Issued by the Financial Accounting Standards Board (FASB) as Accounting Standards Codification® (ASC) 606 and by the International Accounting Standards Boards (IASB) as International Financial Reporting Standards (IFRS) 15, the new standards contain a number of significant changes that impact the ways companies account for revenue. The motivation for the changes is to remove inconsistencies and weaknesses in existing revenue requirements and provide a more robust framework for addressing revenue issues.

The new standards should improve the comparability of revenue recognition practices across reporting entities, industries, jurisdictions, and capital markets and provide better information to investors and external users of financial information by improving disclosure requirements.

In line with a principles-based approach, there’s also a reduction in the number of standards and requirements companies need to refer to when ensuring compliance with Generally Accepted Accounting Principles (GAAP). Under IFRS, companies have used a principles-based model and are accustomed to this accounting framework. Under prior codified standards, U.S. GAAP was more rules-based, so moving U.S. GAAP toward a principles-based model is a big shift. Judgment plays a much larger role in the application of the new standards.

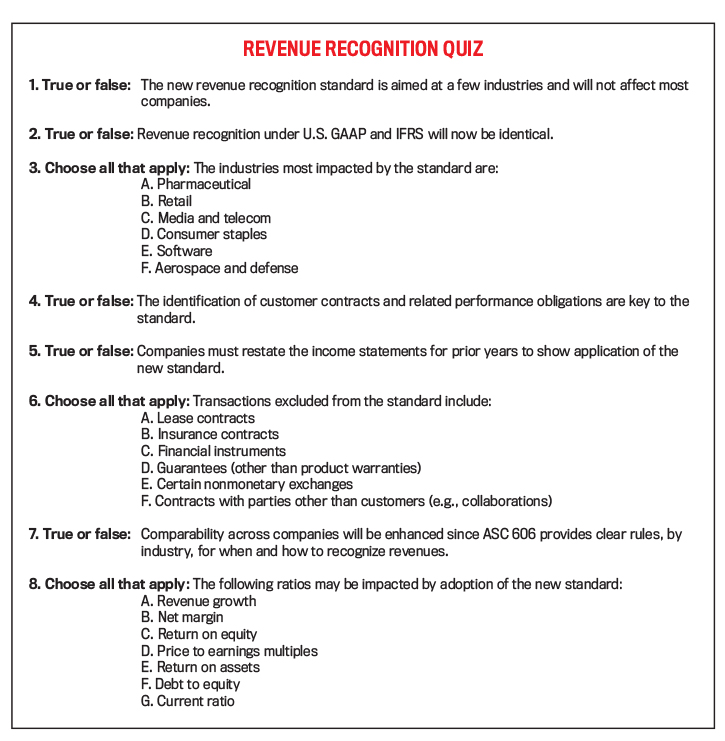

We created a short quiz to gauge your understanding of the key features and implications of these new standards (see “Revenue Recognition Quiz”). The quiz is essentially divided into three basic sections: those affected by the new standards, the key features, and implications for financial analysis. We’ll go over each section separately, providing the answers and examining the concepts in greater detail. By discussing each of these important questions, with an emphasis on the changes to U.S. GAAP, we hope to provide greater understanding and insight into the new rules and their potential impact.

INDUSTRIES AFFECTED MOST

The answers to questions 1 through 3 are:

1. False

2. False

3. A, C, E, F

We spoke with Eric Knachel, a partner at the Professional Practice Group of Deloitte, about the new rules. He said, “The standard will impact the recording of revenue in all industries. While some industries are impacted more significantly, every organization and user of financial statements must be aware and understand the implications of the new standard on financial statements.” He added, “All industries will be impacted since the disclosure requirements will be very significant and may be as much as three times higher than in the past. The additional disclosures will affect information technology systems, business processes, and internal controls.”

There are certain aspects of the new rules that will affect all companies. For example, under the new rules, certain costs to obtain and fulfill a contract are now recognized as assets. These costs include commissions, legal fees, marketing costs, and bid and proposal costs. To be considered an incremental cost, the cost must be related directly to the contract, generate or enhance resources of the entity, and be recoverable. In general, the asset would be amortized on a basis consistent with the transfer of goods and services the asset relates to. This may not always be straightforward if there are renewal periods in the contract. Amortizing these capitalized expenses may require a significant amount of judgment.

In addition, more extensive qualitative and quantitative disclosures are required. Companies are required to disclose and explain changes in contract asset and liability balances that occurred during the reporting period. They also are required to disclose out-of-period revenue adjustments, which is revenue that’s being recognized in the current period but resulted from past performance obligations, and they’re required to disclose performance obligations.

In terms of specific industries, Knachel noted, “There are a few industries which will be affected more significantly since the approach to revenue recognition will differ from the past. For example, software, media and entertainment, pharmaceutical/biotech, automotive, and the aerospace and defense industries will be greatly impacted due to their complex business arrangements and involvement of intellectual property.”

Construction companies and contractors will need to disclose both quantitative and qualitative information in their financial statements when the services are rendered or upon completion of service. Other industries likely to be impacted significantly are telecommunications, aerospace, construction, asset management, real estate, and software. Table 1 contains examples of the impact the new rules will have on specific industries.

Even retailers, distributors, and service providers may experience a material impact on financial statements. For example, retailers will need to decide whether to record revenues on a gross or a net basis. This will depend on whether the company acts as principal or agent. For example, it’s common in retail and distribution to have a drop shipment. If a shipment is sent directly to the consumer from the manufacturer, it becomes necessary to determine legal issues such as who has title or who handles returns. Depending on the answer, retailers may need to record at gross revenue at certain times and at net revenue other times.

Another example is the recording of revenue for financial institutions. For banks, earning interest income is generally out of the scope of the standard. If, however, a bank offers other services like financial planning, retirement services, or consulting services, it then must carefully consider what is in and out of the scope of the standard and clearly identify the impact to its business.

KEY FEATURES AND IMPLEMENTATION

The answers to questions 4 through 6 are:

4. True

5. False

6. All (A-F) would be excluded

What are the key changes to how revenue is recognized? Previously, U.S. GAAP had detailed and disparate revenue recognition requirements for specific transactions and for specific industries. For example, software and real estate industries had industry-specific revenue recognition guidance. The new rules replace these complex guidelines with a set of broad objectives to report to users of financial statements useful information about the nature, amount, timing, and uncertainty of revenue from contracts with customers.

At the core of the new standards is the contract between a vendor and a customer for the provision of goods and services. The new guidance attempts to simplify the decision of when and how much revenue to recognize. The entity is now required to identify goods or services provided to a customer and determine whether they represent a performance obligation. It’s only when the performance obligation is satisfied that revenue may be recognized.

These rules apply to all contracts with customers to transfer goods, services, or nonfinancial assets. They’re applicable to all entities and industries, with only certain transactions excluded. Transactions excluded from the new standards are lease contracts, insurance contracts, financial instruments, guarantees (other than product warranties), and certain nonmonetary exchanges and contracts with parties other than customers (e.g., collaborations).

Adoption of the standards allows two distinct implementation approaches: the full retrospective application or the modified retrospective application. For U.S. GAAP, companies using the full retrospective option must report the cumulative effect of the change in accordance with ACS 250, Accounting Changes and Error Corrections. This requires all prior years to be restated and the cumulative impact of the change reported in the earliest year reported.

Under the modified retrospective approach, an adjustment was made to opening retained earnings in 2018. Prior years are reported under the old standards in effect before adoption of the new standards. The modified approach also requires companies to include an explanation of the significant changes between the reported results under the new standard and those that would have been reported under existing GAAP in the first year of adoption. According to Knachel, 85%-90% of companies selected the modified retrospective application approach.

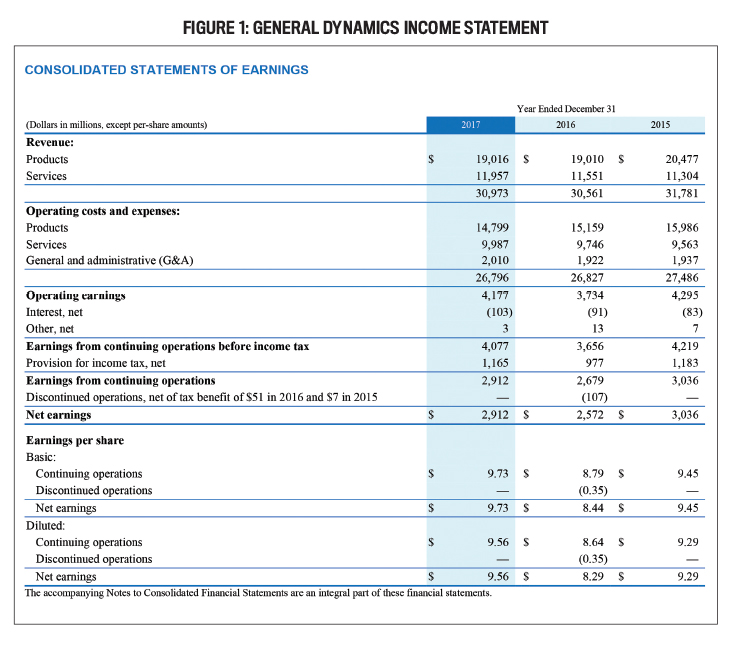

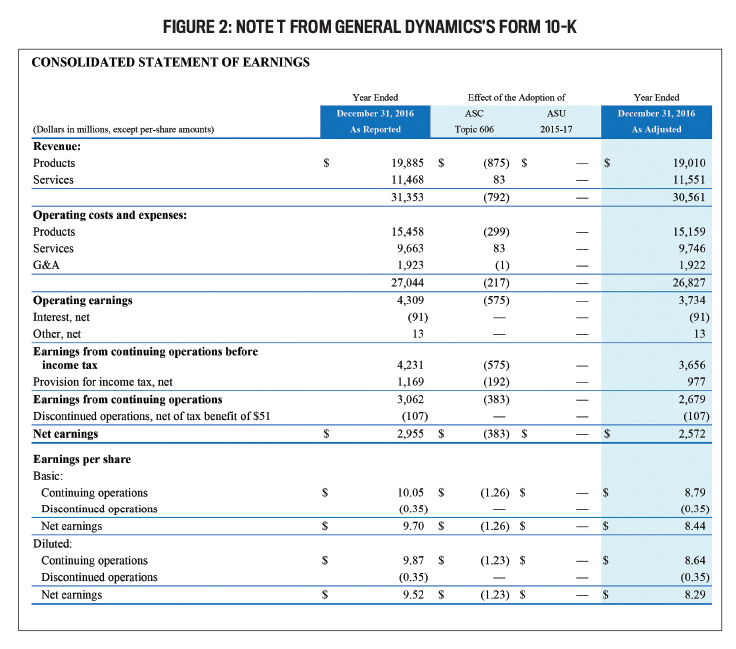

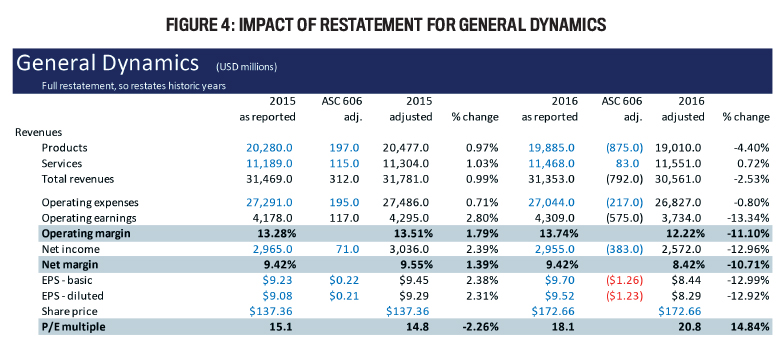

Let’s look at an example of a company that adopted the standard early to show how a company may report using the full retrospective approach. Figure 1 shows the income statement from 2017 Form 10-K of General Dynamics. Following the income statement is the note providing information on the restatement of prior years. Figure 2 shows Note T of the company’s 10-K, which details how the prior period financial statements were restated. Providing detail on how the change impacts prior years enables financial statement users to better analyze changes in revenue and profitability.

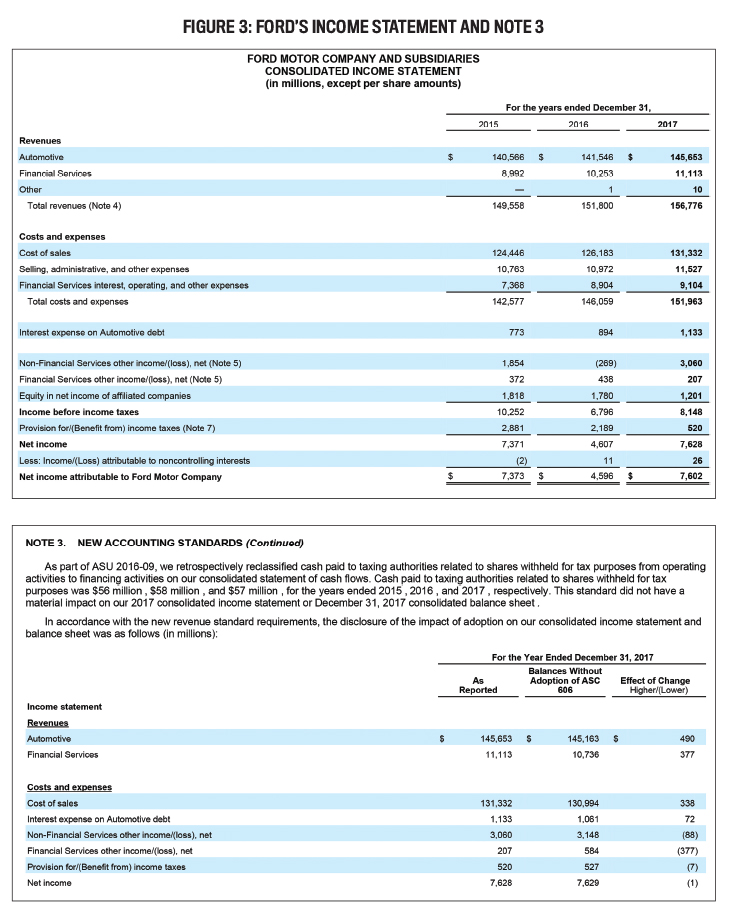

Compare this to the modified approach. Ford also chose to adopt the standard early but used the modified retrospective approach. Figure 3 shows Ford’s income statement and Note 3 from its 2017 10-K. The income statement doesn’t include any mention of the revenue recognition standard, but Note 3 contains information showing the impact on 2017 revenues. A user who knows enough to read the notes can thus identify the increase in revenues due to the accounting change.

FINANCIAL ANALYSIS AND FORECASTING

The answers to questions 7 and 8 are:

7. False

8. All the ratios listed could be impacted

Historically, revenue recognition has been the most significant area of accounting fraud. While the objective of the new rules is to simplify the decision of when to recognize revenue, comparability across companies and industries may not be easier. Financial analysts and users of financial statements may struggle to determine trends because the change in revenues is now due in part to changes in accounting rather than changes in volume or price.

Financial statement users will need to focus on disclosures, and companies may feel pressured to provide meaningful prior-year comparisons and disclosures that explain the accounting treatment of key business transactions. The move to a more principles-based application for U.S. companies will require users to read and understand the judgments disclosed in the financial statement footnotes. The accounting profession will still need to address the question of when it’s okay to have different accounting results due to judgment vs. when accounting should be the same across companies.

Another important takeaway is that adoption of the new rules may impact revenue, equity, and expenses. This means many key ratios will be impacted. As revenues change, users of financial statements may struggle to determine the level of “real” growth. For example, restatement had significant impact on revenues for General Dynamics, which therefore affected revenue growth, profits, profit margins, earnings per share, and the price-to-earnings (P/E) multiple (see Figure 4). These are among the most important ratios for analysts, investors, and creditors.

What will this mean for a company’s future revenue projections? If margins are improving or deteriorating, is it “real” or a result of the new standard? Answers to such questions won’t be straightforward, especially for companies that used the modified approach to adoption—though useful information should be included in the disclosures.

PREPARE FOR CHANGES

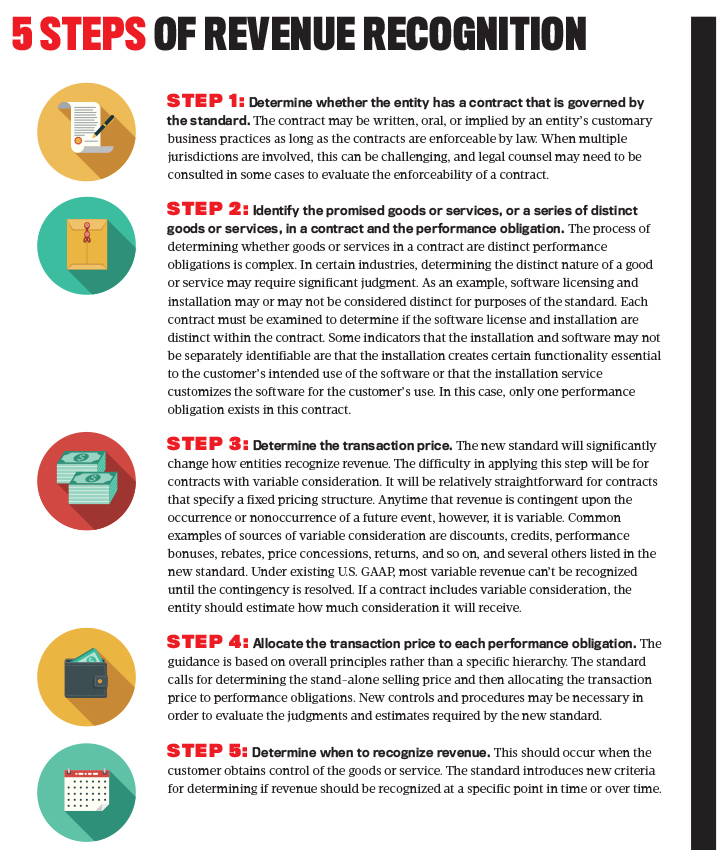

The FASB and the IASB provided an outline of five key steps to implementing the new revenue recognition standards (see “5 Steps of Revenue Recognition”). The new five-step model requires more estimates and judgments. Management must ensure that adequate internal controls exist and business processes have been updated to avoid errors in reporting and potential fraud.

The end result of these new rules and changes is that companies will be reporting 2018 results under a new standard that provides consistent guidelines for revenue recognition around the world regardless of industry and geography. Yet revenue recognition is more than just accounting. For those working within companies, ensuring proper implementation may require new IT systems, processes, and controls.

And for analysts and users of financial statements, it will be important that they scrutinize disclosures and the impact of the new standards to ensure they understand the implications of the new rules, are aware of which industries will experience a more material financial impact, and are able to discern “real” changes in revenues, profit margins, and return measures.

December 2018