another entity (market). The future royalties are discounted to give the present value of the brand (income). Although versions of these methods are used in valuations, the standard itself hasn’t received a lot of attention, although a related Austrian standard (A 6800) is used in Europe.

I think the important thing going forward is to tie brand valuations more explicitly to brand evaluations. The income method can be used with measures of brand strength to determine the contribution of the brand.

Finance/Frigo: A 2015 article in Strategic Finance (“Brand Value: ‘Hidden’ Asset in Plain View”) presents royalty relief as a simple approach where the only issues are the choice of royalty rate and discount rate. It should be realized, however, that the value of the brand for a company that licenses the brand isn’t the same as the value of the brand for a company’s own internal business operations. It’s that value, the left side of the brand system value map, that counts in running the business. Companies really need to distinguish brand evaluation methods from brand valuation methods.

SF: The MASB is working to help companies understand the value of their brands. How can this work be used by CFOs and CMOs?

Marketing/Calder: MASB (themasb.org) has been charged by the ANSI with forming a committee to represent the United States before the ISO committee (TC 289) that I chair. The ISO committee is developing standards for brand evaluation and valuation. China and the U.S. are the co-conveners of the international committee. And I might add that China’s Council for Brand Development has been very active in serving as the secretariat. It holds a national event, “Brand Day,” each year on May 10 to promote this work.

MASB has labeled the recently published standard ISO 20671 as the “golden ticket” for marketers in that it helps marketers to make the case that brand should be treated as a financial asset and not a cost. MASB is actively engaged in providing guidance to companies in implementing a brand evaluation process.

MASB has also conducted original research to demonstrate that brand strength contributes to financial return. A study sponsored by six major corporations found that a choice measure of brand strength explained 75% of the variation in unit shares of brands across multiple brands from diverse categories.

MASB’s biannual summit is an important forum for company representatives and academics to hear about and discuss initiatives by companies.

Finance/Frigo: A good idea would be to have both a finance person and a marketing person in your company jointly contact MASB for more information and use this information to co-create a strategy for understanding and measuring the financial value of the company’s brands.

SF: IR is an important development in accounting and governance with reports on sustainability and other areas. What would be the advantages of including the financial value of brands in IR?

Marketing/Calder: In my view, it isn’t likely that brand value will make it on the balance sheet anytime soon. IR offers a way around this. It certifies that the information is important but doesn’t require meeting accounting standards.

Beyond this, IR is predicated on the concept that businesses create different kinds of capital outputs. Some of these are related to sustainability, which is closely identified with IR. But other kinds of capital are relevant. Brands might well be considered social capital in that value is created for consumers. And as brands seek more and more to engage consumers in a sense of shared social purpose, the fit with IR as a reporting vehicle will become even better in my opinion.

That said, a company could use notes or other reporting vehicles. The main thing to keep in mind is that brand value is important, high-level information about the performance of the company. It isn’t a business secret. It should be part of the face of a public company.

Finance/Frigo: IR is an area where the financial value of brands would be particularly useful. One of six capitals in IR is “intellectual capital,” which includes brand and reputation. Intellectual capital includes intangible assets based on knowledge, including intangibles associated with the brand and the reputation that the company has developed.

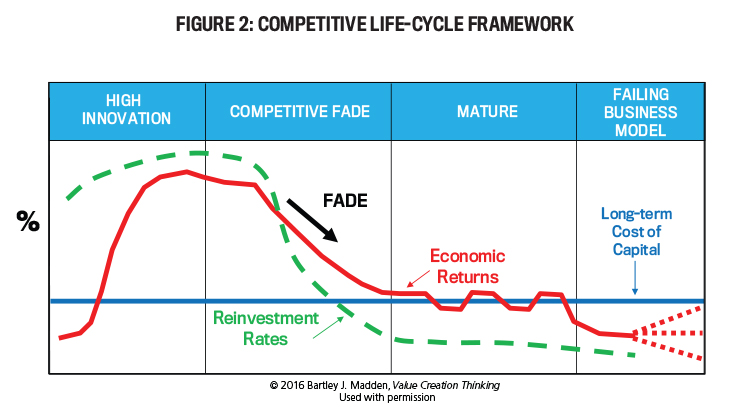

SF: How can CFOs and CMOs determine the best strategy for investments and reinvestments in brands based on a competitive life-cycle (CLC) analysis?

Finance/Frigo: The DePaul Center for Strategy, Execution and Valuation’s research on high-performance companies is based in part on identifying companies that have resisted the competitive “fade” phase in the “competitive life-cycle” of a company (as outlined in Bartley J. Madden’s 2016 book, Value Creation Thinking) and studying the performance of companies in terms of economic returns (return on net assets, cash flow return on investment, return on capital, etc.), growth in invested capital, and relative total shareholder returns. The competitive life-cycle concept describes a distinct relationship between reinvestment rates in the company and its performance in terms of ROI (economic returns) during four phases: high innovation, competitive fade, maturity, and failing business model. The reinvestment rates are the economic resources invested, and they reflect the innovation and growth strategies of a company. (See Figure 2.)

Click to enlarge.

Companies can resist the tendency to fade by making value-creating reinvestments that build capabilities that extend competitive advantage. The Center for Strategy, Execution and Valuation is experimenting with how CFOs and management teams can use strategic life-cycle reviews to evaluate how investments can help companies resist the competitive fade. According to Madden, “management teams can experiment with tough measurement issues like intangibles (including brands) as part of this life cycle review process.”

Marketing/Calder: Brand can of course contribute greatly to the initial growth stage of a company. In many cases, brand strength may increase faster than revenue (Tesla, for example). But brand can be equally important when it comes to life-cycle fade. At some point, the growth resulting from initial investments in innovation plateaus. And this is where competitive fade can set it. New investment is needed, but there is uncertainty as many investments may lie outside the competencies that produced the original growth. Companies often react by buying back stock instead of investing and by cutting costs to increase earnings (Kraft Heinz, for example). This is where many companies are tempted to cut branding expenditures.

A strategic life-cycle review, however, would consider accumulated brand value as a resource that with continuing investment can lead the company to new business opportunities as much as technological innovation can. Brand represents a readiness of consumers to perceive new offerings as valuable. In financial terms, brand has a real options value that can make launching new products or services more profitable.

Finance and marketing often act at cross-purposes. Marketing focuses on justifying expenditures, and finance focuses on reducing them. Both should instead focus on increasing the financial value of brands as a key company asset. Recent advances in brand evaluation and valuation are making it possible for finance and marketing to take the lead in recognizing the potential contribution of brand to financial results.

This article is part of the Creating Long-Term Sustainable Value series begun in the October 2018 issue of Strategic Finance with “Creating Greater Long-Term Sustainable Value” by Mark L. Frigo with Dominic Barton.

October 2019