Despite the pervasiveness of performance evaluations, however, they aren’t always met with enthusiasm by those being placed under the microscope. In fact, for many years, organizations have recognized that their performance evaluation systems don’t always accomplish their intended purposes. Several articles published last summer and fall noted that Accenture and a number of other very large organizations are eliminating their annual performance evaluation systems or are revamping them substantially. The articles note that the costs of the typical kind of performance appraisal system greatly outweigh the benefits.

We conducted a survey of accounting practitioners from the realms of industry, public accounting, government, and education. Our conclusion? A significant portion of this group isn’t satisfied with the way their evaluations are currently conducted, nor do they believe that they accurately reflect their contributions to the organization. The survey also revealed different perspectives depending on whether someone responded as an evaluator or an evaluatee.

A strong majority of performance reviewers, for instance, believe that their evaluations are effective in identifying their subordinates’ contributions and in motivating these employees to do a better job. As recipients of evaluations, however, they were less likely to feel the same way. The results also indicate that initial impressions, including those gained in conversations with colleagues, may affect evaluations of current performance, consistent with a growing body of research suggesting that initial impressions are persistent and difficult to overcome. Even many of the reviewers we surveyed were willing to admit that preexisting impressions may affect their current perceptions.

WHAT THE SURVEY REVEALED

After attending a continuing education seminar on an unrelated topic, participants completed a hard-copy survey designed to obtain their perceptions of their current performance evaluation systems. Approximately 57% of those in attendance (85 participants) completed the survey. Of this group, 80% said they currently work in some management capacity, with 70% classifying their position as “middle management,” “upper management,” or “owner/partner.” The average age of the 49 male participants and 36 female participants was about 46 years old. Respondents reported being with their current organization for roughly 13 years.

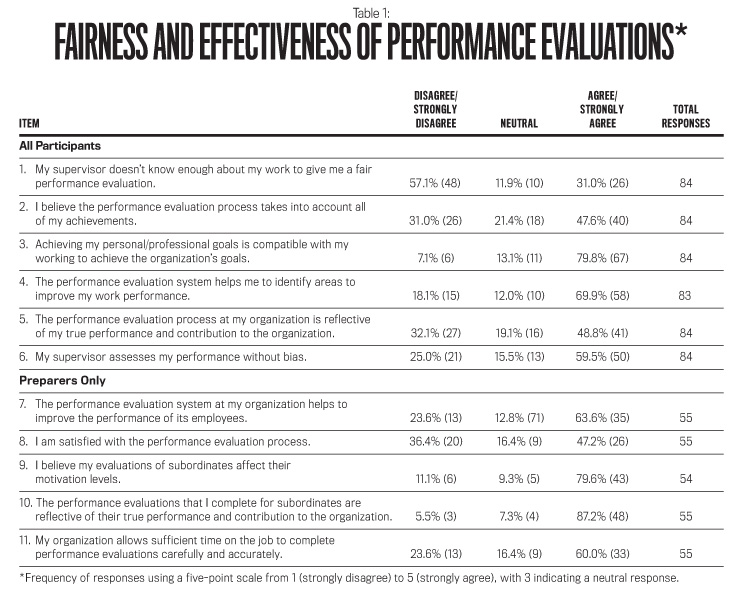

We asked participants to indicate their level of agreement with a number of statements regarding the general fairness and effectiveness of their organization’s evaluations. They responded on a five-point scale from 1 (strongly disagree) to 5 (strongly agree), with 3 indicating a neutral response.

As shown in Table 1, the accounting practitioners overall weren’t impressed with the systems of performance evaluation in place at their organizations. On a positive note, nearly 80% of respondents believe that meeting their own personal and professional goals is compatible with their efforts to achieve the organization’s goals. Further, nearly 70% believe that their system identifies areas where individual improvement is needed.

But the weight of the responses suggests that participants are rather unimpressed with regard to what the evaluations convey about them. More than 30% indicate that their supervisor doesn’t really know enough about their work to give them a fair evaluation and that their performance evaluations don’t reflect all of their achievements nor their true performance and contributions. When the “neutral” responses are added in, the total exceeds 50% for item 5 in Table 1, indicating severe dissatisfaction with the adequacy of performance evaluations.

THE VIEW FROM THE PREPARER’S SIDE

Not surprisingly, the folks on the other side of the desk—the ones who prepare and administer performance reviews—had a different perspective from respondents overall. Of the 55 people who identified themselves as a supervisor, approximately 87% said that their evaluations reflect their subordinates’ true performance and contributions to the organization.

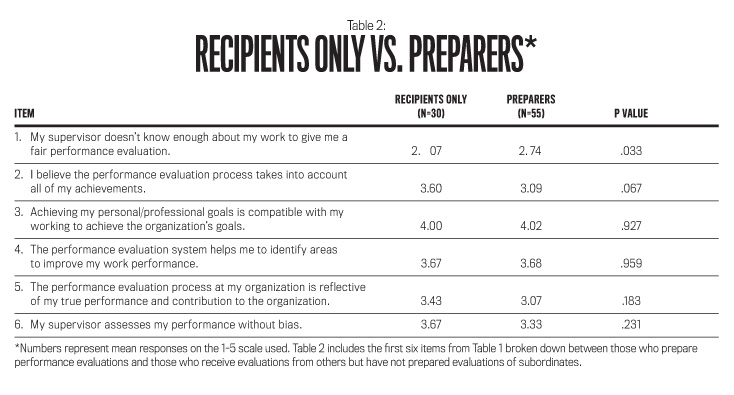

Since we asked essentially the same question of the reviewers and the reviewed (items 5 and 10 in Table 1), we analyzed these two items further and found that the preparers’ mean response (4.2 out of 5) was a full point higher than that of recipients (3.07 out of 5). Further, nearly 80% of performance review preparers believe that their evaluations effectively motivate subordinates. Finally, 60% of preparers believe that their organization allows them enough time to complete performance evaluations carefully and accurately, although 24% indicated that they might be rushed because of a lack of time. Another 16% didn’t tip their hand either way, saying they were “unsure.”

As shown in Table 2, there’s a significant difference between preparers and recipients for the first item and a “marginally significant” difference for the second item. What’s interesting is that preparers were less likely than recipients to agree that evaluations of their own performance take into account all of their achievements but seemed to agree somewhat more that their supervisor doesn’t know enough about their work to fairly critique it. That said, both groups’ tendency was to disagree somewhat with the statement in item 1, meaning that most of them apparently do think their supervisor has a pretty good handle on what it is they do on a daily basis. The difference for item 5 wasn’t significant, although preparers were somewhat less likely to indicate that evaluations received from others reflect their performance and organizational contributions.

HOW PERVASIVE IS EVALUATION BIAS?

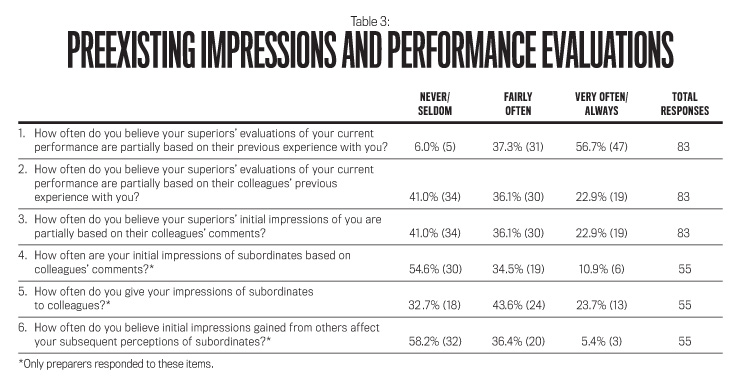

It’s important to note that one in four (25%) survey participants disagree that their supervisor’s evaluations of them are unbiased. To figure out how pervasive bias may be, we analyzed whether perceived biases in particular may account for some of the ambivalence in the previous responses. The vast majority of participants (94%) indicated that their supervisor’s evaluation of their current performance is based partially on their previous experience with one another. (As Table 3 shows, 37.3% said “fairly often,” and 56.7% said “very often/always.”) To a lesser extent, but still far from trivial, 59% believe that their supervisor’s initial impressions and their subsequent evaluations of current performance are based on colleagues’ comments at least “fairly often” (36.1%) or “very often/always” (22.9%). (Statistical tests indicated that gender had no effect on these responses.)

Among evaluators, however, 45% confessed that their own initial impressions of subordinates are based on colleagues’ comments at least “fairly often,” while 67% indicated they often share their impressions about subordinates with others. Nearly 42% of reviewers admitted that initial impressions gained from others often affect their evaluations.

SORTING THROUGH THE IMPLICATIONS

Our survey results suggest that in many cases accounting practitioners aren’t sold on their organizations’ systems for evaluating performance. Clearly, many don’t believe that the evaluations they receive adequately reflect their accomplishments and contributions or that their supervisor knows enough about their duties to evaluate them fairly. While we can’t say unequivocally that such reviews are biased, we can say that many employees believe that they are. In a best-case scenario, therefore, employees’ trust in their supervisors will be limited somewhat. In a worst-case scenario, biased evaluations can result in undesired turnover and even lawsuits.

Those who prepare evaluations of others (you may be one of them) may be more likely than they realize to allow preexisting impressions—whether based on personal experience or that of colleagues—to affect how they currently view their subordinates’ job performance. Depending on a person’s general management style and how hectic the pace of business is, managers may also unintentionally focus on “areas of improvement” and less on positive contributions.

It’s important to note that these evaluations only become “biased” when a different evaluation would have resulted had valid alternative information been considered. Nevertheless, our results show that an overwhelming majority of accounting professionals, when responding as an evaluator, believe that their evaluations reflect true performance and contributions. This finding is consistent with research suggesting that humans consider far less than the total available information because they may be unable to cognitively process everything they encounter about a person and are often overconfident in their assessments of others.

CAN THE SYSTEM BE FIXED?

If you want to take a more general look at your own organization’s system and are perhaps willing to be introspective about your own evaluations of others, here are a few suggestions:

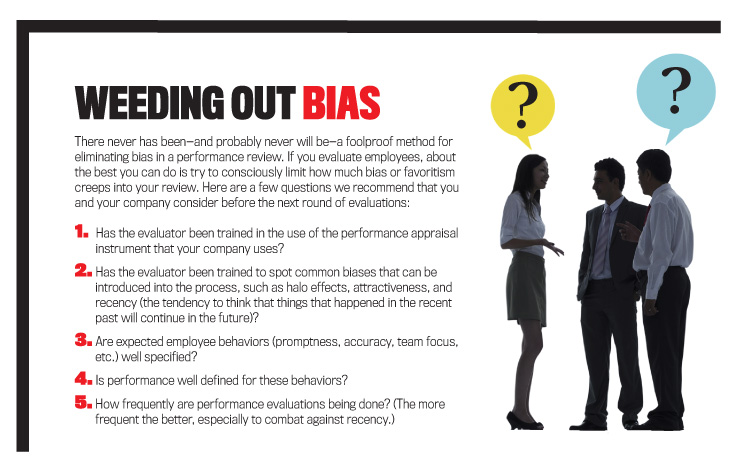

Ensure that managers at all levels are adequately trained in performance evaluation. Proper training for evaluators is imperative, yet research suggests that most companies don’t provide enough training in the problems of and techniques in performance evaluation. Further, individualized or small group sessions, combined with extensive practice and feedback sessions for improving rating accuracy, appear to be most effective.

Be aware that your own judgments may be biased. This bias may not necessarily rise to the degree of that often alleged in lawsuits and seems at least equally as likely to be unintentional as intentional. A considerable body of research suggests that an “anchoring and adjustment” process often takes place in which we begin with some initial “anchor” and fail to adjust sufficiently. That anchor may be an overall impression of an individual based either on previous experience with the person or on what someone else has said about them. If this process occurs subconsciously in evaluating others, the evaluator may (perhaps unknowingly) place excessive weight on the initial impression, thereby biasing his or her evaluation up or down. Further, some research shows that a poor initial impression is particularly powerful in that it may bias the evaluator’s recall of information about a subordinate toward things that are unfavorable. Even if you don’t think you’re biased, your subordinates may have a different perception. They just aren’t going to tell you about it.

Let your subordinates know that you genuinely want to recognize their contributions. For any number of reasons, your path to management may not have required you to work in the same capacity as your subordinates. If this is the case, recognize that your evaluations may reflect a limited understanding of what they actually do on a daily basis. In an age where a “facilitative” management style is often preferred over a “supervisory” one, listen to your subordinates’ ideas and consider them. They won’t all make sense, but some will.

Consider whether it’s time to rethink your system of evaluation. Research suggests that the details matter, such as the scales used. These scales may not capture a rating adequately, even if the related item is relevant and appropriate. Alternatively, the performance dimensions used may need to be updated to reflect your organization’s current strategy and what it expects from employees. In addition, consider allowing employees to critique the process and provide input as to whether the system is measuring what the organization claims that it measures. Usually it does, but sometimes it doesn’t (or doesn’t measure it as well as it could).

We’ve only just scratched the surface of the science of performance evaluations and their proper role in the private and public sectors. Whole books can be, and have been, written about this subject. One of our favorites is Performance Management by Herman Aguinis. No doubt, though, our survey has gotten you to think more about how people on both sides of the performance review fence view the process. If nothing else, we hope we’ve inspired you to have a deeper discussion of this process with the very people responsible for implementing and overseeing it. Done right—respectfully and thoughtfully—it will surely prove to be a win-win for everyone involved.

March 2016