Increasing targets after meeting current ones is common. Continuous improvement, stretching, and growth are all positive reasons to increase targets. But there’s a downside to constantly moving targets up. Employees know that they will, in essence, be punished with more difficult future targets if they meet or exceed current targets. Organizations want to improve and push their employees, but employees will restrict performance in the current period in order to avoid substantially increased targets for the next year.

A FEW EXAMPLES

In trying to set effective targets, managers consider current period performance, as well as other factors. Let’s walk through an example of targets, actual current period performance, and the impact of those results on future performance. At the beginning of each year, quarter, or period, managers set targets for their employees. Generally, those targets, if quantitative, are set based on past performance. They are adjusted for current and expected conditions, but past performance matters significantly and employees know that it matters.

Let’s say you’re a salesperson whose quarterly sales goal is $250,000. As this quarter progresses, you’re having an easier time than usual getting commitments from customers. About halfway through the quarter, you see that $250,000 is right around the corner, and you’ll likely end up at $300,000 or $350,000. Knowing that your boss is going to increase your target next quarter if you make the target this quarter, what will you do?

The most likely outcome is the ratchet effect: You will slow down the pace of your work on your sales goal for this quarter. Or you may start working with your customers to take delivery next quarter. You will lock in the sales and commissions for this period, but you won’t want to exceed the target significantly even though you can. You’ll avoid achieving $300,000 and certainly $350,000.

Academic literature is rife with examples of employees restricting current period output in this way when faced with increasing future expectations. If performance is above expectations, employees may increase income—offsetting discretionary accruals, like the allowance for doubtful accounts or inventory obsolescence, to make next year’s target more attainable.

In addition to accounting choices, salespeople who exceed expectations for the first 11 months of the year often reduce output in month 12 in order to “just meet the target” and keep next year’s target reasonable. This output restriction can be costly to the company because valuable potential customers can be lost when salespeople don’t react promptly to opportunities.

It isn’t only salespeople or earnings management. This can impact any job (see “Watch for Red Flags” for indicators that incentives may be missing the mark). For example, in a month-end closing scenario where you’re trying to get quicker each month, if the new target is 12 hours and this month, you’re coming up on 10 hours and will easily finish the closing process, do you do it? Won’t the new target be moved to 10 hours, and then you’ll always be obligated to be that quick? Don’t you want a buffer just in case next month has some unexpected issues? What if this is a onetime occurrence? If you haven’t substantively changed the procedure to always be 10 hours or fewer, finishing in 10 hours sets you up for difficulty—or even failure—in the future.

Click to enlarge.

THE RESEARCH

A recent study by Jasmijn C. Bol and Jeremy Lill published in The Accounting Review reveals a key to keeping employees working hard even when they have achieved their targets: trust. Their article “Performance Target Revisions in Incentive Contracts: Do Information and Trust Reduce Ratcheting and the Ratchet Effect?” found that managers won’t unfairly revise targets upward if there’s trust between the manager and the subordinate, and employees respond by continuing to perform even when they have met their current target. In this way, the Bol and Lill research shows that you can use target setting, ratcheting, and trust in your organization to get the best performance from your employees.

Bol and Lill examined targets, goal achievement, and target revision in a data set of banks from the same cooperative and with the same compensation system, but with each bank operating as an independent entity. Each bank has a separate board of directors that independently evaluates the bank manager and sets the compensation contract and targets.

The cooperative provides a framework to each of the banks for creating the incentive contract for their bank managers. The framework has four categories (employees, customers, financial, and general) with performance measures that are appropriate for each category. Within each category, the banks’ boards select measures, set weights, and set minimums and targets for each measure. This is reviewed each period, and changes to measures, weights, or targets can be made. If the bank manager’s performance exceeds the minimum, he or she receives up to five points. If the performance exceeds the target, then the manager receives 7.5 to 10 points. More points mean a higher bonus and a potential salary increase, so the measures and targets are very important to the manager.

The researchers focused their analysis on one measure—profitability—from the financial category, which is the most commonly used measure across all the banks. Bol and Lill confirm that, when setting the profitability performance measure target for the current year, boards do incorporate past performance on the profit performance measure. Bol and Lill then go on to investigate if there are conditions that limit how much of the performance is incorporated in current targets.

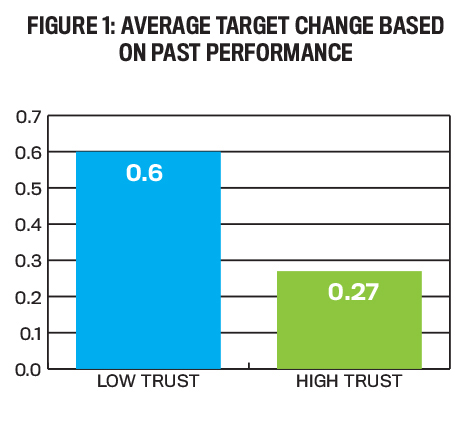

What they found suggests that trust has value in the organizations in the following way: Figure 1 reveals that those managers in a low-trust dyad incorporate about 60% of past performance when revising their targets while managers in a high-trust dyad incorporate about 27% of past performance. For example, assume a bank had a profitability target of 7% and exceeded that target by achieving profitability of 8%. The 1% target-actual deviation would be multiplied, on average, by 60% in case of low trust, resulting in a target in the current period of 7.6%. But with high trust, the 1% target-actual deviation would be multiplied, on average, by 27%, resulting in a target in the current period of 7.27%. Thus, high-trust results, on average, reduced target ratcheting.

Additionally, Bol and Lill found that bank managers keep working toward their targets more steadily when they feel they can trust that their supervisors won’t ratchet targets to a large extent in the future period. Figure 2 shows that if a subordinate has already met his or her target for the year and he or she has low trust with the supervisor, then performance in the current quarter is 87% of what it was in the past quarter. But if the supervisor trusts the subordinate to continue working hard, and therefore doesn’t ratchet the target up, then performance in the current period is 2% higher than what it was in the past quarter.

For example, assume two subordinates have an annual profitability target of 8% and in the third quarter their profitability is 10%. The subordinate with low trust will, on average, lower profitability in the fourth quarter by 87%, resulting in a final profitability measure of 8.7%. The subordinate with high trust will, on average, increase profitability by 2%, resulting in a profitability of 10.2% for the year. This suggests that subordinates who don’t fear target increases answer the question “Given that I’ve hit my target, do I coast until the end of the year?” differently than subordinates who fear target increases. The subordinates in high-trust environments don’t reduce performance as much. They keep pushing.

There are numerous examples like this in the business world of quantitative performance measures that are subject to change over time, prompting employees to withhold performance to prevent the target from being increased too much. Organizations have profit margin, earnings, and return (return on equity, return on assets) targets; salespeople have sales targets; and business unit managers often have targets for return on investments, profit margins, quality, and timeliness. In all these situations, the fear of target increases can adversely affect current performance. If you help design balanced scorecards or performance measurement systems, or if you’re involved in the setting of budgetary targets, then these issues are important to consider.

GETTING IT RIGHT

Research shows there’s a sweet spot for goal setting. In order to provide maximum motivation, targets should be both challenging and achievable, difficult but attainable (see Jan Bouwens and Peter Kroos, “Target Ratcheting and Effort Reduction,” Journal of Accounting and Economics, 2011, pp. 171-185). If targets are too difficult, then employees give up. If targets are too easy, they aren’t as motivating for employees. They need to provide direction but not be completely prescriptive. Setting targets at just the right level is an art.

The target-setting process becomes difficult in the face of information asymmetry. In other words, if the employee has information about the difficulty of achieving the target but the manager doesn’t, then it’s tough for the manager to figure out just the right level to target. Figuring out how to balance the competing demands of target setting is something managers are constantly trying to improve.

Let’s return to the context of month-end closing. Assume that your closing activities currently take 14 hours, and the CFO wants to increase the efficiency of the process. If the new target is too difficult, let’s say four hours, then the closing team will ignore that target and continue with what it has always been doing. If the CFO sets a challenging but achievable target, let’s say 12 hours, the team will work to increase efficiency and make that target. If, on the other hand, the closing team knows that hard work and tweaking a few procedures could lead to an eight-hour close but the CFO doesn’t know that, then it’s unlikely that the CFO will set the target at just the right level.

UNDERSTANDING THE CIRCUMSTANCES

The costs of ratcheting can be significant. Employees may feel justified in withholding performance if adjusted targets are accompanied by no systematic change in their ability to reach that target the next year. Reasons that an employee easily exceeds targets include hard work, a onetime windfall of circumstances, or permanently improved economic conditions. Employees likely believe that the hard work and windfall scenarios don’t justify an increase in future targets, but most would agree that a fundamental change in conditions does justify an increase.

The problem for managers is that with information asymmetry, they don’t know which situation applies to their employees. They’re often left to speculate whether high performance was the result of hard work, a windfall, or a permanent change in conditions and then to determine to what extent the future target should be adjusted. The difficulty is that, to avoid higher targets, employees are motivated to communicate that performance occurred for reasons other than a sustained change in conditions.

Knowing that employees have incentives to hide the truth makes it hard for managers to determine the true cause of high performance. Without knowing the true cause, managers could adjust targets in a way that employees perceive as unfair, causing employees to restrict output in the future (i.e., the ratchet effect). And pressure to perform up to unreasonable goals can also lead to breaches in ethical standards (see “Targets Gone Awry”).

For the month-end closing procedure: If the process is revised and streamlined, then setting the target at 10 hours for the future is fair. But if onetime circumstances resulted in fewer adjustments this period and that ultimately led to a shorter closing procedure, then making the target more difficult seems unfair.

COMING UP WITH SOLUTIONS

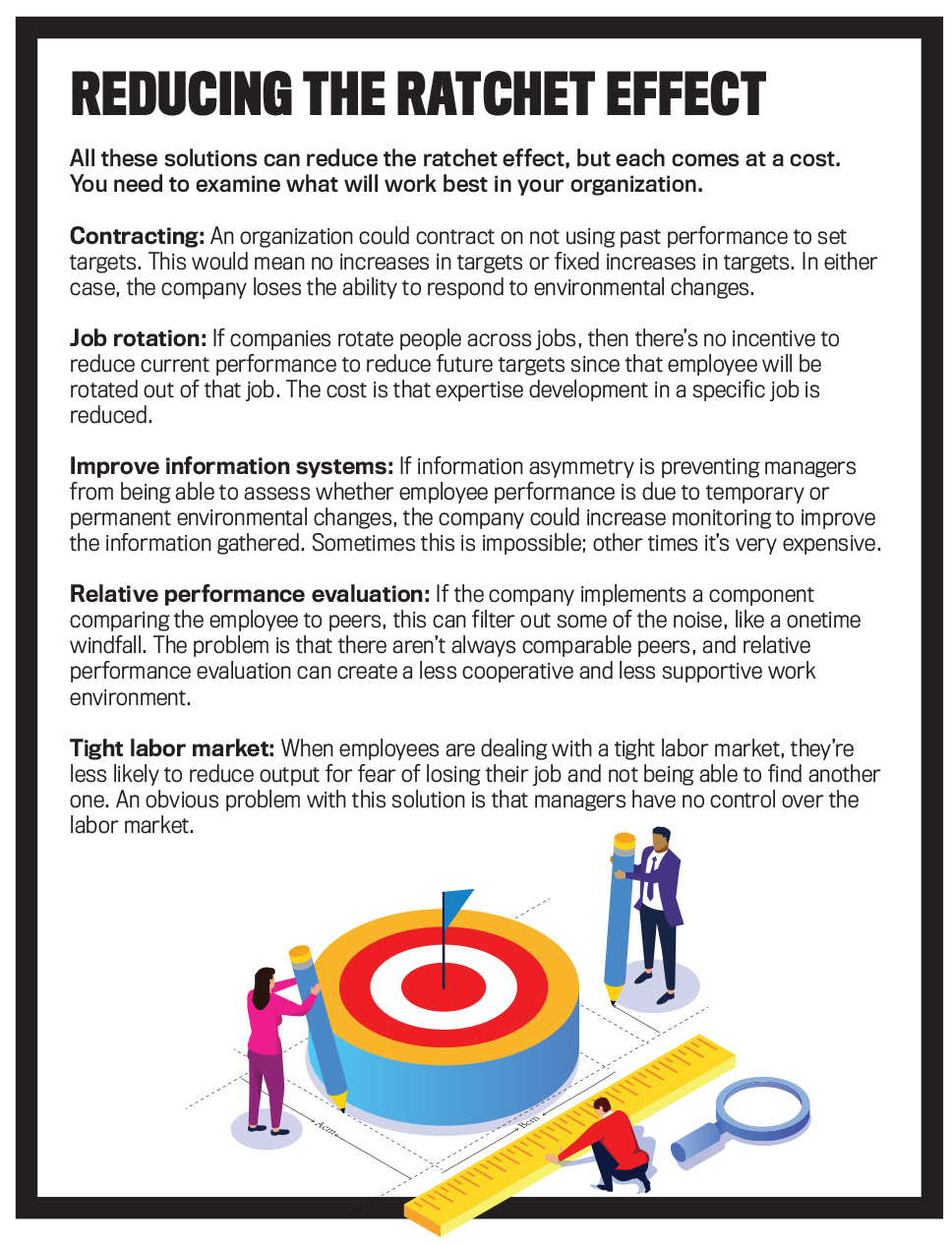

To prevent the ratchet effect, managers need to credibly convince their employees that they won’t ratchet up targets in the face of superior performance or a windfall. Two main ways to convince employees that the targets won’t be increased are contracting and trust. (See “Reducing the Ratchet Effect” for other ways.) First, managers could create a long-term contract with an agreement not to increase targets. While this might satisfy the employee, it would likely be costly for the company to have such a contract. By not increasing targets as the ability to increase output improves (i.e., a fundamental change in conditions), the organization may end up with employees who aren’t working up to their potential but are still meeting targets.

It’s technically possible to write a contract that provides a happy medium that might include partially increasing targets or increasing targets if the employee’s ability to achieve those targets has actually permanently increased. Contracting in such a way would be difficult and cumbersome, as it would have to describe very precisely all possible contingencies, which is nearly impossible to do.

Click to enlarge.

A second approach is to build trust between the manager and the employee. Consider the situation where the CFO writes a contract that states “the closing process target will remain at 12 hours, even if you are able to do better than that.” You can see that this reduces worry for the employee. The employee will still try to close as efficiently as possible. Unlike the costly and inefficient process of writing contracts for every performance measure, developing trust can have a broad effect and encourage employees to work hard.

ESTABLISHING TRUST

A great deal has been written about trust in organizations. Productivity, morale, teamwork, and decision-making speed are all expected to increase with trust. Trust can reduce the cost of transactions, allowing employees to quickly make decisions based on expecting the best of those around them. Trust can encourage employees to use organizational resources wisely toward a shared common goal, and it can encourage employees to follow the leaders in their organization (see Roderick M. Kramer, “Trust and Distrust in Organizations: Emerging Perspectives, Enduring Questions,” Annual Review of Psychology, February 1999).

Without trust, the ratchet effect will likely exist and be costly for the organization. Employees need to be able to trust that their manager will protect them from unfair increases in targets. Managers need to trust that employees won’t restrict output in the current period. When managers and employees trust each other, they can get to the point when targets only increase because it’s “justified.”

In a situation of reciprocal trust, the employee will truthfully communicate why the superior performance occurred. Then trust leads the manager to believe the employee communication and set targets accordingly. Trust facilitates recognition that if people perform well, the next target doesn’t need to go up automatically. If the employee trusts the manager, the employee will truthfully reveal what can be achieved with reasonable effort. Since the employee is truthful, the manager will make sure that there is a fair target and company output will improve.

In our example, if the employee trusts the CFO, he or she will be able to have a conversation saying, “This month we closed in about half the time than we usually do. The transactions were far less complex, and we needed fewer entries. I don’t expect this to persist.” The CFO would understand and keep the target at the same level for the next month.

THE APPLICATIONS

If you increase targets without due consideration of what drove the performance deviation, beware of the ratchet effect. Discussion with your employees about whether this was the result of hard work, a onetime event, or a permanent shift in circumstances will help you understand how much to increase the targets.

Click to enlarge.

You may not get all the information from employees at first, which may make target setting in the face of information asymmetry difficult, but as you continue to dialogue and work with your employees to understand the source of the increased performance, you’ll find a trusting relationship beginning to flourish. There are some important ways to develop trust with your employees (see “Developing Trust”) so that they will continue to work to achieve and beat their targets, even when that’s quite easy. The company will benefit with increased profitability, the employee will benefit with a continued environment in which to strive, and you will benefit by being the manager of a productive employee.

March 2021