I recently talked with Baruch Lev, Philip Bardes Professor of Accounting and Finance at New York University Stern School of Business (above, right), about current issues in finance and accounting and how management accountants can play a part in helping their companies be the best they can be. In this article, he shares insights from his latest book, The End of Accounting and The Path Forward for Investors and Managers (Wiley, 2016). Based on extensive empirical analysis, Lev and his coauthor, Feng Gu, demonstrate how financial reports have largely lost their relevance and present actionable alternatives for CFOs and finance professionals.

Frigo: What motivated you to write your latest book?

Lev: I started noticing the diminishing usefulness of financial reports roughly 20 years ago when I became a partner in a consulting firm in charge of finance and corporate valuations for mergers and acquisitions. As an erstwhile accountant, I relied on financial reports in my valuations, but it quickly became clear to me that these reports were rather unreliable, particularly for tech, pharma, and internet and media enterprises, which were our main clients.

GAAP [Generally Accepted Accounting Principles] earnings didn’t reflect enterprise performance, nor were they guides for future growth, because of the immediate expensing of practically all long-term investments and the host of one-time items and fair-value adjustments. And they are not very useful for predicting cash flows. The balance sheet was, and still is, a hodgepodge of some assets valued at historical costs and others at current value, and most of the really important assets (patents, brands, etc.) are missing from the balance sheet. I gradually realized that this accounting irrelevance affects practically all sectors, not just high-tech.

My perception of financial information’s diminished usefulness was confirmed by many of my colleagues and by executives. For example, in a widely quoted CFO survey, the majority stated that financial reporting is today essentially a compliance exercise rather than an information-sharing activity (see Ilia Dichev, John Graham, Campbell Harvey, and Shivaram Rajgopal, “Earnings Quality: Evidence from the Field,” Journal of Accounting and Economics, 2013).

A CFO of a large company recently emailed me: “My investors don’t understand the accounting, nor do they care.” So I realized that I am encountering a serious, systemic problem worth writing a book about. The widespread, generally favorable reaction to the book confirmed my conviction that accounting and financial reporting needs to be fundamentally changed.

Frigo: What advice do you have for CFOs who want to adopt your ideas and make a difference in how they communicate to the investment community? What are the initial steps they should take?

Lev: Don’t wait for the FASB [Financial Accounting Standards Board] or the SEC [Securities & Exchange Commission] to adapt financial reporting to the 21st Century. It may take a while. Start disclosing relevant information to investors. It’s not only good for investors—it’s good for you, too. Research overwhelmingly shows that improved transparency reduces cost of capital and stock volatility, increases managers’ credibility, and mitigates shareholder lawsuits.

Many companies do this already—product pipeline disclosure by pharma and biotech companies, customer data by telecom, internet, and insurance firms—to overcome the deficiencies of the financial reports. But these non-GAAP disclosures are generally haphazard and inconsistent over time and hence of limited value to investors.

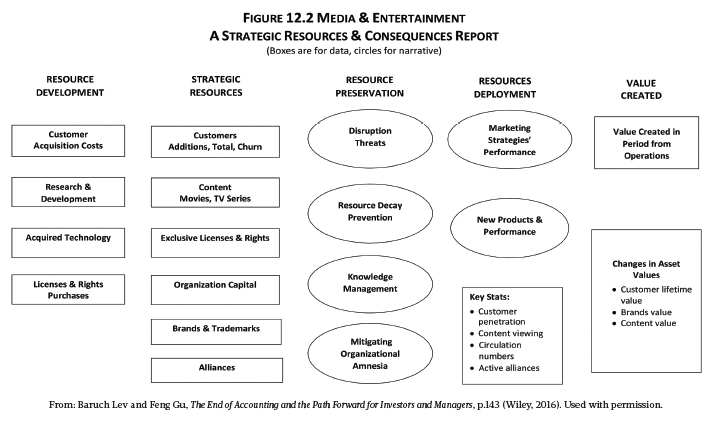

Frigo: In your book, you propose a “Strategic Resources & Consequences Report” that focuses on the items that create a sustained economic advantage. This report would present details on such things as patents, oil reserves, and information technology—all in a standardized form. What are the initial steps you would recommend for CFOs and finance organizations to develop such a report?

Lev: The research underlying The End of Accounting involved the detailed examination of the transcripts of hundreds of quarterly earnings calls to gauge the information sought by investors. Strikingly, most analysts’ questions concerned the strategy of the company and the strategic assets: those value-creating, unique, and hard-to-imitate corporate resources. We based our proposed Strategic Resources & Consequences Report on the information we learned from the earnings calls’ Q&As.

To construct the report, you may start with identifying your major strategic assets: patents, brands, customer franchise, unique business processes (like Amazon’s and Netflix’s customer recommendation algorithms). You proceed with identifying the investments in creating and maintaining the strategic assets (R&D, customer acquisition costs) and delineating the major threats to these assets from competitors’ infringement and technological disruption.

Then comes the articulation of the deployment of strategic assets (how many patents under development, licensed out, abandoned) and the computation of the value created by your strategic and other assets. Chapters 11-15 of The End of Accounting demonstrate this report on four major industries and detail our unique computation of the periodic value creation. See the figure for a sample report.

Frigo: How would you recommend companies address a key intangible asset: brand?

Lev: Regarding brands, first make sure you indeed have brands. Many people confuse brands with widely known names. Polaroid and Xerox are famous names but not much of brands. Real brands enable their owners to charge premium price over competitors. Bayer aspirin is a brand because people knowingly pay more for it than for generic aspirin. Tesla is obviously a brand, too.

Since brands require considerable investments to create and maintain them, the main issue is to compute the ROI [return on investment] of brands: relating the revenues from the premium price charged to customers to the brands’ maintenance costs to determine whether to invest more or less on brands. It can be done, but very few companies do it, and fewer report it.

Frigo: In a recent keynote at the American Accounting Association (AAA) annual meeting, your message focused on “Restoring the Relevance and Viability of Accounting and Financial Reporting.” What do you see for the future of accounting? Do you think things are changing, and what are the barriers? What do accounting professionals need to do to develop better, more effective disclosures?

Lev: There is lots of feverish activity by the FASB and the IASB [International Accounting Standards Board] generating a constant stream of ever-more-complex and expensive accounting standards. But as the evidence clearly shows, this activity does not arrest the continuous deterioration in financial reports’ usefulness to investors. In fact, a recent, award-winning study showed that all the standards issued by the FASB in its first quarter century of operations had no effect on investors’ wealth (see Urooj Khan, Bin Li, Shivaram Rajgopal, and Mohan Venkatachalam, “Do the FASB’s Standards Add Shareholder Value?” The Accounting Review, March 2018). Go figure.

As long as the FASB and the IASB avoid addressing real issues—improved accounting for intangibles, the constant increase in subjective managerial estimates and forecasts underlying financial information (mainly from fair value accounting), and the total obscurity and unreadability of financial reports—there will be no progress in financial reporting usefulness.

Nothing better demonstrates this sad state of affairs than a recent study by two finance scholars showing that, on average, an annual report of a U.S. public company is downloaded only 28.4 times from the SEC EDGAR system, the go-to place for financial reports (see Tim Loughran and Bill McDonald, “The Use of EDGAR Filings by Investors,” Journal of Behavioral Finance, 2018). And, as we all know, downloading doesn’t mean reading and analyzing carefully. I hate to end with this bleak statement, but practically no one reads financial reports anymore. Time for a serious change.

SOLVING THE PROBLEM

The first step in regaining relevance in financial reporting is for all of us to recognize a problem exists. Baruch Lev presents a compelling case for accounting professionals and accounting academics to consider his empirical analysis as well as his ideas for a new era of financial reporting. CFOs and management accountants have an opportunity to experiment and develop internal performance reports focused on the components of the Strategic Resources & Consequences Report that create sustained competitive advantage.

This would enable companies to align strategy with long-term sustainable value creation (see Mark L. Frigo with Dominic Barton, “Creating Greater Long-Term Sustainable Value,” Strategic Finance, October 2018). To do this, CFOs and management accountants can use the Strategic Resources & Consequences Report as a blueprint to better understand and communicate (internally and externally) how the company creates value and intends to achieve competitive advantage with its strategic resources. This would be a major evolutionary step forward to improve financial reporting in the future.

USING THE STRATEGIC RESOURCES & CONSEQUENCES REPORT

Here are four ways CFOs and the finance organization can use the Report to help understand and communicate how the company creates value with its strategic resources.

Develop an Internal Strategic Resources & Consequences Report: This can help the CFO and finance organization develop performance measurement systems and incentives that are more highly aligned with long-term sustainable value creation.

Develop a Strategic Finance Organization: Developing an internal Strategic Resources & Consequences Report can help instill strategic thinking skills and acumen in the finance organization.

Develop Board of Director Presentations: The Strategic Resources & Consequences Report can be a great way to communicate the strategy of the company to the board of directors.

Earnings Calls: The Strategic Resources & Consequences Report can be a way to frame earnings calls discussions.

January 2019