The speed of technological change is disrupting management accounting. Addressing this challenge calls for innovative and creative solutions to reimagine business systems and processes to create value for a competitive edge. Design thinking is a tool and a mindset that can help achieve these objectives.

The concept of design thinking problem solving has been around for decades. It’s only in the last 15 years that it’s seen widespread adoption. Tim Brown, chair and co-CEO of IDEO, a global design and consulting firm specializing in business transformation, put the methodology on the map in 2008. Brown says, “Design thinking is a human-centered approach to innovation that draws from the designer’s toolkit to integrate the needs of people, the possibilities of technology, and the requirements for business success.”

While traditional applications of design thinking focus on increasing customer value and new product development, Gary C. Biddle, professor of accounting at the University of Melbourne, views design thinking as an effective tool to support the management accountant’s role in creating organizational value. He argues that sometimes value-creation initiatives focus on fine-tuning a business model or process that never should have been done in the first place because management accountants got involved too late. Instead, he believes they should ask questions about opportunities for value creation and choose the best opportunities using design thinking.

DESIGN THINKING STEPS

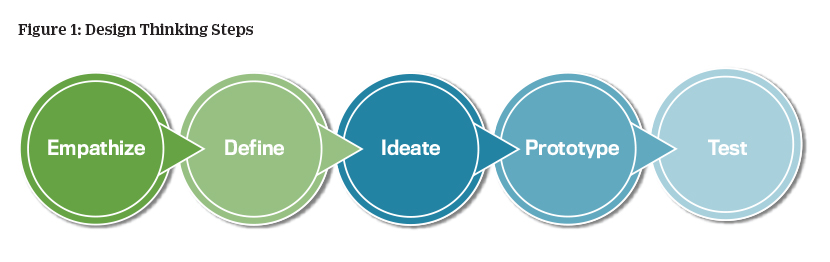

Let’s apply design thinking to developing a new system that leverages technology using its collaborative tools. Design thinking follows a five-step process: empathize, define, ideate, prototype, and test (see Figure 1). The first step, empathize, focuses on connecting to the users experiencing the problem. It requires thoroughly understanding a 360° view of the problem, process, or system needing change.

For example, a company’s basic cost accounting system isn’t integrated with its general ledger, requiring the preparation of manual entries to post monthly inventory and cost of sales transactions. At month’s end, monthly account reconciliations are prepared to balance the two systems. The system hasn’t been updated since implementation a decade ago. It isn’t integrated with other departments’ functions such as supply chain management, sales, quality, and logistics. Data and information requests from other departments are processed manually because the reporting module doesn’t interface with the general ledger. The inefficiency of the system causes errors, confusion, and frustration for users because it isn’t robust. Employee turnover is high; morale is low.

The design thinking team begins by interviewing and observing the cost accounting team’s and other departments’ interfaces to understand current processes. The emphasis is placed on the team’s stories to identify important details (i.e., inventory, quality control, and production scheduling), the current system’s issues and inefficiency (such as the lack of supply chain vendor interface), and how the current system affects the team’s workday and morale. The designers must put themselves in the users’ shoes and should never assume they understand the system based on their previous experience. The designers must start with a clean whiteboard approach.

Define is the second step. Once an understanding of the environment and the issues are identified from the first step, attention turns to refining a definition of the problem. Care must be taken to follow a human-centric approach. For example, using the previous example, it’s tempting to jump to the conclusion that new software is required. That is simply a technical solution to the problem. There may be other processes and features that need to be examined before a decision is made. As noted, other internal users such as the production and sales departments need to be consulted to identify their requirements to ensure a comprehensive system is designed. The company may have budget limits constraining the scope of the project requiring prioritization and project phasing.

Ideate, the third step, focuses on team brainstorming to identify creative solutions. This is the engine of design thinking, to push toward innovation and business transformation. In addition to the accounting department, all stakeholders such as production, quality, sales, marketing, and the design team need to participate. The IT department needs to be at the table to identify tools and processes that leverage the system with technology.

For example, advanced cost accounting techniques such as Just-in-Time, demand planning, and vendor supply chain interfaces are value- creation opportunities. The design team needs to research those opportunities and be prepared to demonstrate how they will create value. Business transformation must be part of the discussion because it will accelerate value creation. All team members must be open-minded about innovative and outside-the-box solutions. Using an online visualization tool (think virtual sticky notes) is an effective way to organize ideas in real time and allows greater participation for virtual teams.

Stormboard’s design thinking templates facilitate structuring and capturing ideas generated during these sessions. Once the ideas are collected, they’re organized thematically (affinity clustering). This step is iterative. Multiple brainstorming rounds are recommended to allow the team to build upon strengths and mitigate weaknesses in proposed solutions.

PROTOTYPE AND TEST

After the ideate step, a testable prototype model of the system or process is developed. Because the design is still a work in progress, the initial model doesn’t need to be complicated. Simple works. A slide show, storyboard, outline, business process diagram, or presentation describing the system will suffice. The objective is to solicit more feedback and refine the model to ensure it meets organizational and users’ needs. The objective is to identify and address opportunities and concerns. The more effort spent tweaking the prototype, the better the design. Like the ideate step, this is an iterative process that benefits from multiple reviews and refinements.

The final step is testing the system. This can range from a working prototype to a full-blown test system of the new design. The system’s stakeholders should participate to reaffirm that their requirements are met. Their participation simulates the new system, provides a hands-on experience, is a closer representation of the final system, and affords another opportunity to fill the gaps in the system.

Many organizations delegate system design away from users. Management accountants live and breathe their systems and have invaluable insight and experience that should be captured in the process. A design thinking approach to system design empowers their participation and is a major step toward value creation.

The views expressed in this article are those of the author and don’t necessarily reflect the official policy or position of the Air Force, the Department of Defense, or the U.S. Government. Distribution A: Approved for Public Release, Distribution Unlimited. USAFA-DF-2022-908.

February 2023