Unlike airports in the United States, where different organizations typically provide the various services within the airport, the Group handles most operational activities within Dublin Airport, from security to disaster recovery to restaurants. This difference makes the organization an ideal candidate to study the concept of life cycle costing (LCC). LCC considers all costs related to keeping a fixed asset in production throughout the asset’s entire life cycle in order to optimize both the initial investment and the continuing costs of repairs and maintenance.

Management of the Group strategically assesses the investment in capital expenditures for acquisitions, along with ancillary costs and the costs associated with the repair and maintenance requirements of those assets while they’re in service. For this reason, determining accurate costs using an LCC approach is critical. In the airport’s case, this is necessary to safely and cost-effectively accommodate the growing number of passengers with the efficiency that passengers expect. The airport must manage risk since the failure of older assets can pose a danger to travelers, employees, and visitors. This process requires a “whole life” asset view, which involves the coordination of several critical areas, including, but not limited to, asset acquisition, operations, repairs, and maintenance.

The Group views asset management as a critical part of its business. As with many organizations, the airport’s systems didn’t meet the growing needs of capturing the voluminous data it needed for tracking the full life cycle costs of assets. At Dublin Airport, obtaining the whole life cost of an asset took 14 steps, crossed two primary computer systems, involved three people from different departments, and required more than a day to set up a single asset. The process was further complicated by crossing multiple functional areas, e.g., airfield operations, third-party repair technicians, and finance, which made gathering the information a conflicting priority between departments.

Even with this amount of effort, the data was often still incomplete or inconsistent. The ability to track the assets over their entire life span was essential for the Group, as the failure of an asset could mean severe passenger delays, expensive equipment damage, inadequate spare parts inventory, or worse (e.g., injuries). The wide variety of assets tracked by an airport—such as safety equipment, fire protection equipment, security detection assets, and kitchen equipment—increases the difficulty in tracking the equipment. In addition, the process would also need to track the traditional cost, payback, and return on investment considerations.

TRACKING PHYSICAL ASSETS

Two primary systems track physical assets at Dublin Airport: an Oracle enterprise resource planning (ERP) system and the computerized maintenance management system (CMMS). The Oracle system, primarily used by the finance department, contains all financial information for all assets owned by the airport. When an asset is acquired, the asset’s project manager completes an asset creation form, which is then used by an employee in the shared services center to enter the new asset into the Oracle system.

The Fixed Asset Register (FAR) module within the Oracle system contains the financial records for all of the nearly 10,000 assets. FAR is used to track depreciation, estimated life, disposal of assets, and other data required for financial reporting. While FAR is adequate for preparing the statements for accounting, a complete view of the assets isn’t possible.

For most of the asset project managers, the only step in the process they were responsible for was completion of the asset creation form. At times, project managers didn’t understand some of the fields on the form or how the information was used downstream. For example, when asked to select a category type for the equipment, project managers frequently selected “Miscellaneous Equipment” rather than selecting a more precise category. The inaccurate data on this form further hindered the ability to compile the complete life cycle costs.

In addition, repairs and maintenance are typically initiated and tracked by a different physical department, as is the case at most businesses. The maintenance and functional operations departments use the CMMS, which collects the data related to maintenance and other operational costs. Linking the assets between the two systems is time-consuming; thus, the information isn’t readily available.

A university and industry consulting team worked with the Group to review its current processes and to identify and recommend solutions to enhance the LCC process at Dublin Airport. One of the primary concerns was that the organization was unable to use the information in the Oracle FAR to optimize the maximum value it could achieve. While FAR meets international accounting standards, the lack of structure with the asset creation form made it impossible to determine the total life cycle cost.

In addition, linking assets between the Oracle system and the CMMS proved to be a challenge due to a lack of standard naming convention for the assets. The difficulty in getting this information prevented management from having a complete picture of the assets, which is useful in determining which assets were going to be obsolete soon or had maintenance costs that exceeded expectations. Without complete information, the Group wasn’t receiving the full value from the data it did have.

LIFE CYCLE COSTING

The airport’s situation isn’t unusual. Many companies struggle with capturing the total ownership costs of their fixed assets on an ongoing basis.

At the time of an asset’s purchase, finance typically focuses on capturing the acquisition costs of the assets required for accurate financial reporting—this includes not only the costs of the asset, but the costs to install and prepare the asset for usage. Yet often, these are the only costs considered. Maintenance costs for the asset, including the cost to operate the asset and all personnel costs related to the upkeep of the asset, aren’t considered.

During a purchasing decision, the organization may prepare some estimates of the full life cycle costs to compare projects. Once the asset is purchased, however, the tracking of other actual expenses, such as maintenance, falls by the wayside. Those in the finance department tend to focus primarily on what information is needed for financial reporting, e.g., asset costs and depreciation. They rarely track the other expense items by an individual asset once that asset has been installed. Since those costs aren’t required for financial reporting, they typically aren’t tracked in the financial systems. On the other hand, operations and maintenance departments are more concerned with the maintenance costs, with little focus on the financial statement implication.

Since each group or division has a different perspective of what information needs to be captured, a full picture of the asset’s costs isn’t available. Yet in many cases, the post-acquisition costs of an asset can exceed the initial costs of an asset, creating a significant financial obligation over the life of an asset (see Figure 1). Companies that have a better understanding of the full cost of an asset can make better decisions regarding maintenance plans, replacement of equipment, and ongoing support.

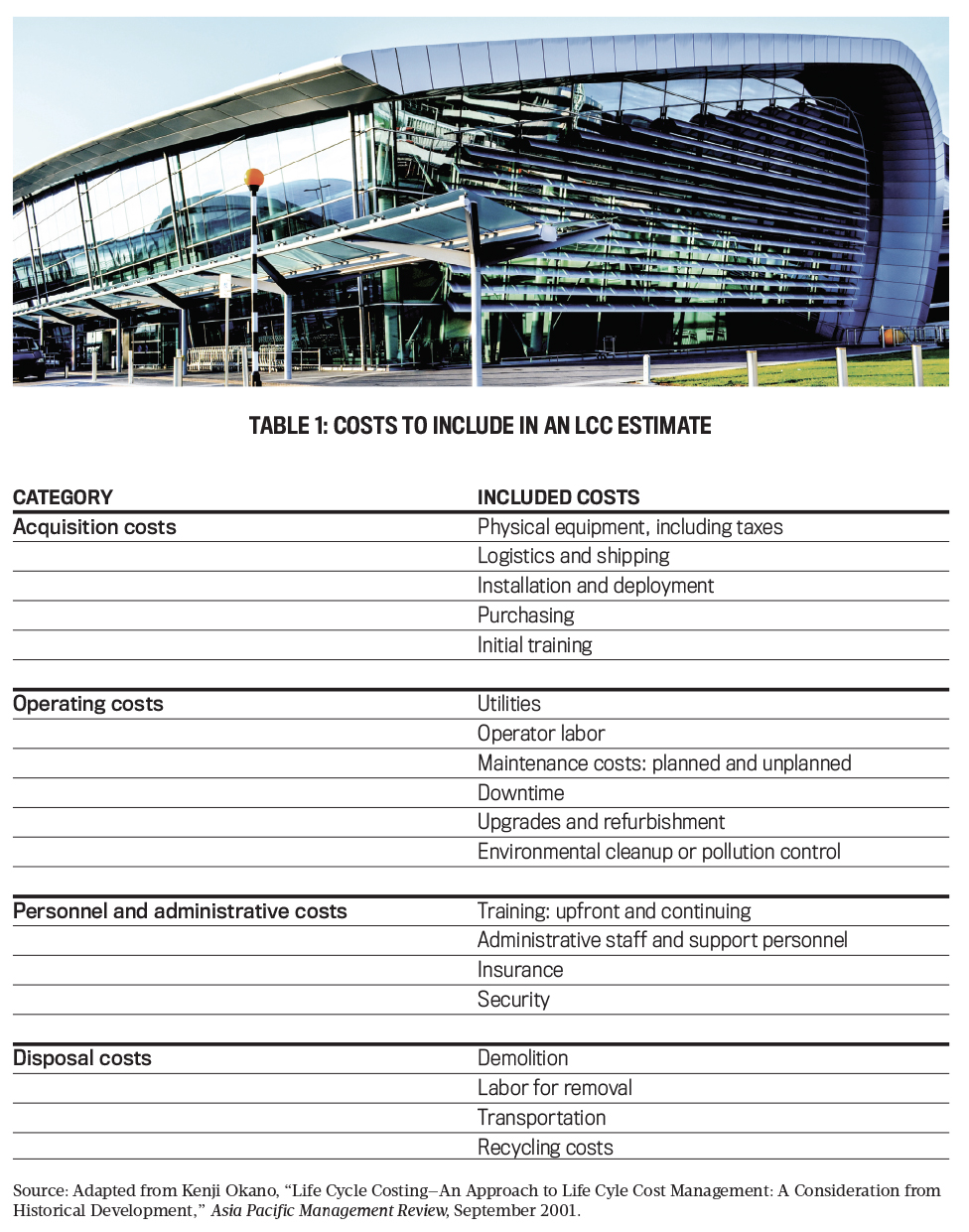

At the time of an asset acquisition, the estimated life cycle cost can be used to compare projects or competing brands of a particular asset. The types of costs to include are in Table 1. The expenses used in determining the total life cycle cost will vary among different asset types. What’s important is that the costs considered are relevant to the operation of the business and are developed fluidly based on the most recent information, in contrast to traditional costing methods that are developed to be in compliance with accounting principles or tax laws.

Click to enlarge.

Many companies find that tracking the actual information after the purchase is more complicated than preparing the initial acquisition estimate. Yet there’s much to gain for companies that choose to track the asset costs after its acquisition. Many assets have increased operational and maintenance costs as they near the end of their useful life. A trend of an asset’s costs over its life can be compared to a typical pattern for this asset. Using this type of analysis can lay a foundation for planning for capital budgeting. For example, if an asset is experiencing higher repair costs than expected based on comparisons to similar assets, it can signal a potential problem. Management can then adjust the replacement cycle, if needed, and the corresponding maintenance and capital budget. Tracking total life cycle costs can help an organization better manage its overall asset portfolio.

In the case of Dublin Airport, the Group manages a wide array of different types of assets, most of which are vital to the airport’s operation. An outage of a critical asset can shut down the airport, causing immense travel disruptions for passengers and losses for airlines. Thus, having an accurate picture of the performance of an asset can help manage assets and maximize uptime.

In addition to traditional quantitative assessments, organizations should also track and anticipate both risks and opportunities. This is known as risk mitigation and opportunity identification. From a risk perspective, each asset should be assessed periodically to ensure not only that direct individual asset costs are considered, but to determine the possibility that the asset could fail, causing damage to other assets or, even worse, injuries or deaths.

From an opportunity perspective, there are always new alternative assets being introduced, and they often operate at lower costs than the assets they would be replacing. Therefore, when LCC is combined with risk and opportunity considerations, the result is a fresh and dynamic asset view and a deeper understanding of the important role that fixed assets play within an organization. When handled properly, the result can provide justification for using existing staff—or even adding additional head count—to manage the asset portfolio by providing a positive return on investment of the increased labor costs.

One crucial component of tracking asset costs is identifying the trends in maintenance and operations. If costs are suddenly increasing more than expected, it may be time to evaluate the viability of the asset. Asset owners will need to determine if the asset needs replacement or requires significant maintenance overhaul. The visibility of an asset nearing the end of its useful life cycle helps to reduce the risk of failure at an inopportune time.

This information can also be part of a capital budgeting plan. For example, when the uptime of the assets is critical, as in the airport, having a plan for replacement is crucial. Having more accurate information about the potential maintenance costs can give foresight to potential failures. The capital budget can be updated accordingly, allowing management to make more timely decisions.

SIX SIGMA PROJECT

To help the Group evaluate the current state process and obtain more accurate actual life cycle costs of the assets, a university and industry consulting team consisting of four students, their instructors, and airport staff undertook a Six Sigma project at the Group. As the current systems and processes were seemingly at their limits or threshold, the project goal was to analyze the current systems and processes for asset management and make recommendations for more consistent tracking in the FAR module and better decision making. In turn, the data in the two systems could feed an LCC process, helping the Group achieve its goals to help make Dublin Airport a leader for airline travel in Europe.

The team evaluated both the Oracle ERP system and the CMMS. One of the team’s main observations was that the Group wasn’t able to fully utilize the FAR module. It didn’t capture consistent data for fields such as locations, categories, and asset lives. To correct this, the FAR configuration was changed to have users select from a list of choices rather than enter free-form text. This change helped to alleviate the lack of consistent structure in completing the asset creation form.

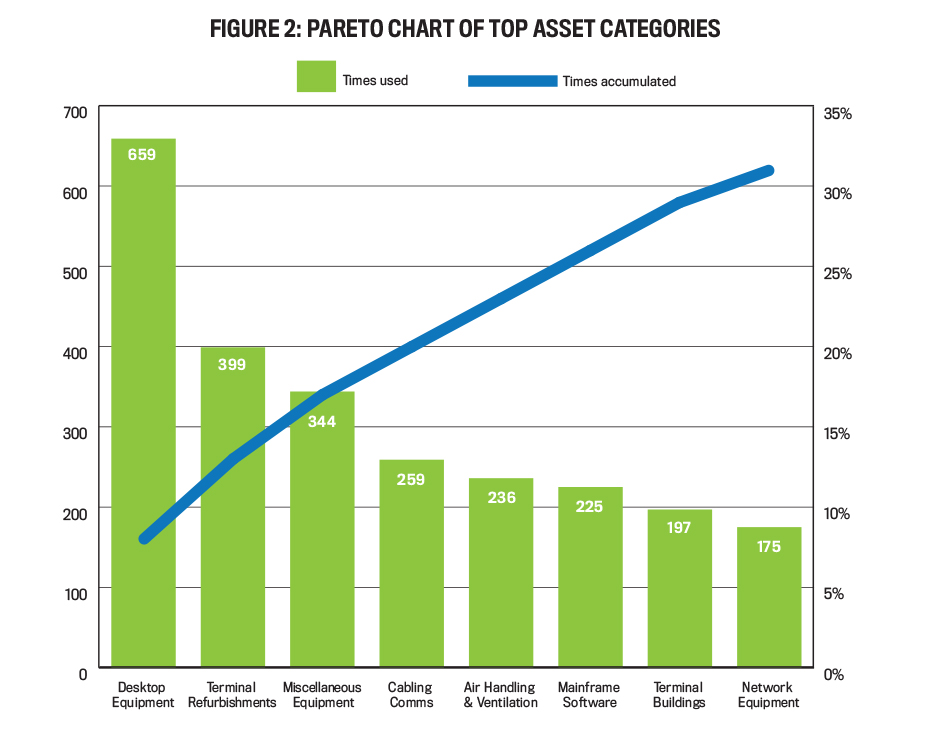

A statistical analysis of a sample of assets verified there was an issue with inconsistency in naming and categorization between the two systems. For example, in a sample of 100 assets, 24 of the assets had an incorrect category listed. Of the 191 existing categories, 16 were never used and 45 were used fewer than six times.

The large number of categories, sometimes with overlapping descriptions, added potential errors in the asset data. In addition, more than half of the sampled assets had a description inconsistency between the two systems. Figure 2 shows a Pareto chart with the eight most-used categories. As noted previously, the Miscellaneous Equipment category was frequently used as a catchall when the asset project manager was unsure of the proper category.

Click to enlarge.

The complicated nature of the process added to the data inconsistencies, partially hindered by the number of steps and individuals involved in FAR entry and maintenance. The team found that this process led to an increase in possible entry errors.

The team made several recommendations to simplify the entire process and provide greater accuracy. The recommendations focused on consistent naming of the assets between the two systems at the time of the acquisition as well as capturing all the costs in a single location. Even though this meant duplicating the asset acquisition costs between the two systems, it reduced the time required to retrieve actual cost information later. The asset number from the CMMS could then be cross-referenced in the Oracle system. The consistent asset number makes it easier to link the two systems and find the asset information. The new process, recommended by the team, would reduce the number of participants by one and cut the number of steps by one-third.

POST-PROJECT ACTIONS

Due to the common ground created through the use of LCC, an immediate synergy occurred. While there was a predictable stress between individuals and functions, LCC enabled all of the teams to see the common goal that expanded beyond the original fixed asset accounting and tracking of repair costs. The accountants and operations individuals are no longer working in silos and now can actively manage assets to provide risk mitigation, cost reduction, and opportunity identification.

As with many cross-functional projects that rely on multiple systems, the Group hasn’t been able to implement all of the recommendations due to resource constraints. Getting the available resources in different departments at the same time has been difficult. Yet the Group has been able to make strides in improving its process by aligning the descriptions of the assets between the two systems and gradually implementing recommendations as time and budget have allowed. This helps tie the assets together for gathering information.

Following the consulting team’s report, the Group sought a new enterprise asset management system and selected a new service provider (IBM Maximo) in 2018, which is now being implemented across Dublin Airport’s Asset Care. A vital part of the requirements was stock management and real-time integrations between Oracle and Maximo. This part of the project was the first to go live, leading to a change in process that includes:

- All spare parts are managed for asset care in Maximo.

- Issuing spare parts to work orders and minimum/maximum inventory management process occurs entirely in Maximo.

- Purchase requisition requests are sent through the Oracle system to follow the normal purchasing processes.

- Items are procured through Oracle Purchasing as per the Group’s existing company processes. They are then received on Oracle as “Non-Stock Items.” Receipt information is transferred to Maximo, where the items are automatically received as “Stock Items” to complete the cycle.

While the focus of this project was on the importance of consistency in fixed asset cost data and LCC in the context of aviation operations, the challenges and associated opportunities apply to all industry segments. And the recommendations are scalable from the smallest to the largest organizations.

As companies are facing stricter budget and financial pressures, they’ll be forced to justify expenditures for capital assets. LCC provides better data to help management make a data-informed decision regarding the organization’s asset portfolio. Managers can better predict the length of an asset’s useful life, providing better forecasting of future replacement needs or major service expenditures.

This project has become even more relevant with COVID-19 and the economic crisis. Accounting firms are diving deep into possible impairment of asset issues as there’s a need to justify the continued relevance and positive contribution of fixed assets. LCC couldn’t be more timely—proper application will not only optimize costs and mitigate risk but will also assist with justification as to its overall value for continuing operations.

May 2021