Taking a more theoretical approach, however, shows students a more sterile view of accounting than they will encounter in the real world. Many instructors and developers make efforts to incorporate realistic elements into their classes so students are better prepared to begin their careers. By using case studies, inviting practitioners to speak in the classroom, taking students to on-site visits, and involving students in simulations, instructors can give their students a better, more complete understanding of what the job of an accountant actually entails and the problems they might face when working in one of those jobs.

As an instructor in cost and managerial accounting courses, I enjoyed introducing elements of realism into my classroom, but I always wondered if they went far enough. When I got the opportunity to develop a senior-level, advanced managerial accounting course at Iowa State University, I made an effort to design the course in a way that it would bridge the gap between the classroom experience that students are accustomed to and the on-the-job experience they might encounter after graduation.

A NEW COURSE

I first came up with the idea for my Advanced Managerial Accounting course 10 years ago after attending a meeting of the Iowa State accounting department’s Accounting Advisory Board. Board members at that meeting were asked about the skills they were looking for when they hired our graduates. Their response was that they were happy with the students’ knowledge, but they wanted more soft skills. They wanted employees who could work well with each other and who could communicate well in various settings—written and oral, formal and informal. They also wanted flexibility. They believed our graduates understood what they had learned in class but had difficulty applying that knowledge in situations that weren’t as clear-cut as the scenarios in their classes.

As I listened to our board members, I realized that the idea of a course that emphasized communication really appealed to me. As an undergraduate, I had majored in English and broadcasting, so I had a good background to teach such a class. I began to develop a course that addressed all the points the board had brought up: communication, teamwork, and flexibility. As I worked on the course, I kept in mind that I wanted the students to work in an environment that was closer to what they would experience in a job than what they’d so far experienced in the classroom.

TEAMWORK

I always include group work in the classes that I teach, but for this course, I wanted to take teamwork a step further and have students work in teams for the entire semester. You don’t always get to choose who you work with on the job, so I decided to form the teams myself using a skills inventory that students filled out. They would rate their abilities in a variety of areas, including accounting, math, writing, speaking, design, and leadership. I would then build the teams by trying to balance these skills, ensuring that each team had someone who rated themselves highly in each area.

One ubiquitous problem with working in groups is freeloading, which is when members of a group don’t contribute their fair share of the work or effort. I thought about how this freeloading would be addressed in the workplace: If someone doesn’t put in enough work over time, eventually he or she will end up with lower pay, fewer opportunities for advancement, or a lost job. To simulate this environment, I required each team to develop two policies: a point-sharing policy and an employment policy.

After each project, I would reward points to the entire team, and the team would then split those points among individual members according to its point-sharing policy. In effect, the points were their paychecks, and I gave the teams the autonomy to distribute those paychecks however they liked. The fact that they had to develop and follow a policy meant that the whole team had to agree on how points would be shared and that they couldn’t take points away from someone arbitrarily. Having such a policy gave the teams one tool for dealing with the freeloading problem on their own.

The other tool the teams had was the employment policy, which described how and when team members could quit, be hired, or be fired. With these policies in place, the class operated as an open labor market, giving teams another weapon against freeloading as well as a way to deal with personality conflicts. I felt that empowering the students to deal with these problems was good for both the students and me—it would give them experience they could draw on in their future careers, and it would save me the hassle of trying to solve their problems myself.

COMMUNICATION

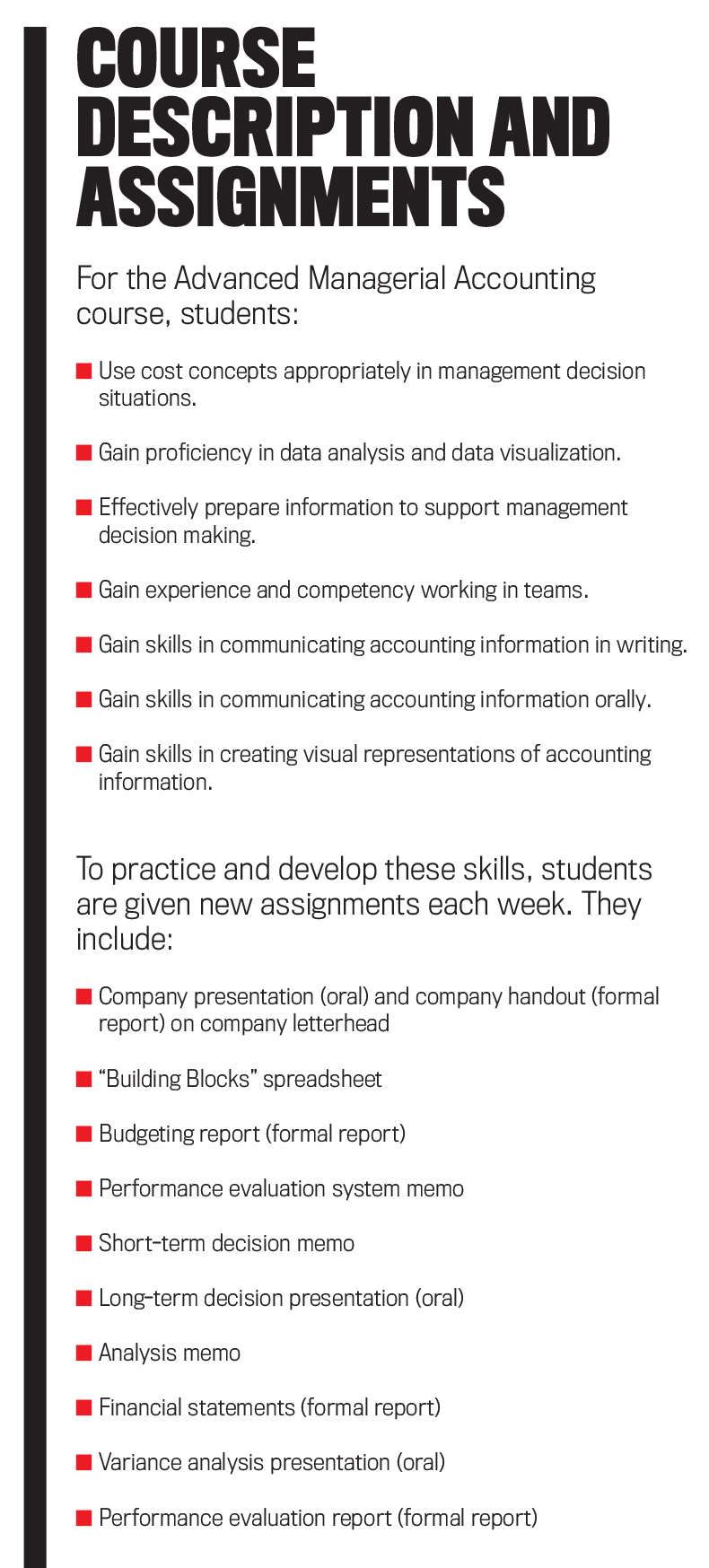

To emphasize communication in the course, I again decided to take a more extreme approach than I’d used in previous classes. Half of the grade on every project would be based on communication (with the other half based on content), and every week there would be a project that required a communication deliverable, such as a memo, report, oral presentation, and so on (see “Course Description and Assignments”). I wanted to give the students ample opportunity to practice and improve their communication skills in a manner that would help me measure their progress across multiple assignments.

To encourage improvement, I decided to give each team extensive feedback on their communication as well as their content. I prepared rubrics for each type of assignment—oral report, formal written report, and memo—that served as both a grading tool and a list of categories I should be sure to give feedback on. Throughout the course, I would look for improvement in the areas where I indicated they needed work, and I would incorporate that improvement into the course grades.

I knew that, in some groups, everyone would participate in creating the communication each week while in others the best writers or speakers would take on most of the communication work. I decided that this was fine with me. While all individual students may not improve their personal communication skills over the course of the semester, they would at least witness the process. I felt that the realism and experience of a team environment was more important than ensuring that every student was evaluated on individual work.

FLEXIBILITY

One important aspect of the course for me was that it should build students’ flexibility. For example, one of the class assignments is for the teams to put together a company budget for the following year and prepare a formal written report suitable for presentation at a board meeting. It’s one thing to know how to put together a budget when your instructor has shown you a step-by-step procedure and given you the numbers you need to use in your calculations, but it’s quite another to be told to prepare a budget suitable for presentation at a board meeting without any specifics as to what format to use or what level of detail to include. I wanted the students to experience the realism, uncertainty, and freedom that comes along with open-ended, ill-structured assignments because accounting is often messier in the workplace than it is in the classroom.

I also wanted the students to experience finding numbers rather than being given numbers. This would require the estimation and guesswork that sometimes occurs in more realistic situations. Therefore, each team had to come up with the revenues and costs they used in the class based on their own research—information they could obtain from a variety of sources, including family, friends, personal experience, books, magazines, or (mostly) the internet. Any numbers they used had to be realistic, reasonable, and consistent from assignment to assignment.

THE FINAL PROJECT

My department chair liked my proposal for the course and wanted to open it to both seniors and graduate students. To do so, I had to find a way to make the graduate experience different from the undergraduate experience while keeping both kinds of students in the same classroom. One way I could do that was to encourage the graduate students to take a leadership role in their teams, but the curriculum needed to differ as well. Since I also wanted to include at least one individual assignment, I thought that making the individual assignment different for the two groups of students would be the ideal solution.

For the graduate students, the final assignment in the class would be an individual oral presentation. Each student would interview someone from a small or medium-sized business, then give a presentation on that business’s managerial accounting practices. The undergraduate students would be the audience for the presentations, which would serve as the basis for their own individual assignment: an essay about how managerial accounting practices differ in the real world from what they’d learned in their managerial accounting classes, including this one.

I wanted the graduate students to focus on small and medium-sized businesses because the techniques they’d learned in their classes are often most useful in large businesses, where different people within the organization need to communicate with each other and understand the financial implications of decisions made across the organization. As businesses get smaller, that need diminishes, so managerial accounting practices will also differ—or not exist at all. Since I wanted the students to realize that accounting in practice is more ambiguous than it is in the classroom, I thought that learning about a variety of practices in smaller businesses would be a good way to finish the class.

CLASS STRUCTURE

Because students had to complete 11 major projects during the 12 weeks of class in an environment that wasn’t defined well and where they had to do research, planning, and writing in teams, I decided to completely do away with the traditional classroom fixtures of lectures and exams. I felt that the students would learn a great deal just by applying techniques they’d learned previously in new ways and by researching and using new techniques on their own for topics they hadn’t encountered. So apart from oral presentations some weeks, as well as a few mini-lectures on communication techniques, all the class time would be spent on group work. I would be available to answer students’ questions during class, and I could also use that time for grading.

HOW THE CLASS HAS CHANGED

The first time I taught the class, I was amazed at how long it took to grade the students’ projects. There was so much to think about: Were their numbers reasonable? Did they apply the techniques correctly? Grading managerial accounting work without an answer key was certainly a challenge, and that was only half the grade!

For the other half, I was thinking about things like grammar, spelling, sentence structure, organization, tone, and visual appeal if the project was written and things like eye contact, volume, gestures, and transitions if it was oral—these weren’t areas I was accustomed to grading. One of the projects—the budget—was massive but necessary, and grading it took up all my time that week. The others were more manageable but still took more time than I’d anticipated.

As I taught the course again and again over the next few years, I made changes that made life a little easier. I broke up the budget assignment into two parts: In the first week, the teams just came up with the numbers they’d use for the budget report they created in the second week. I made a spreadsheet template for the students to use when they provided their numbers, and that gave me a grading key I could use for the rest of the semester. I also revised my rubrics to include checklists that would better allow me to grade content and communication in a standardized manner and to provide feedback that the students could use to improve on future assignments.

Initially, the course consisted of just one section offered during the spring semester. After three years, it expanded from one section to two, and enrollment kept growing. There were only four groups when I first taught the course. By the time it grew to nine groups, I realized I couldn’t handle much more, so I started asking for class sizes to be capped. The students needed electives, though, and they liked the class, so my requests were denied. In my sixth year of teaching the course, I had 15 groups across two sections, which was way too much; with all the grading, I had almost no time for research that semester.

The demand for the course continued to be extremely high, however, so, rather than cap enrollment, the department chair assigned another instructor to work with me in the class as well as a teaching assistant (TA) who had communications experience. There were 18 groups that semester, and even with three of us grading, we had our hands full. Finally, the following year, the department agreed to cap enrollment in each section and also approved hiring a TA from the English department to assist with communications grading. Since then, the course has become much more manageable.

The TAs from the English department also influenced how I taught the class. They helped me realize that I had been providing the groups with too much feedback. As a detail-oriented person, I felt compelled to point out every area where students could improve. But this was overloading them. The students improved much more once we focused in on a few crucial issues.

My latest TA introduced me to the idea of providing screencast feedback rather than written feedback. Screencasts, which are narrated video recordings of computer screens, are more personal than writing, and they allow students to hear vocal inflections and other verbal cues that enhance what I’m saying. I can also get screencasts finished and distributed to students more quickly than written feedback.

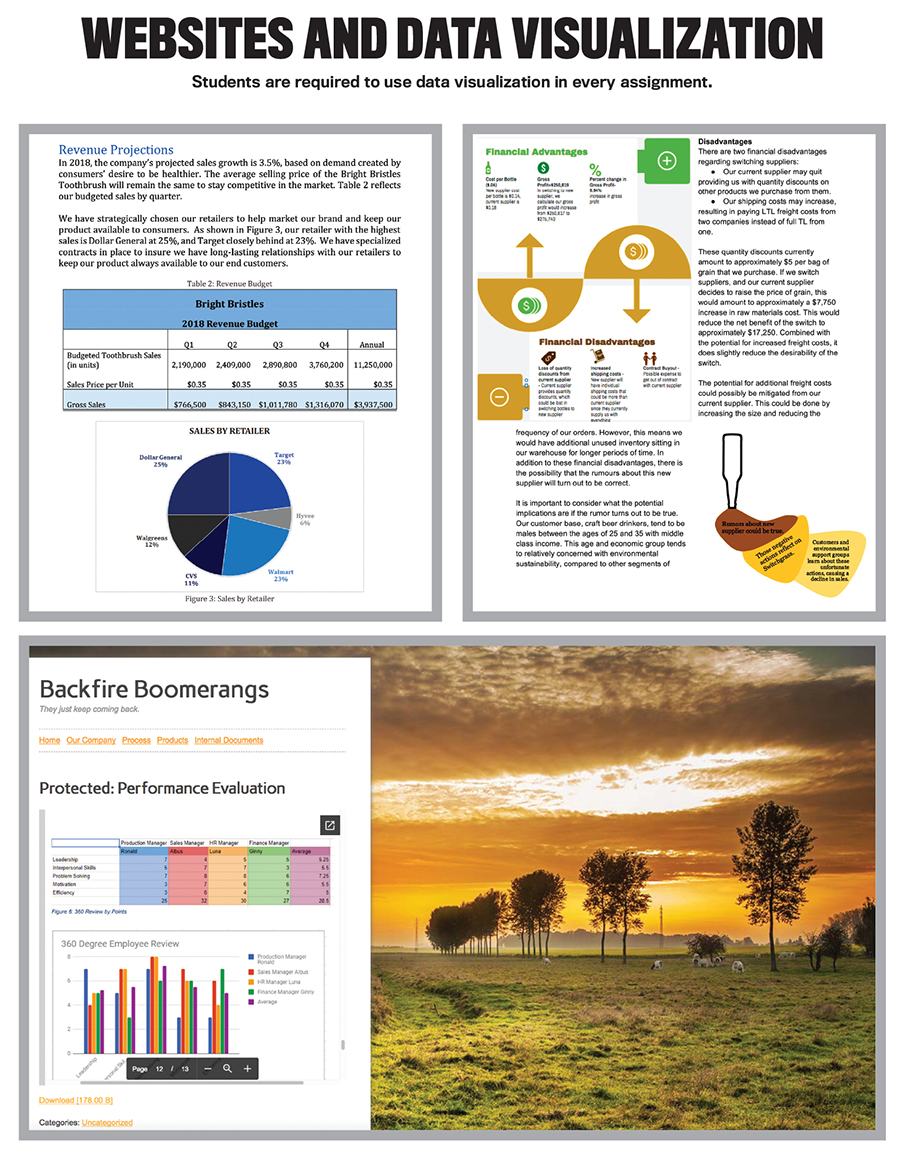

One other way in which the class has changed over the years has been in the emphasis I’ve placed on data visualization. When I started teaching the class, I encouraged students to include charts and graphs in their work because they make data easier to understand than if it’s presented in text or tables. Over the past decade, however, the concept of data visualization has expanded to more than just charts and graphs—now we see infographics, pictures with data overlay, heat maps, hierarchies, and so much more. And we see them everywhere: Data visualizations are included in annual reports, on websites, and increasingly in dashboards to present accounting information within organizations. Accordingly, I have moved from encouraging visualizations to requiring them in every assignment, placing more and more weight on that component of communication (see “Websites and Data Visualization”).

As communication in general has become more digital, so have the class projects. I used to require each assignment to be printed, grading the groups on how professional the printing looked. Now each group is required to build a website for its company and post almost all the assignments there. Only the formal reports are still printed (and also posted on the website).

VALUABLE EXPERIENCE

Despite all these changes, the core idea of the course hasn’t changed—I still want students to experience a more realistic accounting environment than they ordinarily encounter in the classroom. By working with others in a long-term team, creating their own numbers, making their own decisions about what information to present and how to present it, and completing numerous assignments that require them to communicate that information in a way that the user understands and can use it to make decisions, the students get to experience some of the intangible factors that make the workplace different from the classroom.

Most of the students appreciate the experience, too. The most frequent feedback I get from students on class evaluations is that the class is tough but fun—and valuable as well. When I hear from former students, they say that they’re glad they took the class. They felt it helped prepare them for their jobs. And while it often has been a challenge to teach, I enjoy the class as well. It’s very rewarding to see accounting students demonstrate creativity and problem solving on a weekly basis while building skills that I know will be valuable for their future.

October 2018