What about China, you ask? While the slowdown continues, the Asian powerhouse will still chug away at a projected growth rate of 6.3% in 2016. The rest of the world, however, remains concerned about what slower growth in China will mean for them. In North America, this will be good news for some (such as U.S. steel importers enjoying lower input prices) and bad news for others (such Canadian commodities exporters).

SLOWER GROWTH IN CHINA HAS ITS BENEFITS

Against this backdrop, companies are reexamining their international expansion plans, keeping an ever-closer eye on the political risks of operating overseas. Cybersecurity is also top of mind, and CFOs continue to invest in systems and processes to ensure the safety of customer and employee information. At the same time, concerns around the recent U.S. interest rate increases and the impact on their companies’ bottom lines are prompting CFOs to step up their hedging strategies while sharpening their pencils once again to maintain margins against potentially higher financing costs and interest rate impacts on the demand for goods and services.

Worthington Industries, for example, is a global, diversified, metals manufacturing company serving the international automotive, construction, and agriculture markets. In 2014, it was the one of the largest purchasers of steel in the U.S., second only to the automakers. As CFO Andy Rose explains, his company has benefited from slower growth in China—more specifically, a softer global market for steel. “With the commodity index declining, and with China having the capacity to produce more excess steel than the U.S. consumes in a year, there’s been a flood of low-cost steel into the U.S.,” he says.

“Ultimately, for us that’s a good thing,” he continues, “because in our steel business we generate the same spreads, but as prices fall, we have to use less working capital to do it…and then in our manufacturing businesses our input costs are lower because steel prices are lower.”

The upshot for Worthington is that, in 2016, lower manufacturing costs will continue to level the playing field against foreign imports from countries with low labor costs. Healthy margins and easy access to capital have fueled domestic and international expansion for the company, allowing it to add production capacity in both China and Turkey. In China, Worthington’s plan is to tap into the local market for automatic transmissions and, in Turkey, to develop and deliver products to transport natural gas, which will ultimately be imported into the U.S.

So with all the good news for his industry stateside, what’s keeping Andy Rose up at night?

GEOPOLITICAL RISKS BECOME A BIGGER CONCERN

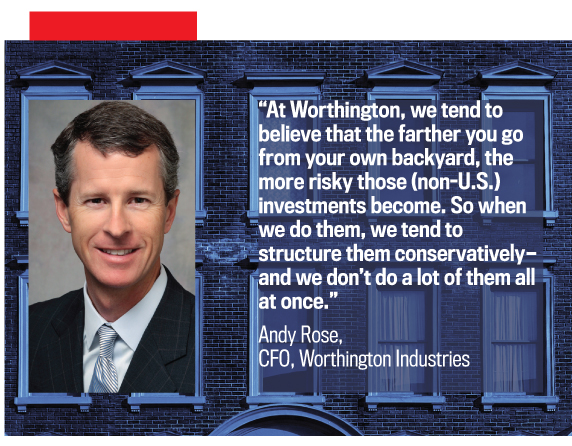

As a risk-averse CFO, Rose takes a cautious approach to expansion outside the U.S. “At Worthington, we tend to believe that the farther you go from your own backyard, the more risky those investments become. So when we do them, we tend to structure them conservatively—and we don’t do a lot of them all at once.”

For Rose, risk management will therefore be given increased priority in 2016; more specifically, he’ll be keeping track of the geopolitical risks in the Middle East. While Turkey is expected to remain a partner, the risk outlook in that region has changed significantly over the last year, with a relatively high terrorism threat and tense relations with its neighbors.

That’s obviously a concern, Rose explains, but adds that the decision to invest in Turkey was strategically necessary. “We didn’t pick Turkey because we thought it was the lowest-risk country,” he says. “We picked it because we found an acquisition opportunity that was of a size we wanted and with the product technology we needed to produce transport containers for the natural gas market in America. There were limited opportunities to find that same technology here in the U.S.”

Over the long term, Worthington intends to build those same manufacturing capabilities in the U.S. In the meantime, Rose’s strategy for mitigating the company’s risk exposure in the region is twofold: First, in order to minimize its exposure to possible disruptions in the supply chain, the company intends to house its inventory in a number of locations, including the U.S. Second, Worthington will explore ways to increase the speed at which the company can build production capabilities in America.

While monitoring geopolitical risk has moved up on Worthington’s agenda, Rose considers cybersecurity to be a top priority, too, not just within the IT department but across the entire company. “Even as a manufacturing company,” he explains, “we have ERP (enterprise resource planning) systems, we use the Internet, we have healthcare…so we have personal information that we have to protect. If you spend any time talking to the cutting-edge innovators in Silicon Valley, they’ll tell you that this is also their single biggest issue—and it’s not just for Silicon Valley. It trickles all the way down to Main Street, too.”

As to how issues around cybersecurity impact the finance department, Rose notes that it’s finance’s job to look at what vulnerabilities might exist, the potential for their information to be exposed, and the potential for industrial espionage. “If hackers decide they’re going to target Worthington, and for some reason want to shut down our manufacturing operation or tap into our ERP system, that would materially affect our operations. It also affects the finance function because we use that same system to compile our financial statements.” Rose says that his job going forward will be to ensure the right investments are made to bolster security while the company continues to make employee education around cybersecurity a priority.

DOMESTIC ISSUES ARE WORRISOME, TOO

Companies like Worthington, whose major markets are in North America, aren’t feeling the same pressures as U.S.-based firms that rely on revenue from overseas operations. For publicly traded companies like Hologic, which manufactures medical imaging systems and diagnostic and surgical products, it’s domestic policy that will be keeping its CFO up at night in 2016. More specifically, the focus will be on the impact of recent interest rate hikes on domestic demand, capital markets, and currency volatility.

According to company CFO Bob McMahon, the question for 2016 is going to be around the impact of interest rate increases and, for Hologic, how the capital markets will respond. “My expectation is that we’re going to see a lot more volatility in share prices,” McMahon says. He adds, “At the same time for us, since we have some variable interest rate debt, we are planning for our interest rate costs to rise, and we are monitoring that closely. We also have instituted some interest rate cap hedges to partially protect us.”

In addition, the company will be embarking on a new hedging strategy to protect cash flow against a rising U.S. dollar.

“When you think about a maturing global organization,” McMahon explains, “increasing certainty around results is something that the finance organization has to focus on. So for 2016, we’ll be hedging against currency fluctuations on a transactional basis and taking a much more proactive stance, which is new for us.” Historically, the company has done very little in this area, he adds.

Furthermore, McMahon also points to the impact of increasing interest rates and currency volatility on their customers, which may affect capital budgets and, in turn, may make it more difficult on Hologic’s sales of equipment. “Although we’ve seen capital spending increasing in hospitals and shifting toward larger purchases of equipment in 2015, we expect that to remain flat for 2016,” McMahon predicts.

Complicating matters, because almost one-quarter of Hologic’s sales come internationally, any increase in the value of the U.S. dollar reduces the value of international sales. To help manage these costs, Hologic plans to leverage its current out-of-country capabilities, such as creating more production and sales infrastructure outside the U.S. Not surprisingly, Hologic has its eye on the Chinese market. “It’s my job, as we think about our capital plan, to help come up with a strategy around how we support international growth from facilities outside the U.S.,” McMahon notes.

To get there, the finance department will be providing more business analytics to drive efficiencies in their operations. “Essentially we’re looking to optimize our resources against the backdrop of strong compliance,” McMahon adds. To that end, finance will be working closely with operations to look for ways to reduce cost of goods sold. As he explains, “One of the big areas we’ll be looking at in 2016 is building cost-improvement programs into each one of our plants. In the longer term, we’re looking at whether we have the most efficient operations network, and finance will play a big role in that, too.

“We’re also working with third parties and our strategic vendors, looking for ways to drive things like centers of excellence or shared-service activities.” For example, Hologic will examine how to leverage its lower-cost operating locations, such as its Costa Rica facility, vs. performing the same activities in some of its higher-cost locations around the world.

FACING CHALLENGES ON MULTIPLE FRONTS

Not unlike Hologic, Minnesota-based Polaris Industries, the largest manufacturer of off-road vehicles in the world and the second-largest maker of snowmobiles, owes a large portion of its revenues to exports. As company CFO, Mike Speetzen will have the job of putting together a financial management strategy for 2016 that will allow Polaris to capture demand in emerging markets, manage its exposure to interest rate and currency fluctuations, and maintain a strong internal control environment to minimize risk, all the while being focused on reducing production costs.

Polaris sells products in 126 countries, generating about 15% of sales outside North America. It delivers more than 300,000 off-road vehicles annually, produced mainly in the U.S. and Mexico. It’s no surprise then that the strength of the U.S. dollar has been a challenge for Polaris. “The rising dollar is certainly going to put more stress on our ability to manufacture here and export abroad,” Speetzen says.

As a result, the company will continue to grow its production capabilities outside the U.S. For example, in the last two years Polaris has expanded into India through a recent joint venture to produce a new utility vehicle for the local market. Going forward, the company will be developing production capabilities in China in order to lower its manufacturing costs while still servicing the entire greater Asia continent.

The lure of lower costs aside, companies have plenty of inherent risks with international expansion, particularly as it relates to compliance with local laws and regulations. “The good news is we’re aware of where those risks lie,” Speetzen explains. “As we go into those markets, we’re also very careful about partnering with a reputable company. For example, our joint venture company in India has a very well-established track record of working with U.S.-based and European companies. But we also put a lot of other mitigating controls and processes in place to make sure that we’re not going to put ourselves or our reputation at risk.”

While going global will continue to be the theme for the foreseeable future, ultimately it all comes back to the customer. “I’ll be watching our retail numbers more closely because a lot of our products are for general recreation purposes,” Speetzen adds. “Our off-road vehicle business has been growing double digits up until this year, and we’re now talking about mid-single digits for 2015.” On the commercial side, too, sales are facing a bit of a headwind because of lagging oil and gas production in the U.S. and weaker demand in the farm sector.

Like most companies that have their fingers in many far-flung pies, Polaris reviews its foreign currency exposures on an ongoing basis utilizing both external foreign exchange expertise and internal understanding of cash flow requirements around the world and strives to minimize or eliminate foreign exchange risk through various hedging techniques.

“We’ve got a considerable number of hedges in place for 2016,” Speetzen says. “It’s an active program, and given the large number of countries we sell into, it’s something that we keep a very close eye on. We have a hedge committee, comprised of our treasurer, myself, and our chief operating officer. We go through our hedges on a monthly basis to make sure that we’ve got a really good understanding of what current currency values are vs. forward rates. We then make some decisions around how aggressive or passive we want to be on the hedging strategy.”

Meanwhile, cost management remains a critical issue. While Polaris has grown at a high rate over the past four or five years, it has also added a significant amount of costs, Speetzen notes. With lower growth rates expected for the near term, however, Polaris will be taking a more disciplined approach around discretionary spending. “We’re going to have a lot more discipline in making sure that our costs aren’t outpacing revenue growth,” the CFO says. “We’ll still be making sure we’re feeding the growth pipeline, but we’re going to have to be more discerning about where and what we spend our money on.”

WHAT ABOUT YOUR COMPANY?

For 2016, what’s keeping your company’s CFO up at night will clearly depend on whether you’re expanding internationally, exposed to interest rate and currency volatility, or need to focus on reducing costs and improving efficiencies in a slow-growth economy. Your organization will be lucky if only one of these factors comes into play, but more likely than not you’ll feel the effects of all of them.

One common theme among CFOs I spoke with in preparing this article, however, was that their purview reached across the entire organization from treasury management to operations to systems analysis and control. In other words, wherever risk and opportunity present themselves, the CFO has a critical role to play in the decision-making process.

January 2016