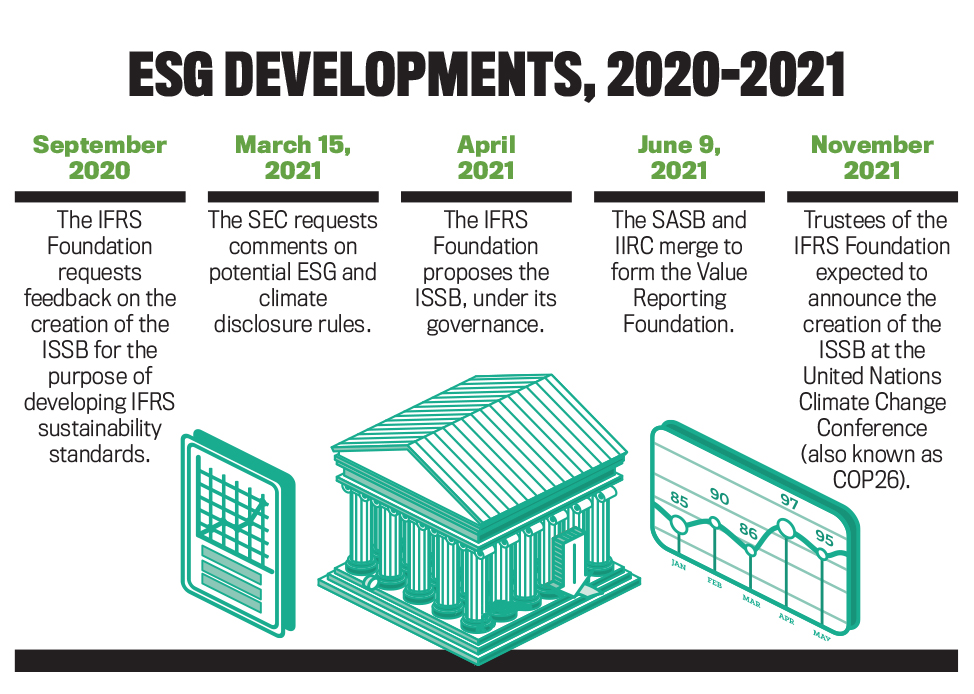

That was followed by an April 2021 exposure draft that included the creation of the International Sustainability Standards Board (ISSB), which would set IFRS sustainability accounting standards under the IFRS Foundation’s governance structure.

The initial September 2020 paper received a whopping 577 responses from around the world, most of which pointed to the conclusion that, as noted in April 2021, “there was indeed an urgent need for global sustainability reporting standards. Moreover, there was broad agreement among the respondents to the Consultation Paper that the Foundation should play a leading role in the development of such standards.”

WHO SETS THE STANDARDS?

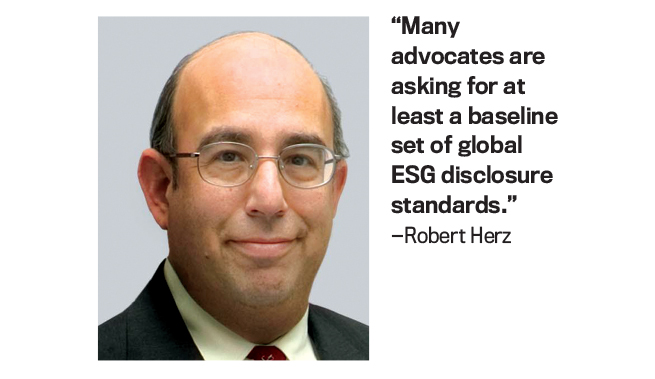

As to why the IFRS Foundation is getting into the game, Robert Herz, a member of the newly formed Value Reporting Foundation board—created by merging the Sustainability Accounting Standards Board (SASB) and International Integrated Reporting Council (IIRC)—as well as former chairman of the Financial Accounting Standards Board, original member of the IASB, and current board member of the SASB Foundation, explains that it’s a matter of comparability and investor demand.

“It’s a bit like the evolution of accounting standards and the demand for first, uniform standards within countries,” he says. “Over time with investing across borders, there were increasing demands for international comparability of the information.”

There’s also been a significant rapid increase in the number and size of the environmental, social, and governance (ESG) investment products that are marketed to institutional and retail investors, Herz explains, but the ESG information disclosure environment hasn’t really kept pace. “Many advocates are concerned that there haven’t been sufficient developments in the marketplace through voluntary disclosure efforts and are asking for at least a baseline set of global ESG disclosure standards.” When it comes to disclosures, “It’s a bit of an alphabet soup right now,” he adds.

The April 2021 exposure draft from the IFRS Foundation trustees also outlined the governance structure of the ISSB. Comments on the proposal were due by the end of July 2021, and, at the time of this writing, the ISSB appears to be a fait accompli. There are many questions yet to be answered (see “Open ESG Questions”), but the new Board’s mandate will be to:

- Focus on information that’s material to the decisions of investors and other participants in the world’s capital markets.

- Initially focus on climate-related reporting while also moving quickly to work toward meeting the information needs of investors on other ESG matters.

- Build on the well-established work of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures as well as work by the alliance of leading standard setters in sustainability and integrated reporting focused on enterprise value.

- Work with standard setters from key jurisdictions, such that standards issued by the new board would provide a globally consistent and comparable sustainability reporting baseline as well as flexibility for coordination on reporting requirements that capture wider sustainability impacts.

GARNERING SUPPORT

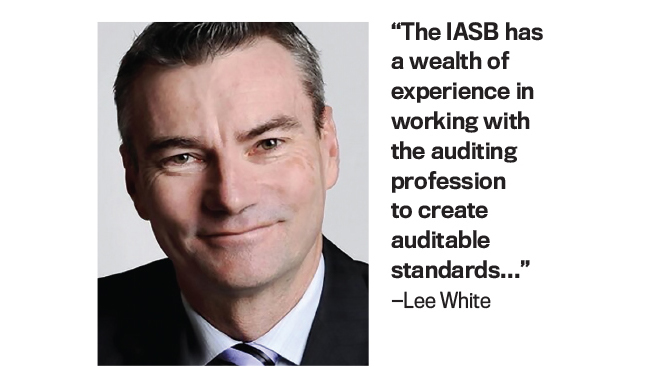

As Lee White, executive director of the IFRS Foundation, explains, the IFRS sustainability standards as developed by the ISSB will be optional for companies reporting under IFRS. “As with the IFRS accounting standards, adoption of the standards and decisions about which companies will be required to apply them will be up to jurisdictional authorities,” he says.

But according to some, embedding IFRS sustainability standards into regulatory requirements is clearly the way to go. In a joint letter to the International Organization of Securities Commissions (IOSCO), the CDP (formerly the Carbon Disclosure Project), Climate Disclosure Standards Board, Global Reporting Initiative, IIRC, and SASB encouraged IOSCO to support ISSB standards built upon their existing frameworks.

They wrote, “Integration [of their guidelines and frameworks] with the IFRS Foundation’s governance and oversightcould deliver internationally-accepted institutional arrangements for sustainability disclosures relevant for the capital markets, ensuring robust governance, rigorous due process and independent standard-setting, within the context of accountability to public authorities who foster outcomes that are in the public interest.”

They also support the ISSB’s standard development agenda and concur that, in order of priority, “The first block of sustainability disclosures would focus on sustainability impacts that affect company performance, risk profile, economic decisions and enterprise value creation. The second block would address all significant impacts on the economy, environment and people, thereby providing a comprehensive picture of a company’s positive and negative contribution to sustainable development and value creation.”

In its carefully crafted response letter to the IFRS Foundation’s September 2020 consultation paper, Consultation Paper on Sustainability Reporting, IOSCO offered a clue as to how the international regulatory environment might evolve, pointing to “the voluntary and high-level nature of many of the frameworks and the lack of binding obligations” that hinder the ability of companies to provide material information to investors and other stakeholders. It therefore “supports the IFRS Foundation Trustees’ engagement in sustainability reporting, including its consideration of the creation of an SSB [Sustainability Standards Board].” This is a significant endorsement, as IOSCO’s members regulate more than 95% of the world’s securities markets.

STUMBLING BLOCKS REMAIN

In terms of ESG reporting, the U.S. Securities & Exchange Commission (SEC) has new regulations that require human resources and capital disclosures. It has also taken a closer look at enforcing existing disclosure requirements that cover climate-related risks, having cited the topic as one of its examination priorities. It subsequently issued a public statement requesting public input from investors, registrants, and other market participants on climate-change disclosures. In addition, the SEC is cochairing the Technical Expert Group that’s working to support the ISSB.

Yet not everyone at the SEC thinks sustainability issues should be within the scope of the SEC’s mandate or the IFRS Foundation’s agenda. According to the ESG subcommittee of the SEC’s Asset Management Advisory Committee, any rulemaking around climate disclosure and ESG reporting should be informed by the SASB standards and the materiality principle as related to business and investor risk alone. In a June 2021 speech, SEC Commissioner Elad Roisman noted that the SEC has no mandate to pursue wider societal or environmental goals, and other commissioners strongly recommend that the IFRS Foundation sticks to its traditional knitting.

In July 2021, SEC Commissioner Hester M. Peirce said, “I understand the allure of setting up a sustainability standards board under the same umbrella as an established international accounting standard-setter, the International Accounting Standards Board (‘IASB’). Nevertheless, the Foundation should avoid this venture into sustainability standard-setting because doing so would (i) improperly equate sustainability standards with financial reporting standards, (ii) undermine the Foundation’s current important, investor-centered work, and (iii) raise serious governance concerns.”

There are potential risks if securities regulators can’t get on the same page when it comes to ESG reporting requirements, as Jeff Thomson, president and CEO of IMA® (Institute of Management Accountants), pointed out in IMA’s December 2020 comment letter to the IFRS Foundation’s consultation paper: “While we observe that European bodies, generally, are driving much of the forward movement, we note that the approach taken by the IFRS Foundation must be global and align with regulatory schema in other jurisdictions, including North America. We do not want to see the development of more silos in corporate reporting which create complexities and costs.”

ENTER THE AUDITORS

Whether the creation of the ISSB and IFRS sustainability standards will achieve harmony in ESG reporting around the world remains to be seen. But what’s fairly certain is that going forward, auditors will be playing a much greater role in assuring the validity and accuracy of external ESG information provided to investors and other stakeholders.

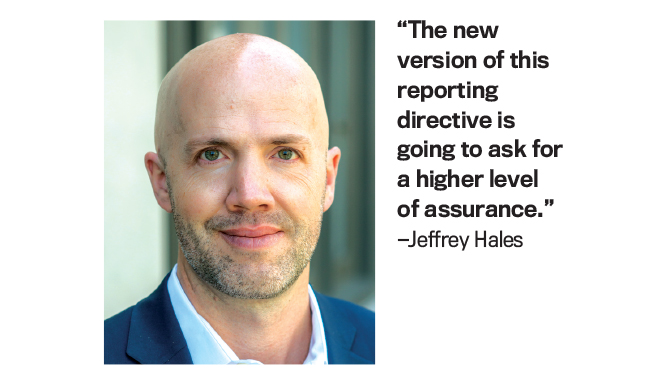

According to Jeffrey Hales, chair of the SASB, for companies that are either located in the European Union (EU) or have significant operations in the EU, the corporate sustainability reporting directive is going to include some type of assurance requirements. “Historically the requirement has been more of an existence check,” he notes. “The new version of this reporting directive is going to ask for a higher level of assurance. It’s possible that IOSCO endorses some higher level of assurance, similar to what’s required when reporting under the IASB accounting standards.”

When it comes to supporting higher-level attestation, the auditors have traditionally had the ear of the king, so to speak. As White explains, “The IASB has a wealth of experience in working with the auditing profession to create auditable standards that the new board can learn from, while also working directly with the International Auditing and Assurance Standards Board and regulators. This will also be vital to enhance the value of information for investors and preventing so-called ‘greenwashing.’”

MORE AUDIT IS BETTER

Accountants are also in agreement that, when it comes to ESG reporting, more audit is better. As Thomson noted in IMA’s comment letter, “We understand that assurance is desirable. We also note that standards can help companies design, implement, and maintain internal controls and oversight to enhance the quality of sustainable business information.... Assurance, confidence, and trust are interrelated and foundational to any corporate reporting system, particularly when speaking about business sustainability. This applies equally to information released externally and information provided to management for decision making on risk, innovation, and strategy.”

Similarly, the International Federation of Accountants (IFAC) concluded that with the IFRS sustainability standards released by the ISSB, auditor’s assurance will not only be easier, but will motivate internal management and boards to revisit their roles in sustainability reporting. “This global approach will also provide a better foundation for assurance engagements,” it wrote, concluding, “A robust, high-quality set of sustainability reporting standards will provide a better foundation for any future assurance standards or methodologies, as well as bring greater clarity and focus on the roles and duties of management and directors who are integral to any assurance engagement.”

The auditors are obviously in agreement. According to Kristen Sullivan, Deloitte & Touche LLP’s sustainability and ESG services lead, the current challenge in performing ESG assurance, whether it’s at a limited or reasonable level, is whether there are “suitable criteria.” Suitable criteria are needed to perform an examination or review, and that’s where standards come in, Sullivan notes. “Companies today are looking for that definitional clarity in the market and this new authoritative body to help define it. Naturally, with a clear standard that really establishes the benchmark, companies will be in a better position to subject that reporting to external assurance.”

ESG IS YOUR BUSINESS

Should IFRS sustainability standards gain widespread traction, not only in the countries represented by IOSCO, but in the United States as well, accountants will increasingly find themselves in the ESG business. When it comes to reporting standards, Thomson concludes that mainstream financial reporting teams need to play an active role in overseeing the quality of external ESG data. He also recognizes the great divide between accounting and sustainability professionals. “One of the most significant challenges that we’ve observed in the market,” Thomson wrote, “are the language barriers between mainstream financial accountants and the sustainability reporting community.”

Can the creation of the ISSB harmonize the current wide disparity in ESG reporting around the world? The leading ESG groups seem to think it’s possible. “We’re hopeful that this is all moving in the same direction,” Hales says, “toward comprehensive corporate reporting on a global scale and that it captures both ESG issues as well as the integration of those topics with regular financial accounting.” (For a look at the recent and upcoming major milestones, see “ESG Developments, 2020-2021.”)

It ultimately depends on the appetite of the regulators and governments to support the work of the ISSB, but there are still serious concerns to address. If left up to voluntary ESG disclosures, investors may still be in the same position when it comes to comparing ESG performance between companies. More specifically, as IFAC concluded, “…market-driven, voluntary reporting cannot achieve relevant, reliable, and comparable information globally, which is what global capital markets require. Nor is it likely to have legitimacy and backing from public authorities.”

For finance professionals, though, that train has left the station. According to Sullivan, developing authoritative sustainability standards under the proposed ISSB is a clear inflection point and inherently brings new accountabilities for the finance function. Accountants and CFOs will need to think about an ESG discipline for their companies through the lens of risk and opportunity, she notes. “First and foremost, in this new environment, finance needs to develop a set of policies, procedures, and mechanisms to drive a consistent level of data management, flows, and controls,” she explains. “While the subject matter may be different than traditional finance information, finance will be required to apply a similar level of rigor and infrastructure around ESG reporting.”

September 2021