And they’re empowering consumers to foster change by redirecting their purchasing power to more sustainable consumption trends, which can in turn, impact how outputs are produced.

Companies are being challenged to create value for their stakeholders, including shareholders, while balancing current societal needs and the preservation of future generations’ needs. The outputs and outcomes produced by corporations are seen by some as litmus tests of their responsiveness to issues of sustainable development. Today, an increasing number of companies are looking to establish a competitive edge by implementing sustainability strategies that can impact both what is produced as well as how it’s produced. Yet this is far from easy.

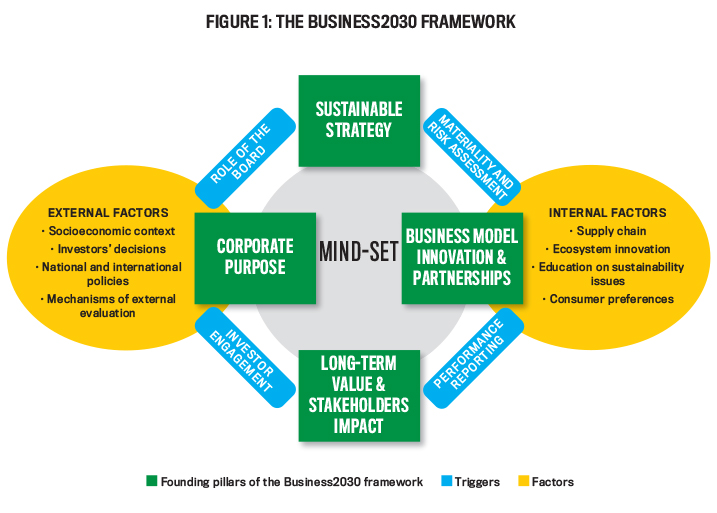

It requires companies to increase the pace in moving from “business as usual” to what we call Business2030 (see Figure 1). Organizations that embrace a Business2030 perspective by aligning their purpose to value-creating strategies not only contribute to society’s efforts to deal with the monumental challenges we face, but also strengthen their long-term competitiveness. Business2030 presents a clear signal that companies can send to their stakeholders that the organization’s goals are linked to the sustainable development goals (SDGs) set by the United Nations in its 2030 Agenda.

Making this shift toward Business2030 requires companies to closely evaluate their value-creation process. Nowadays, value-creation processes are designed through an inclusive process of decision making and management that results in a reporting practice capable of explaining the interdependencies among the multiple capitals deployed. The International Integrated Reporting Council has clustered these features in the term integrated thinking (see “Redefining Corporate Accountability through Integrated Reporting,” Strategic Finance, August 2013). As never before, the adoption of this practice becomes relevant in fostering the mind-set necessary to adopt the SDGs at a corporate level.

While all economic sectors must address these growing needs, the food sector in particular confronts unprecedented challenges. Not only must it contribute to finding solutions to feed the world population, which will grow by more than one-third by 2050, but it must do so while keeping its environmental impact in check. Thus, seeing how companies in that sector are reacting to these challenges—along with the tools and support they’re using—can shed greater light on how businesses everywhere can transition to Business2030.

FOSTERING PURPOSE: THE FOOD SECTOR

In addition to the fact that agriculture contributes up to about 30% of anthropogenic (caused by human activity) greenhouse gas emissions, this sector also provides a useful example due to the number of parties involved in its value-creation process. Agri-food organizations have a large value chain encompassing farmers, suppliers, food processors, research institutions, intermediaries, transporters, wholesalers, retailers, and consumers.

Traditionally, the supply chain of agri-food organizations has been characterized by a farm-to-fork approach, which is the key of the value-creation process. Yet the current social and environmental scenario requires that the supply chain of agri-food businesses be as transparent as possible. Indeed, if consumers are evaluating these companies’ responsiveness to the environmental challenges of our times, this requires that food businesses go from a farm-to-fork approach to a fork-to-farm explanation of how the goods are produced.

The parties involved in the agri-food value chain require companies to provide extensive information on the origin and safety of products. To do so, businesses have been undergoing several different evaluation and certification processes. Yet if the aim is to understand how companies are integrating sustainable strategies, adopting differing metrics renders a comparison in relation to those tools questionable. To this extent, the role of management accountants becomes crucial to validate the use of those evaluation and certification processes.

The report Fixing the Business of Food, which details the efforts of the Barilla Center for Food and Nutrition (BCFN), the UN Sustainable Development Solutions Network (SDSN), the Columbia Center on Sustainable Investment (CCSI), and the Santa Chiara Lab of the University of Siena (SCL) to help the food industry align SDGs and with the 2030 Agenda, identifies four pillars of alignment for the sector: promoting healthy diets; sustainable production processes; sustainable supply chains; and good corporate citizenship.

The study analyzes these pillars to shed light on the sustainability performance of 10 international companies that represent, according to major international rankings, good practices in terms of sustainability. It notes that companies agree in principle on the importance of fostering sustainable development as a core business concept, but what they provide about their operations can be biased and focused on those areas of sustainability performance where companies do better. Thus, more work is needed to ensure that reporting and monitoring systems are more homogeneous and therefore comparable.

Potential areas for improvement include the need for companies to put greater effort into producing more sustainable products and providing information on their nutritional contents to promote improved awareness on the relevance of healthy and sustainable diets. Leading companies should promote solutions to foster the principles of circular economy within their supply chains and a clearer traceability of inputs and production processes. The role played by companies in their social context (e.g., tax practices) should be reported through key performance indicators (KPIs).

Too often, the progress toward the achievement of SDGs is assessed using different time frames, indicators, and criteria. At the same time, it emerged that if more reliable and comparable performance indicators were used in the sector and analyzed by investors, those companies interested in sustainability would be ready to aim at more ambitious environmental and nutritional targets.

Let’s take a look at some of the models of best practices the report identified, including Kellogg’s, Honest Tea, and Barilla.

KELLOGG’S SUSTAINABLE PRODUCTION PROCESS

Kellogg’s is a leading global plant-based food company that operates in more than 180 countries around the world. The company’s main products include ready-to-eat cereals and convenience foods such as cookies, crackers, and cereal bars. The core business of Kellogg’s Company relies heavily upon the use of natural capital and the use of energy for product manufacturing.

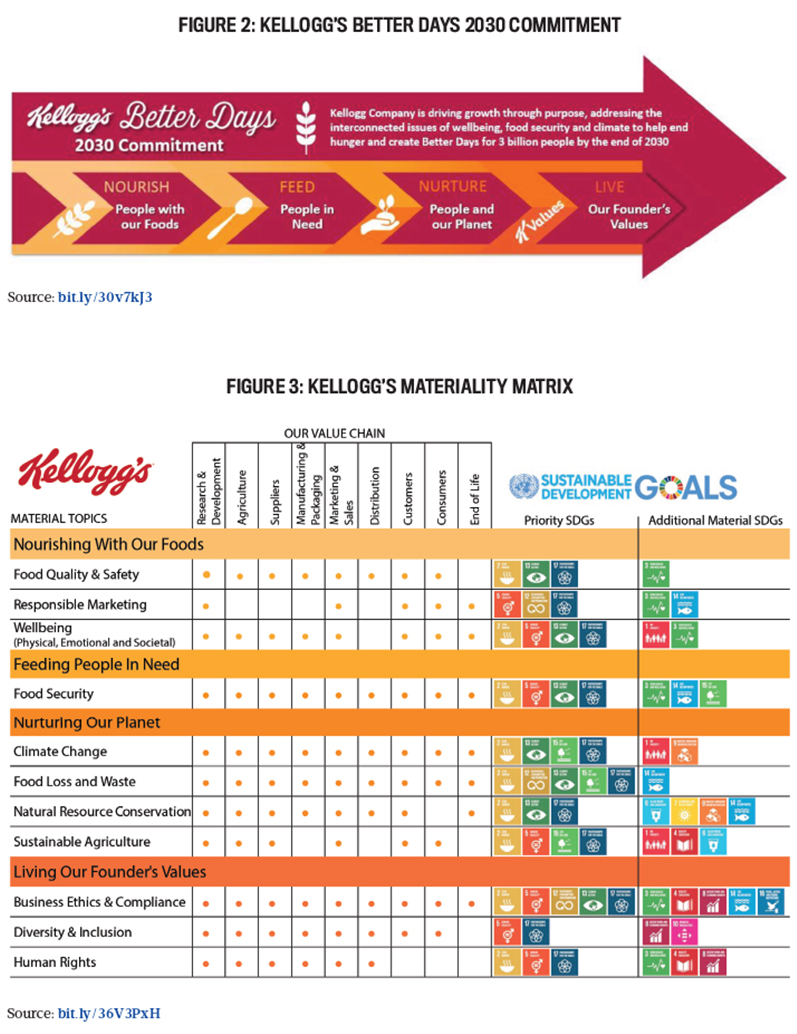

Kellogg’s has based its Better Days 2030 strategy on a strong sustainable value chain that assesses on a regular basis the specific risks linked to the resources used within the production process (see Figure 2).

Click to enlarge.

At Kellogg’s, environmental and global food security challenges have been considered by aligning the performance of the company with SDGs. The company has defined short- and long-term strategies to ensure financial stability while pursuing social and environmental sustainability to create value for all its stakeholders. To implement this strategy, Kellogg’s has been using three levers:

- Undergo a materiality and risk assessment process to thoroughly understand the company’s current and potential environmental, social, governance, ethical, and economic impacts.

Kellogg’s identified topics material to its value chain and focused on assessing those that were aligned to the company’s vision, purpose, strategy, brand portfolio, and geographical footprint. Moreover, it assessed the areas of intersection of its value chain to understand where synergies could be found and addressed how these topics were relevant for its stakeholders and for its value-creation process (see Figure 3).

- Monitor performance against holistic financial, social, and environmental targets.

Kellogg’s ultimate goal is to reduce the risk of disruptions from unexpected constraints in natural resource availability or impacts on raw material pricing. It does so by carefully assessing the management approach it adopts over natural capital. Within this scenario, the company has set the goal of improving efficiency. For example, in its owned manufacturing footprint, it has been reducing water use, total waste, energy use, and greenhouse gas emissions by 15% per metric ton of food produced by 2020 from a 2015 baseline.

- Redesign products to face the challenges linked to food security, well-being, and climate change.

Kellogg’s has committed to responsibly sourcing its 10 priority ingredients as determined by environmental, social, and business risk assessment by 2030. It will do so by partnering with suppliers and farmers to measure continuous improvement. Kellogg’s has been fostering long-term value creation by adopting programs of financial resiliency capable of sustaining periods of economic and environmental stress. As for issues of food security, the company has committed to an internal agenda that sets the ultimate goal of nourishing 1 billion people by producing foods that deliver specific nutrients for those in need and for those who suffer from hunger.

HONEST TEA’S SUSTAINABLE SUPPLY CHAINS

Honest Tea is one of the top-selling organic bottled tea brands in the United States and is carried in more than 130,000 outlets. Coca-Cola purchased the company in March 2011 after making an initial 40% investment in 2008. The acquisition of the company by Coca-Cola helped expand the distribution of Honest beverages, but it represented a challenge in terms of maintaining the Honest Tea mission and product integrity.

The challenge was met by the company with the decision to hire a director of mission to strengthen and keep the company’s values intact. Since his hiring, the director of mission has ensured that the information disclosed within the Honest Tea mission report sheds light upon the latest projects and learnings, thus highlighting successful areas as well as where the company came up short.

First, the long-lasting mission to ensure that all families have access to organic foods has grown to become the effort of democratizing organic drinks. This goal has driven the company to look beyond the outputs produced to acknowledge the impact that the company has on a wider number of stakeholders. Honest Tea has worked to ensure that its ingredients are sourced from organic farmers and bought at a price premium. The premium price set enables Honest Tea’s supplier to invest the cumulative premiums in local community projects, chosen through a bottom-up approach.

The initial shift to this strategy was made possible in part by a cost-saving change in the design of the bottles. In past years, the company has passed down its mission to its consumers by adopting a transparent fork-to-farm disclosure of information.

Second, as a company that produces on-the-go beverages, Honest Tea has faced challenges in its production process. The company’s core business relies on both its natural ingredients and the way in which it stores and distributes them, so it has concentrated on seeking systems that would decrease the environmental impact of its business. In the last three years, the company explored materials that would ensure a sustainable packaging of its products. In 2018, it developed new packaging solutions for the Honest Kids pouches and plastic bottles to include recycled material. Thanks to this initiative, the company decided to shift away from the pouch and toward Tetra Pak packaging, which is widely recyclable in most municipalities. In 2018, about 64% of Honest Kids product sales were from Tetra Pak boxes.

The analysis of Honest Tea suggests that the company has fostered a sustainable strategy that’s translated across its value-creation process. Indeed, the company ensures that the strategy is sustainable across the entire supply chain, especially in the relationships it holds with its suppliers. The premium price at which the company purchases the raw materials for its production process is offset by cutting other costs, e.g., design of the bottles.

BARILLA, DELIVERING PURPOSE

Since its founding, Barilla has become an icon in the food sector, holding 28 production sites and contributing to the production of more than 1.9 million tons of products. Yet the excellence of this company is to be found in how it links its purpose to its performance.

Barilla’s purpose is “to produce goods which are good for consumers and good for the Planet.” The company translates this into the mission of building a world in which the quality and safety of products are the reflection of the well-being of people and of the planet itself. In order to achieve this purpose, the value chain of Barilla is based on four key dimensions:

- Increasing the value of the brands;

- Providing products of superior quality, including from a nutritional point of view;

- Enhancing the sustainability and transparency of the supply chains; and

- Incentivizing an entrepreneurial spirit among Barilla people.

These dimensions are then transformed into two key actions. First, Barilla promotes a healthy Mediterranean diet with its products (using selected raw materials; clean, safe recipes; and balanced nutritional profiles). To this aim, the company communicates the nutritional profile and lifestyle of the Mediterranean diet to the consumers through additional services.

Moreover, in order to continually improve existing products or launch new products that are healthy and sustainable, in 2009 Barilla created its nutritional guidelines. These guidelines are updated every three years based on internationally established dietary guidance (e.g., “Dietary Guidelines for Americans”). Barilla’s Nutrition unit also collaborates with the Health and Well-Being Advisory Board, an advisory body made up of international experts in nutrition and various other fields of medicine. And to measure the effect of applying the guidelines, the Nutrition unit calculates the Barilla nutrition index by classifying its product portfolio into three categories: Joy for You, Better for You, and Good for You.

The second action is Barilla’s effort to improve the sustainability of its products by responsibly managing all processes from field to fork, purchasing ingredients and processing them in a way that’s sustainable; transparent; and respectful of people, animals, and the environment. Barilla leverages its corporate purpose to fine-tune a sustainable strategy to be adopted within its business model.

The company’s transition toward a Business2030 mind-set begins with its definition of the corporate purpose, which is then reflected in its annual reports. Barilla has translated its purpose into its “Good for You, Good for the Planet” mission and aligned it with the production of goods focused on fostering healthy and sustainable dietary patterns.

Barilla’s mission is operationalized in a sustainable raw materials supply chain, governed by the Barilla Sustainable Agriculture Code, a document that describes the sustainability criteria used for making purchases. The code is based upon five fundamental principles that govern the entire supply chain of the company: seeking efficiency and competitiveness in the production system, protecting business integrity and enforcing the code of ethics, promoting food health and safety, reducing environmental impacts, and listening and working together for continuous development.

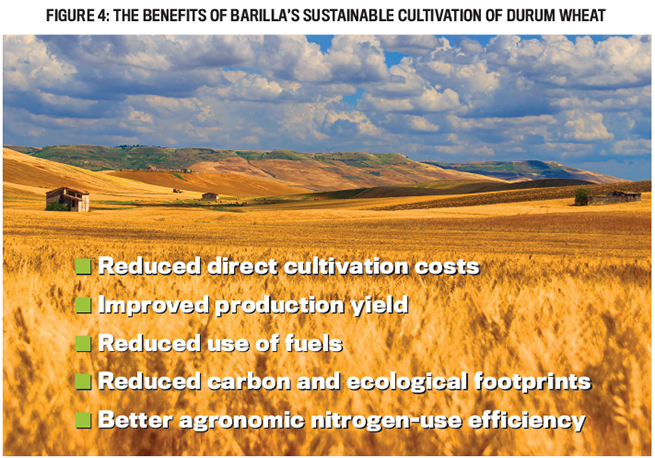

These principles govern the supply chain of the flagship product of the company—pasta. And if the flagship product is pasta, then the strategic raw material of the group is durum wheat. One of the great drivers of the Barilla sustainable supply chain is represented by the company’s supply contracts (see Figure 4). The company sources 89% of its durum wheat locally, out of which 36% is supplied by Italy.

For the Italian segment, the management of the supplying contracts of durum wheat has been part of a long process aimed at favoring the Italian supply chain of pasta. This process started with the first contract proposal between the company, local supplier consortia, and the region of Emilia Romagna back in 2006. This first agreement established the deliveries, increased quantities, and set long-term quality enhancement projects. The agreement to increase local sourcing and decrease transportation costs while fostering local economic growth was signed at a later stage. Then, due to price fluctuations on durum wheat, Barilla included an additional price premium, incentivizing local farmers to sell the durum wheat to the company. The supply contracts had by then evolved to include a variety of different contracts.

In 2017, new cultivation contracts, which covered 67% of the tons purchased by the company, bound the company to acquire 900,000 tons of the strategic raw material from Italian farmers. This corresponds to an investment of €240 million. In 2018, the company signed an agreement with the Crédit Agricole financial institution to allow the group’s suppliers to receive direct loans under competitive financial conditions, no matter their membership to consortia. In 2018, 67% of the tons of the durum wheat purchased by the company were under cultivation contracts.

The company has been ensuring a sustainable cultivation of durum wheat through collaboration with HORTA, a spin-off of the Catholic University of Piacenza, which has supported the company in the creation of the Barilla Decalogue for Sustainable Cultivation of Quality Durum Wheat and granoduro.net. These practices have resulted in a number of benefits for the company, including reduced direct cultivation costs, improved production yield, reduced use of fuels, reduced carbon and ecological footprints, and better agronomic nitrogen-use efficiency.

PURPOSE-DRIVEN ORGANIZATIONS

Aligning corporate performances with the 2030 Agenda and SDGs requires a deep process of integrated thinking that begins with the definition of the company’s purpose. That has to be translated into a coherent company mission and executed through long-term value-creating strategies. Setting its purpose is therefore the starting point for a company to embark on its Business2030 journey. When an organization is able to answer to its “why,” it’s capable of transforming societal and environmental challenges into corporate opportunities.

The food-sector companies analyzed here transformed challenges into opportunities by linking their purpose to their performance through an integrated approach, leading to the creation of sustainable strategies able to foster corporate competitiveness and long-term performance. Understanding the needs of stakeholders and fostering the right approach to trigger the required internal change was fundamental. This can be done in several ways:

- Kellogg’s understood the needs of its stakeholders, mapped them, and translated them within its value-creation process;

- Honest Tea leveraged its strong corporate purpose to implement a sustainable strategy to tailor specific relationships within its supply chain;

- Barilla began from a clear and company-wide definition of its corporate purpose based on the values of the family owning it and translated it into its relationship with stakeholders.

THE ROLE OF MANAGEMENT ACCOUNTANTS

Kellogg’s, Honest Tea, and Barilla are all engaged in fostering their competitiveness through sustainable strategies. This is a complex task that requires the ability to integrate sustainable growth within the perspective of long-term value creation, governance systems, and management mechanisms. It’s within such areas that management accountants can take a leading role to operationalize the reporting practices that align corporate purpose with a company’s sustainable and value-creating strategies and communicate that information to stakeholders. When this occurs, reporting practices can be used to clarify the internal processes that lead a business organization to embed SDGs.

If integrated thinking is crucial to lead companies from business as usual to Business2030, management accountants are the key enablers of this process by promoting a holistic perspective and supporting a company in aligning competitiveness and sustainable growth. Management accountants are able to share and implement best practices in measuring, reporting, and assessing value-creating strategies that could incentivize the transition to Business2030.

One challenge in this effort is the growing number of institutions and organizations that issue standards, guidelines, and certifications. Several organizations and frameworks have been created to foster the alignment of businesses to sustainable practices. Indeed, the danger is having a number of overlapping standards whose scope is unclear. In response to these varying standards, guidelines, and certifications, management accountants can help capture and mold behaviors, actions, and outcomes. By using tools, ad hoc measurements, and KPIs, management accountants are able to ensure that the company is implementing a sustainable strategy. Within this area, the finance organization and CFOs are of the utmost importance in ensuring that:

- The corporate purpose is reflected in the strategy and objectives of the company;

- Performance measures capture the whole value-creation process and are aligned to a sustainable supply chain;

- Incentives foster long-term value for all the stakeholders of the business organization; and

- Management accounting practices are used to enable holistic thinking, which fosters a purpose-driven-mind-set.

Finance organizations and CFOs may enable new conversations and support purpose-driven organizations to detect the right resources, engage in activities, and communicate with stakeholders, thus leading them to a comprehensive business model. Fostering a different approach is crucial when analyzing a company’s business model, for it enables a shift from focusing on business outcomes to focusing on how those outcomes lead the company to have an overall positive impact. It’s of the utmost importance to shed light on the impact that these processes have upon all stakeholders, beyond investors. CFOs have the ability and skills to foster the holistic approach that enables change to occur, to enable a smooth transition to Business2030.

This article is part of the Creating Long-Term Sustainable Value series launched by the October 2018 Strategic Finance article “Creating Greater Long-Term Sustainable Value” by Mark L. Frigo, with Dominic Barton, and an extension of the December 2018 Strategic Finance article “Toward Business2030”.

February 2020