After the roller-coaster ride of 2020 and 2021 due to the COVID-19 pandemic, companies around the world are eager for a return to more typical operating conditions.

The Q3 2021 Global Economic Conditions Survey (GECS) shows that global confidence, which had dipped significantly in 2020 and early 2021, remains high. And the two “fear” indices that GECS tracks—which are measured by concerns that customers and suppliers would go out of business—declined for the second straight quarter and returned to pre-COVID levels globally.

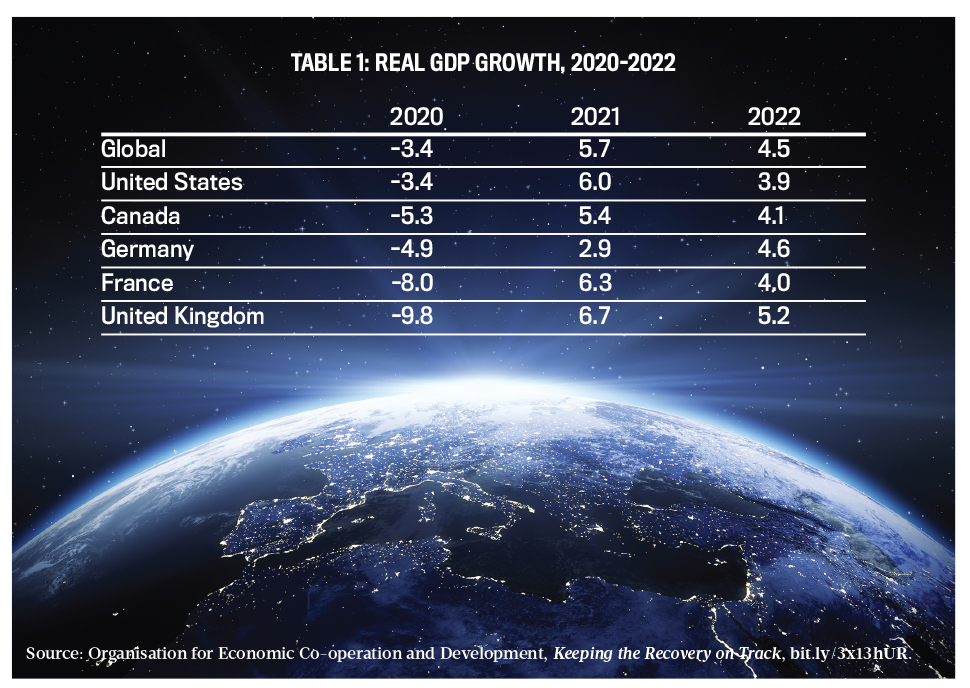

In the United States, consumer demand is expected to return to more normal levels in 2022. According to the Conference Board, real U.S. consumer spending is expected to grow by 3.3% this year, along with an increase of 3.5% in real gross domestic product (GDP). While the U.S. recovery is expected to be slower than other G7 economies, it also didn’t have as far to crawl back from 2020 levels, as reported by the Organisation for Economic Co-operation and Development (see Table 1).

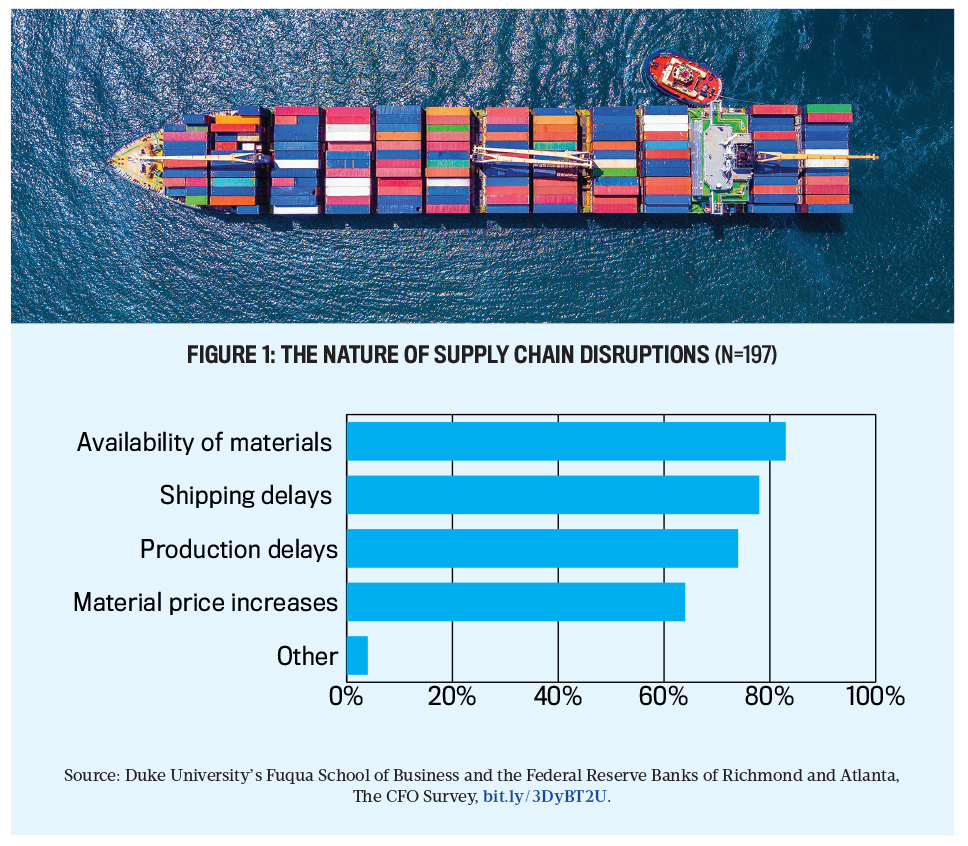

For 2022, trade cost increases for U.S. producers, importers, and resellers remain a concern, as supply chain problems are expected to persist well into the new year. According to Duke University’s Q3 2021 CFO Survey, three out of four U.S. companies experienced disruptions including shipping delays, reduced availability of materials, increased materials prices, and production delays (see Figure 1). Fewer than 10% of CFOs expected these supply chain difficulties to be resolved by the end of 2021, and most respondents anticipate these issues won’t be resolved until the second half of 2022 or later. Those experiencing supply disruption experienced an average 5% reduction in revenue.

Click to enlarge.

The Duke CFO Survey shows that large companies were more likely to be taking action to adjust their supply chains, such as holding more inventory stocks, diversifying or reconfiguring supply chains, shifting production closer to the U.S., or changing shipping logistics. Meanwhile, small companies had less room to maneuver and were more likely to report waiting for supply chain issues to resolve themselves.

“Supply chain problems caught a lot of people by surprise,” says John Graham, professor and survey director at Duke University. “We had a decade or two of Just-in-Time inventory management to keep costs down and also likely sourced from the single cheapest location. Now, CFOs realize that with Just-in-Time inventory management, if something goes wrong in the supply chain, their companies will be in trouble.”

In order to mitigate those risks, companies are diversifying sources and bringing the supply chain closer to home, Graham says. “If you’re a North American company, you’re bringing it back to Mexico and Canada,” he says. “If you’re a U.S.-based company, because of shipping, you’re bringing it back into the U.S.”

LABOR SUPPLY AND SKILLS SHORTAGES

While supply chain disruptions will remain a problem, CFOs are also worrying about finding skilled labor to fuel potential growth at a price their companies can afford. Labor quality and availability are top concerns for CFOs, and attracting and retaining talent is likely to dominate their agendas throughout 2022.

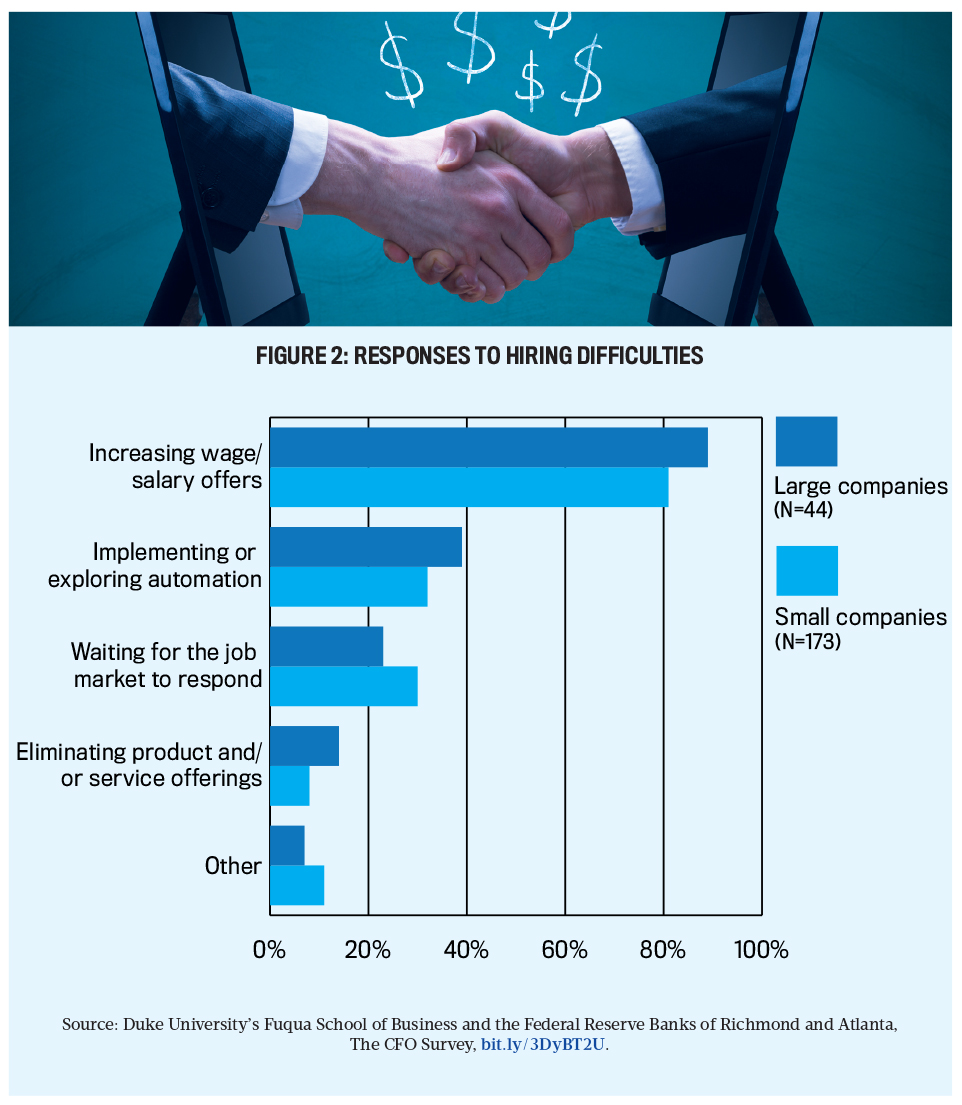

According to the Duke CFO Survey, roughly three in four CFOs are finding it difficult to fill open positions (79% of large companies and 73% of small companies). In response, the vast majority are increasing wages and salaries to attract and retain employees. Thirty-nine percent of large companies and 32% of small companies will be turning to automation to fill the talent gap (see Figure 2).

Click to enlarge.

Graham says companies can’t find the talent they need due to two fundamental problems. “One is the skills mismatch, and CFOs have been complaining about this in an ever-increasing way for years,” he says. “The other is that many people aren’t yet going back to work.”

He further explains that some people are sitting on the sidelines because they’re afraid of COVID-19, some are staying home because they don’t want to send their kids to school, and others have opted out of the workforce altogether. And it isn’t just a cost issue, he says—output has suffered as well. Those companies that were experiencing labor difficulties took a revenue hit of 5%. “That’s a pretty big number. You might’ve seen 15% revenue growth coming back from the recession; now you’re down to 10%, and some companies with anemic revenue growth could potentially be in the black due to staffing problems.”

With companies facing stiff competition in filling open positions for skilled talent, building from within—and retaining high-performing talent—will also be important. As Paul McDonald of Robert Half wrote in October 2021, “Managers should seize the opportunity now to affirm or reaffirm their commitment to each employee’s professional development” (“Invest in Your People,” Strategic Finance). He recommends a couple of tactics to help retain and develop current talent, including conducting a career-mapping exercise with individuals, providing appropriate professional development, and establishing a culture of growth.

AUTOMATION

In order to meet demand and cope with talent shortages, many companies will be turning to technology in 2022. After a brief slowdown in 2020, IT investments are rebounding with renewed automation and digital transformation. Omar Choucair, CFO of Trintech, a Texas-based software company with offices around the world, explains that COVID-19 put a pause on these major digital transformation projects because “many CFOs couldn’t see beyond a one-month forecast.” Today, given the shortage of talent, the only way companies can scale without increasing staff is to invest in technology, he adds.

For finance staff particularly, working from home during the pandemic necessitated automation. “What’s turbocharged our market is that with all this hybrid work and people working remotely on a permanent basis, CFOs turned to technology to ensure business continuity and do the financial close and reporting,” Choucair says. “That’s been a pretty significant tailwind behind us.”

In order to fill its talent pipeline to meet demand in 2021, Trintech took a deep dive into analyzing its competitive position in the labor market. “We’ve really done all kinds of benefit compensation analysis to ensure that we’re market-driven, and we spent a lot of time with our HR leaders to ensure that we get really good talent and are paying them accordingly,” says Choucair, adding that, as to the bottom-line impacts of increasing compensation, “I’m not sure if you can necessarily offset the rising costs of attracting talent. We’re not able to save our way into getting better talent, so the only offset is higher revenue.”

RECRUITING TALENT

Other strategies around attracting and retaining talent that will become the norm in 2022 are more flexible work hours, incentive payments, and longer vesting periods for stock. “What’s new is that we’re seeing a lot more flexibility offered for work from home, along with more signing and retention bonuses, and long-term incentive plans,” explains Judy Munro, senior managing director at Robert Half Executive Search. Companies are also extending typical vesting periods in order to discourage employees from leaving, she adds.

For Vena Solutions, a Toronto, Canada-based software company, the risk of not being able to fill the talent pipeline will ultimately hit the bottom line. “For our company, there are no demand constraints. Any technology, like Vena, that allows people to work from home is exploding,” says Tom Seegmiller, vice president of financial planning. “Our main challenge is scaling and enabling our team fast enough to feed the growth that will ultimately catapult the business forward.” At first it was hard to find good development staff, he explains, “but that’s spread to more areas of the business now, and that’s definitely a risk we’re thinking about in 2022.”

Remote working (see Figure 3) has added a level of complexity to Vena’s employee search. “We’re not exactly sure of what our labor market looks like down the road; there is a lot of uncertainty,” says Vena CFO Darrell Cox. “We used to compete within Toronto, but are we now competing with New York or San Francisco, or London, and what are the inflationary dynamics that are going to dictate employee compensation?”

Click to enlarge.

For finance talent specifically, companies are looking for more specialized skills, Munro says. “Experience in FP&A [financial planning and analysis] is one of the top skills companies are looking for in finance talent, but now the depth they’re expecting is beyond anything I’ve seen before.” Financial analysis has gotten much deeper and broader into all areas of the business, mostly due to the availability of data and business intelligence tools, she adds. And it isn’t just finance that’s benefiting from these skills: FP&A experts are now in high demand across all corporate functions.

“The thing that I’ve seen more of recently is embedding an FP&A professional in the functional areas of the business,” says Munro. “Embedded into sales and marketing, logistics, and supply chain—anywhere the company needs a true business partner.” That’s where FP&A roles have gotten very interesting, she adds. “It’s changing organizational structures.”

THE ROLE OF THE MANAGEMENT ACCOUNTANT

This is good news for management accountants with broad-based business training and an understanding of operations. Today, FP&A is all about finding efficiencies and figuring out where opportunities to improve revenues and profitability lie across the entire company, says Munro, and management accountants are well positioned to take this on. “FP&A professionals are very analytical people,” she adds, “and understand how modern business intelligence tools can extract meaningful data.”

Inherently understanding the operations of the business, building models, and stress testing have been crucially important to Vena during COVID, explains Cox. “With the increased volatility in the past two years, our FP&A team has been focused on what’s coming through the opportunity funnel.”

Taking leading indicators and translating them into a revenue forecast have been critical, Cox adds. “It isn’t just measuring what’s coming out of the general ledger; it’s understanding in advance what’s going to impact the business and how that’s going to affect revenue—and not just on the quarter, but month over month. If you’ve got a lot of uncertainty like we do right now, you need to see as far into the future as you can and give yourself time to react.”

THE EVOLVING ROLE OF THE CFO

In 2022, companies will look for CFOs who can bring finance experts with them. “Followship is actually a criteria now, and it’s the first time I’ve seen that as a job requirement,” says Munro. “Companies want someone who has built a following among their finance teams and, when going to a new role, can bring them along and have an instant team.”

Since COVID-19 began, Munro notes, companies are placing more emphasis on a CFO’s ability to lead a business transformation, whether it be a divestiture or an expansion of the business, an acquisition, or a major contract. “Those skills are highly valued, and there are a lot of companies going through different types of transformation right now, and that’s something that has accelerated in the last two years,” she says.

At the same time, companies are looking for CFOs who can take their technology agenda to the next level in 2022. “Digital transformation is on steroids at the moment, and there’s really no end in sight,” says Munro. Consequently, companies are looking for CFOs who understand how to leverage technology to their best advantage. “For the finance function specifically, finance leaders are looking to eliminate repetitive tasks, and COVID has supercharged that agenda.”

CFOs are always striving to be impactful and strategic in the value they provide. “The way we do that is by being engaged in the business, thinking more holistically about the value we can provide with our particular skill set and the tools we have at hand,” Cox says. “A CFO who wants to be impactful transforms numbers into words and puts the story in the hands of the right people at the right time, even before they knew they needed it. Technology has been transformative in enabling us to do this effectively.”

As we roll into 2022, there are likely to be as many risks as there are opportunities as the world tries to adjust to and recover from COVID-19. Demand surges are likely to level off, easing the strain on supply chains by midyear. Yet talent shortages and skills mismatch aren’t expected to be resolved until the threat of COVID-19 is well over or when companies can retool with technology or training incentives can encourage labor to reenter the market.

For CFOs, managing through these challenges doesn’t imply a retooling of their skills, but rather refocusing their agendas, being proactive in predicting business impacts, and relying more on FP&A teams to ensure they have the analysis they need when they need it. Meanwhile, building leadership teams will be more important in 2022, as will the CFO’s role in business and digital transformation.

January 2022