The current health crisis has added urgency to the need for adopting new technology. As Michael Heric, Kurt Grichel, and Sabine Atieh wrote, “COVID-19 will demand not only that finance teams devote more time to value-added activities, but also that traditional activities, such as receivables and payables, run more efficiently and effectively, through remote collaboration and other new ways of working” (see “Is Your Finance Organization Ready to Navigate the Coronavirus?”). This increase in remote working combined with the already ongoing technological evolution creates a perfect storm for new technology being needed—and needed right now.

Yet a recent joint study by Deloitte and IMA® (Institute of Management Accountants) found that many companies are “having difficulty implementing even basic technology projects in finance” (From Mirage to Reality: Bringing Finance into Focus in a Digital World). Similarly reflecting the challenge in implementing new technology, a recent Gartner report noted, “On the one hand, finance leaders must recognize the potential for effective finance transformation using advanced analytics, ML [machine learning] and artificial intelligence (AI). But on the other hand, it’s important to keep in mind a sober truth: The path to ML and AI nirvana is littered with the corpses of failed implementations” (Rob van der Meulen, “Financial Forecasters Should Beware 3 Machine Learning Myths,”).

Organizations are unsure how to prepare for this technological challenge and where to start. There’s no shortage of material available to describe the capabilities of these new technologies, but there are few available resources on where organizations, particularly small and medium-sized ones, should start their “digital transformation,” especially with regard to the finance function. We focus on that issue here.

When thinking about where and how to deploy new technology, we recommend organizations go through a series of steps. First, think about where the need is greatest or will have the largest impact with the least effort. Next, determine the technology to be applied. Finally, have an effective change management process in place. Let’s explore each of these in more detail.

START WITHIN FINANCE

Opportunities to deploy new technologies exist both within the finance function and elsewhere throughout the organization in the processes for which finance is a cross-functional partner. While both of these can be fruitful venues for deployment of new technology, it’s often better to start within the finance function for a variety of reasons.

First, many finance areas today are experiencing severe resource shortages. They’re increasingly being asked to do more—like assuming a role in enterprise risk management and strategic planning, for example—with the same or fewer resources. IMA research has consistently shown that CFOs and controllers desire to assume a higher-value-added role in their organizations but are prevented from doing so due to the need to commit resources to overseeing more traditional responsibilities such as financial reporting and internal control. (See, for example, The Evolving Role of the Controller.) Using technology to reduce the resources needed for such tasks can free up finance to assume additional responsibilities, including serving as a strategic business partner to the rest of the organization.

Second, deploying new technology within the finance function reduces the need to get buy-in for an initiative from others outside the area. This enables finance to focus on initiatives that it believes are most important.

Third, automating finance first provides a low-risk opportunity to get the implementation of new technology “right” before rolling it out to other areas. Successful rollout of technology projects within the finance function provides “proof points” that can serve to demonstrate the potential for subsequent rollouts in other parts of the organization. As a joint Association of Chartered Certified Accountants (ACCA) and IMA study noted, “The finance organization needs to demonstrate consistently the value it is bringing to the enterprise. It needs to get better at showcasing the proof points, because this secures sustainable commitment and helps finance be seen as fully integrated into the business” (Financial Insight: Challenges and Opportunities).

Finally, by deploying new technology, finance can gain credibility as a technology leader within the organization, becoming an area that others can look to when developing their own technological solutions. Emma Hitzke, senior product marketing director of Emerging Technologies at Oracle, notes the common impression that “Finance likes to influence and say they push for change in other departments, but finance doesn’t like to change themselves. They’re very conservative.” Leading technological change is a good way for finance to counteract this impression.

WHERE TO START?

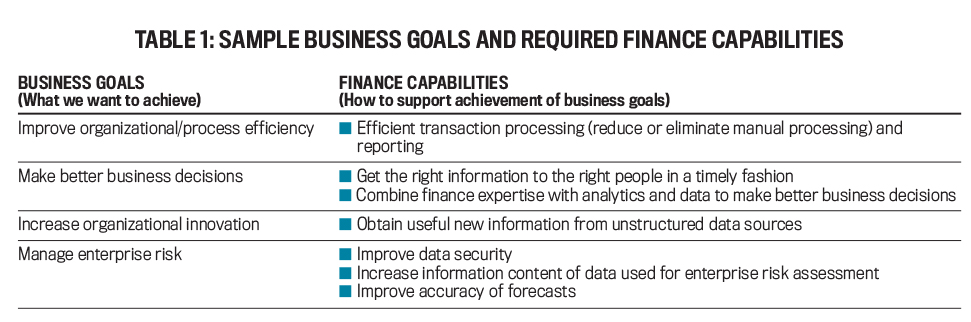

With so many technologies emerging and evolving rapidly, choosing where to begin can be a challenge. An important initial step should be developing a strategy to effectively use the leading-edge technology and analytics techniques required to become a data-driven organization. Development of this strategy starts with considering finance’s business goals. These might include minimizing compliance spending and risk, increased speed of innovation, or reduced administrative complexity. As Gartner notes in its Finance Technology 2020 report, delineation of these goals will help an organization ascertain the capabilities finance needs to develop, i.e., “how we will support the business”. Table 1 presents examples of potential goals of finance areas and the capabilities needed to meet those goals.

Click to enlarge.

Click to enlarge.

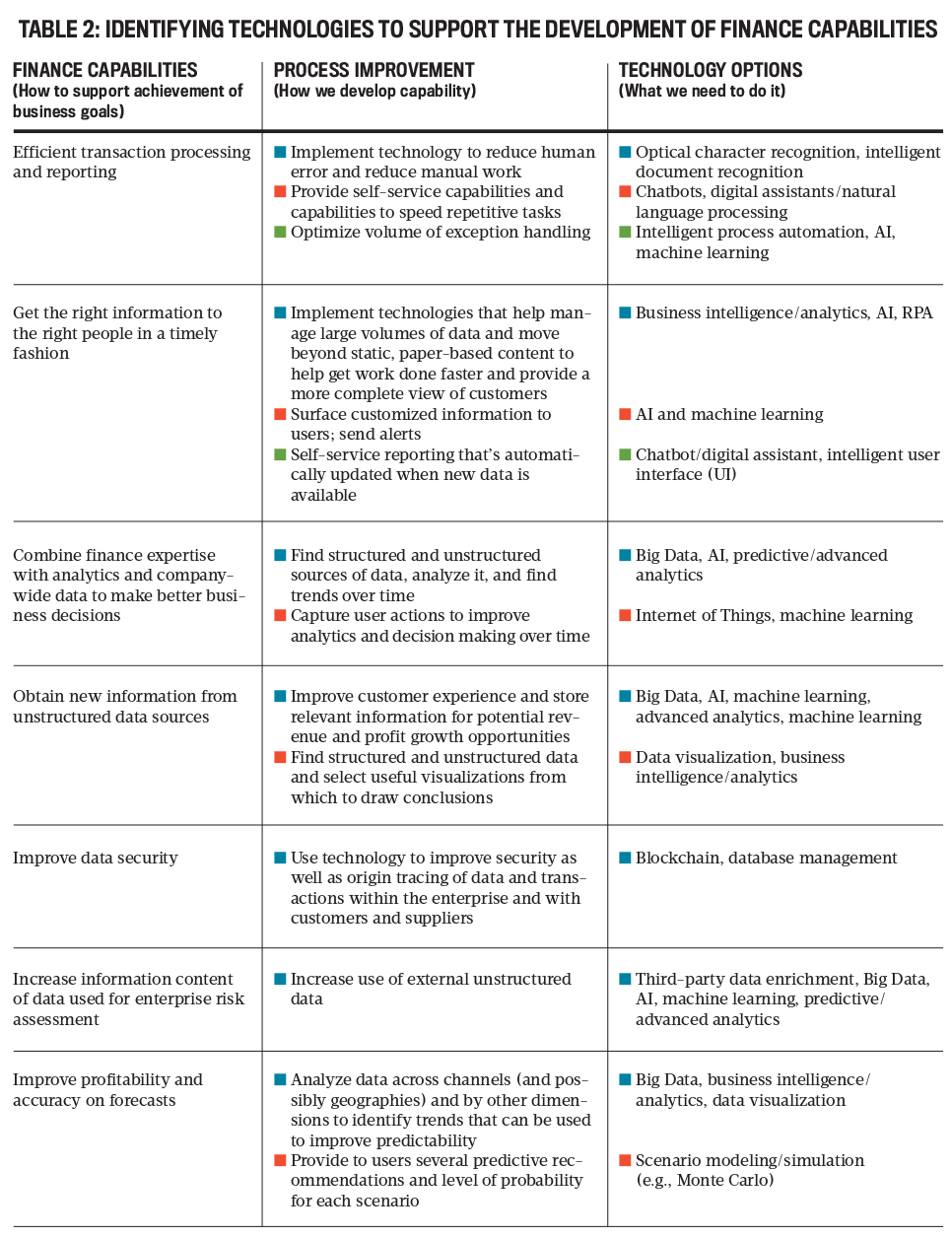

Delineating the business goals and the capabilities finance needs to develop to meet those goals will, in turn, help identify necessary process improvements and the technologies that can be used to achieve the desired capabilities. Table 2 contains some examples of these.

Click to enlarge.

Click to enlarge.

SELECTING THE TECHNOLOGY

Once finance has identified it goals and possible technological solutions, the next step is to identify a specific problem to solve using advanced and emerging technologies. One place to start is by identifying critical business questions and determining how data can be used to answer these questions. As Ray Wang noted, this will entail identifying the appropriate data sources, building data proficiency, and connecting the right data with the appropriate people (see “How to Lead a Data-Driven Digital Transformation,” Harvard Business Review webinar).

In addition to knowing the business goals and needed capabilities, finance functions just beginning their digital transformation need to consider other factors as well. These include whether the implementation of a particular technology can be done at a smaller scale initially, the required competencies of the finance staff to implement and use the technology, the amount of capital expenditure required, and the length of time required for implementation. The potential solution should be evaluated on all these dimensions. Finance can then map out short-, medium-, and long-term technology objectives.

When considering the implementation of new technologies, it’s important to remember that those that generate significant immediate efficiency gains can yield substantial returns. The key is to find repetitive, time-consuming tasks that must be performed consistently yet quickly. These are often tasks that involve multiple steps and/or a large amount of data. They should be evaluated for their ability to be automated as well as the period required for payback of the associated technological investment and for the impact on staffing requirements.

An additional consideration is that technologies such as robotic process automation (RPA), analytics, and AI are enabling virtual finance platforms that can be built on top of core systems rather than having to replace them. This enables improvement in the finance function without moving or changing the core essential systems that typically have a large associated cost. RPA is a good example of such a technology because it integrates well with legacy technologies and processes, can often be implemented in less than a month, and can generate positive returns within three months for simple processes.

As AFP Mindshift notes in Emerging Technologies and the Finance Function, activities that can be automated through RPA range from relatively simple—like using screen-scraping technologies to take data from websites or legacy applications, manipulate the data, and enter it into another system for use in other processes—to more complex activities, such as combining robots with more unstructured data and algorithms to manage complex tasks and become more intelligent and independent over time.

Another consideration is that digital transformation for most organizations is a journey, not a destination. In a 2019 IMA study, only 8.5% of organizations reported that they have completed implementation of their desired leading-edge analytic techniques and technologies (The Data Analytics Implementation Journey in Business and Finance). And in Pivoting to Digital Maturity: Seven Capabilities Central to Digital Transformation, Deloitte notes, “Digital transformation is about more than implementing discrete technologies. Rather it requires developing a broad array of technology-related assets and business capabilities.”

As such, it’s helpful for organizations to focus initially on foundational technologies that develop an organization’s data infrastructure and the general technological maturity of its staff. This, in turn, facilitates the subsequent implementation of other technologies.

IMPLEMENTING THE TECHNOLOGY

Now that you’ve identified the technology (or more likely, technologies) that you want to implement, what’s next? It’s important to keep in mind that implementing new technology can have a significant impact. Organizations need to practice effective change management practices in these implementations. (For a thorough discussion of change management techniques, see the IMA Statement on Management Accounting, Managing Organizational Change in Operational Change Initiatives, by Katie Terrell.)

Getting the implementation “right” involves paying attention to several key items, including:

- Starting simple and small when first implementing projects.

- Expanding the sources of data used and exploring potential uses not only of data available internally but also of data available externally.

- Getting information based on data into the hands of those who need it on a real-time basis.

- Getting upper management on board (or in the case of cheap tech, start a bootstrap movement).

- Getting IT and finance organization buy-in.

- Forming a cross-functional team and communicating well.

- Adequately evaluating the technology and potential vendors.

- Building strong data governance and quality infrastructure in order to ensure data integrity and quality.

THE ROLE OF FINANCE AND ACCOUNTING PROFESSIONALS

For finance and accounting professionals, the prospect of implementing new technology may at first be intimidating. Yet, on one level, it’s about problem solving, which is what management accountants do—we find efficient ways to solve problems.

Being able to implement technology is a valuable skill. But knowing “what goes on under the covers is a more valuable skill, even when it is done for you,” says Daniel Smith, head of innovation and founder of TheoryLane Cloud Integration Solutions and a member of IMA’s Technology Solutions and Practices Committee. “Management accountants need to penetrate the hype and jargon and understand what is really going on. We need to understand how data moves, is transformed, and used.”

An example of this is blockchain. Accountants should be able to understand how to build a blockchain and how it works, but they shouldn’t have to be the one who actually builds it. We need to be able to construct a value proposition—understand the nature of the situation, perform a make vs. buy evaluation, and assess the options of building it in-house vs. outside (which depends on the value proposition).

Many organizations are slowly moving toward a data-driven approach to business. Business behavior creates data, and we’re starting to take greater advantage of that data. Right now, a human intermediary is needed to understand what the model is. That’s the role that management accountants can fill—someone who can see the data and understand its implications. Described as an “analytics translator,” this role requires combining accountants’ domain knowledge and quantitative and project management skills with other abilities.

As Gartner notes, “A creative, critical thinker with deep knowledge of the business and some basic coding skills can make an effective citizen data scientist. Some companies even find that analysts with non-IT backgrounds make better citizen data scientists than certified programmers because they are more open-minded and willing to reframe their thinking” (gtnr.it/2QAT3pX).

This is the way of the future. As management accountants, we need to look forward to the opportunities new technology can bring to our companies. Finance organizations that fail to adopt appropriate technology will risk becoming irrelevant as they fall behind the rest of the organization. Given all the benefits and efficiencies from these emerging and evolving technologies, can you afford to ignore them and risk becoming obsolete?

Emerging Technologies and Processes

AI: The replication of human intelligence by machines programmed to think as humans do. The term can also apply to machines that display traits normally associated with human cognition, such as learning, logic, and problem solving. GOFAI (good old-fashioned artificial intelligence) basically uses algorithms plus data, while neural AI uses digital networks to model the cooperation seen in the neural networks of the human brain.

Big Data: This can refer to one or both of the following:

- A large volume of structured, semi-structured, and unstructured data that’s difficult to analyze using traditional techniques (e.g., too slow or hits capacity limits). Unstructured data could include audio files, video files, email text, notes from call centers, etc.

- Software that’s used specifically to analyze large volumes of structured, semi-structured, and unstructured data to glean new insights (e.g., customer behavior, operational bottlenecks, possible new revenue sources, etc.)

Blockchain: Essentially, a digital ledger of transactions using a chain of computers that must all agree on and approve an exchange before that exchange can be verified and recorded. Cryptography keeps the exchanges secure in “blocks.”

Business intelligence/data analytics: A process for analyzing data and finding information to act upon using technology that will help executives, managers, and others in business make informed decisions.

Chatbot: An application that simulates human conversation online through text or text-to-speech. It’s often used for customer service and for providing or gathering information.

Cloud computing: The delivery of basic computer services over the internet rather than stored locally. This can include servers, storage, databases, networking, software analytics, and more.

Data visualization: The process of displaying data and/or information visually, like with maps or graphs, so that it makes more sense to the human brain. Typically, it highlights patterns, trends, and anomalies in the data. It’s usually a part of business intelligence.

Digital assistant: Voice-activated software that can understand and carry out electronic requests using voice recognition, natural language processing, and speech synthesis.

Edge computing: Using a distributed, decentralized architecture, edge computing involves data processing performed in the cloud but away from the large central networks to deliver localized analysis and decision making closer to the source data. A major advantage is reduced latency.

Intelligent process automation: A combination of robotic process automation (RPA) and AI that helps complete work more efficiently.

Machine learning: The process through which digital machines are able to learn from their own observations, from trial and error exercises, or even from natural language processing and generation. Machine learning can be either supervised by designers and programmers or unsupervised as when a machine learns on its own to play winning chess, Go, or even computer arcade games.

Natural language processing: A group of tools that enables machines to extract information from human speech or text and, in some cases, respond to requests based on that information.

Robotic process automation (RPA): Software that can be programmed to do basic, repetitive tasks across one or more applications. It can launch and operate other software and handle large amounts of data and multiple-step tasks in a particular order, saving employees a lot of time and reducing errors.

Virtual reality: Computer-generated simulation of a three-dimensional image or environment that provides means for physical interaction. Useful in demonstrations or for training.

The authors would like to acknowledge the assistance of Denis Desroches in the writing of this article.

October 2020