Companies establishing more sophisticated accounting procedures and policies related to their use of cryptoassets must confront a number of internal control and financial reporting issues separate from those of traditional currencies, intangible assets, or other investments.

When analyzing cryptoassets, it’s important to distinguish between core characteristics and control-based applications. Blockchain, at the core of the idea, is a platform and technology system that enables the nearly instantaneous transfer of information in an encrypted manner between network participants. Clearly the increased security and encryption associated with blockchain reduce some of the risk associated with potential unethical actors, but additional controls, disclosures, and reporting practices must be factored into the accounting and reporting process.

We’ll take a look at some of the related key areas, including control considerations, factors related to digital currency custody, and elements that arise as crypto businesses become increasingly integrated into commerce at large. We’ll finish with an analysis of the current legal regulations and financial reporting implications.

CONTROL CONSIDERATIONS

As companies enter into custodial and financial advisory services connected to digital currencies, an analysis needs to be made as to what types of blockchain platforms will be utilized. While public blockchains, like those underpinning bitcoin and ether, may have seized the narrative with regards to blockchain development and implementation, the majority of enterprise applications that companies adopt are going to be based on private, permissioned, or consortium-based blockchain platforms. These private models provide more control to the parties establishing the blockchain and allow a more stringent vetting process to determine what other entities may access or post to the blockchain.

Different types of blockchain platforms require different levels of security, investment, and resources, and they have different implication models from an operational perspective. As different organizations launch services based on providing custodial services, financial services—including investment advising—and control issues surrounding these services need to be accounted for, including:

- Who has approval rights?

- What consensus mechanism will be implemented?

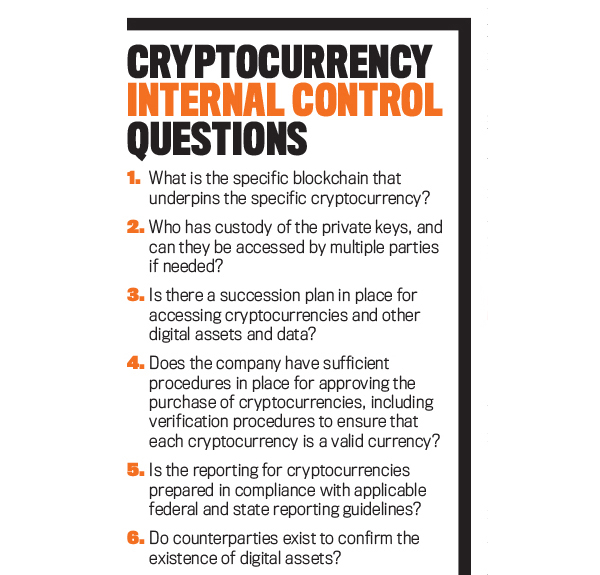

- To what degree will the organization and its auditors rely on the information posted to the blockchain? (See “Cryptocurrency Internal Control Questions” for additional questions to consider.)

Reza Mahbod and Darius Hinton note that, as with any accounting database or new technology platform, organizations employing the technology must ensure that proper segregation of duties and access stratification are established (see “Blockchain: The Future of the Auditing and Assurance Profession,” Armed Forces Comptroller, Winter 2019).

If clients are depositing various cryptoassets with different financial institutions—a practice already occurring—how do the controls over these assets enable proper attestation and assurance? Companies must establish duties that separate access to the assets, approval of their transfer, and recording of the transactions related to them. Control issues related to these areas would include access to private key information, verification related to the custody of different amounts, and valuation concerns, including where the price information of different cryptoassets is listed. As it relates to private keys and access controls, organizations possessing the cryptoassets must have multiple parties with knowledge of where the key is stored so that if the holder becomes unable to perform his or her duties, the organization can still access and utilize the assets.

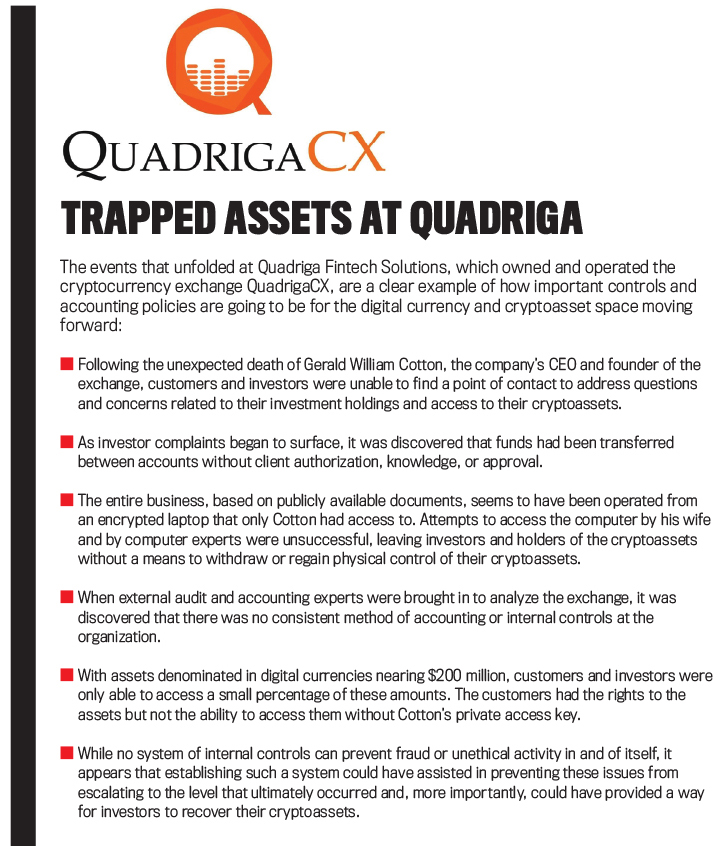

Additional considerations connected to offering more comprehensive custodial services and products require understanding which employees (if any) at the company have access to the underlying code driving the blockchain itself, the protocols for updating or modifying the code of the blockchain, and how the application programming interfaces connect the permissioned blockchains to existing software tools. Each of these considerations should be assessed, documented, and tested for design and operating effectiveness if the company is to rely on them. (“Trapped Assets at Quadriga” provides an illustration of the dangers of relegating control concerns to an afterthought.)

Click to enlarge.

In terms of disclosure and reporting, we believe that control considerations and policies surrounding cryptoassets should be disclosed to investors, regulators, and lawmakers alike. In addition to the business benefits connected to increased transparency, this can also provide an additional safeguard against lawsuits and other shareholder actions.

FINANCIAL STRUCTURES AND DIGITAL CURRENCY BUSINESSES

Operating a blockchain platform, establishing a digital currency business, or possessing cryptoassets create potentially overlooked risks that can hamstring even the most promising organizations if they aren’t proactive. No analysis of the regulatory updates or changes is going to be complete or exhaustive, but there are several themes that are going to have a direct impact on digital currency financial services applications. While recognizing that the digital currency market is global, we focus on considerations for U.S.-based organizations.

Although there remains some ambiguity regarding how blockchain and various cryptoassets should be treated under different legal jurisdictions, the considerations included within this analysis can be applied across the board. Presently, the International Accounting Standards Board (IASB) is reviewing the accounting treatment for such assets and appears to be leaning toward an intangible asset approach or off-balance-sheet classification. This lack of consistency, while presenting challenges for organizations seeking to offer services, also provides an opportunity for proactive organizations to obtain a leadership position.

The vast majority of financial institutions, such as Fidelity and other asset managers operating in the blockchain and digital currency space, operate as a legal trust. There’s one substantial difference between a trust and a bank that can make a difference from a reporting, risk management, and internal perspective. Operating as a trust requires seeking trust licenses in individual states within which the firm wants to operate, increasing the localized risks associated from a compliance perspective.

Alternatively, operating as a banking institution reduces the regulatory and compliance burden since banks don’t have to file for licensure in each individual state. The importance of these differences can be boiled down to the controls and policies that need to be put into place to secure different classes of cryptoassets and the roles and responsibilities that audit and attestation professionals will assume as this market continues to develop. Additionally, the reduced complexity that’s achieved by using a banking institution as the custodian enables practitioners to leverage existing controls and standards vs. having to build entirely new controls and control policies related to cryptoassets.

Another option that’s in its early stages is the concept of a specialized entity constructed specifically for the handling of cryptoassets. Benjamin Bain notes that this appears to be a viable option for organizations looking for an alternative operating structure (“Wyoming Aims to Be America’s Cryptocurrency Capital,” Bloomberg Businessweek, May 15, 2018). Since the entity is so new, its specifics are still being clarified.

It’s also important for practitioners to take into consideration any new challenges—which may create future opportunities—specifically related to digital currency-based business models. First, how are the different cryptoassets held on behalf of clients actually secured or verified? This involves a number of different control considerations, including the appropriate sourcing of asset prices, verification of digital currency wallet ownership, and the ability to verify and confirm that the wallets and contents that are presented as under administration actually agree with amounts that are objectively verifiable.

Second, are any of the counterparties that are indicated as involved via footnotes or other disclosures able to be contacted to confirm or deny the amounts presented in the financial statements or other filings? This may be antithetical to some of the most enthusiastic early adopters of blockchain technology, who believed the decentralized structure and lack of institutions was the future of the technology, but the sharing of information between network members and external audit professionals will need to occur in order for the market to continue to develop.

Last, and arguably the most important of all, is the reality that controls, custody, and disclosure of the various risks and challenges that may accompany a new form of doing business will require a more comprehensive approach to creating and delivering these advisory types of services. Controls, including the design and testing of controls and the reporting of control information, may not always seem like the most scintillating part of the digital currency conversation, but they’re something that must be taken into account as cryptoassets and blockchain technology continue to become more closely integrated into the financial services space.

BALANCE SHEET CLASSIFICATION

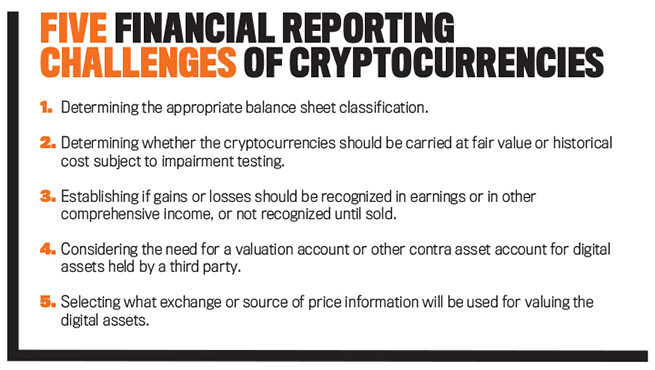

Companies and organizations that elect to accept, possess, or invest in digital currencies or other cryptoassets are currently offered little guidance on how these assets are to be presented for financial reporting purposes. Presently, there is no direct authoritative guidance by the Financial Accounting Standards Board (FASB) regarding how companies that possess cryptoassets should recognize, record, or report these assets. Thus, CFOs, corporate accountants, and public accounting firms have been left responsible for making the determination. (See “Five Financial Reporting Challenges of Cryptocurrencies” for some of the crucial financial reporting challenges.)

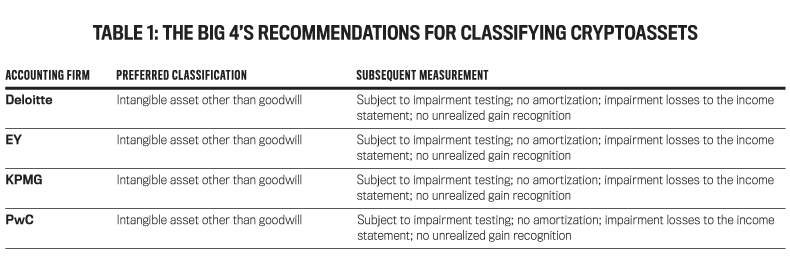

As noted by The CPA Journal, the prevailing opinion recommends treating digital assets as indefinite-lived intangible assets (bit.ly/2LShUE6). A review of white papers detailing the treatment of digital assets issued by the Big 4 accounting firms finds that they’re also in agreement about the treatment of cryptocurrencies under current GAAP: They recommend that cryptoassets be treated as intangible assets not subject to amortization or fair value accounting and that the assets be subject to periodic impairment testing (see Table 1). Interestingly enough, all of the Big 4 recommend classifying cryptoassets as intangible assets, an existing reporting taxonomy, rather than creating a new asset class or category.

Click to enlarge.

Click to enlarge.

In their March 2018 white paper (pwc.to/2NrWVsH), PwC did note that they believe recording the assets as intangible assets, measured at fair value, with changes in fair value reported directly to earnings through the income statement, would better reflect the economics of cryptocurrencies. And they encouraged the FASB to undertake a project to consider accounting for cryptocurrencies.

Digital currencies are unique assets that don’t fit neatly into a singular asset class. Based on the usage and characteristics of these assets, we have identified four potential balance sheet classifications: investments, cash and cash equivalents, inventory, or intangible assets other than goodwill. We will address each classification individually and provide our recommendations. (Note that we’re focusing on cryptoassets held by noninvestment firms, i.e., companies not in the routine business of buying and selling stocks, bonds, cryptoassets, and other holdings.)

Investments. FASB Accounting Standards Codification (ASC) 320, Investments—Debt and Equity Securities, and ASC 325, Investments—Other, provide guidance on how to classify investments in debt and equity securities and other investments that represent a share in either the equity or debt of a corporation, subsidiary, joint venture, or other noncontrolled entities. This guidance doesn’t include any mention of investments in assets not tied to the equity or debt of another entity. Despite companies “investing” in cryptoassets, this omission seems to preclude companies from classifying digital currencies held for speculative purposes as investments.

Cash and cash equivalents. The FASB ASC Master Glossary defines cash and cash equivalents as currency and “short-term, highly liquid investments that have both of the following characteristics: (a) readily convertible to known amounts of cash and (b) so near their maturity that they present insignificant risk of changes in value because of changes in interest rates.”

The name “digital currency” implies that the asset is used in payment transactions and is an acceptable form of settling up between entities in a business transaction. The term “currency” has long referred to those currencies backed by a government or bank, such as U.S. dollars, euros, or Chinese yuan. These are accepted by governments, banks, and consumer businesses alike. This is in stark contrast to digital currencies, where very few merchants accept digital currency for business transactions.

Additionally, the U.S. Internal Revenue Service (IRS) treats digital currencies as property for tax purposes, requiring gain recognition when converted to U.S. dollars. Given these considerations, digital currencies are neither currency in the traditional sense, nor are they cash equivalents because they aren’t readily convertible into cash and don’t require settlement in cash. Because of these differences with the FASB’s definition, we don’t believe classifying as cash and cash equivalents to be appropriate.

This topic may be worth revisiting in future research, as several U.S. states are either enacting or considering legislation that would enable institutions and individuals to settle debts, including taxes, via bitcoin. Being able to settle debts, and especially the ability to pay taxes, is a defining characteristic of items classified as currency.

Inventory/commodity. Many digital currencies are created via an algorithmic process called mining. Because the total number of available digital currency is often fixed (like with bitcoin), each time a currency is mined, it becomes harder to mine the next coin and the available supply is reduced by one. Even though this process occurs virtually, it’s similar to the mining process that occurs for oil, natural gas, and other nonrenewable resources. When these commodities are mined, they’re recorded at their cost to produce and classified as inventory.

ASC 330, Inventory, states that “inventory has financial significance because revenues may be obtained from its sale, or from the sale of the goods or services in the production of which it is used. Normally such revenues arise in a continuous repetitive process or cycle of operations in which goods are acquired, created, and sold, and further goods are acquired for additional sales.”

For the majority of companies, cryptoassets aren’t the primary revenue source for the company and therefore don’t routinely represent a “continuous repetitive process.” Most of the companies also didn’t mine their cryptoassets; they merely possess them. Given these considerations, unless the company is in the business of mining and selling digital currencies as part of its regular business cycle, we don’t believe that inventory is an appropriate classification for cryptoassets.

Intangible assets other than goodwill. An intangible asset is an asset that lacks physical substance. ASC 350, Intangibles—Goodwill and Other, requires intangible assets that aren’t developed internally to be initially recorded at the acquisition cost. Subsequent recognition depends on the life of the intangible. Definite-lived assets are amortized over the life of the asset, while indefinite-lived assets are not amortized and instead are subject to impairment testing at least annually.

Digital currencies, by definition, lack physical substance. They exist digitally within a public blockchain and can’t be stored, transferred, or obtained outside of the digital space. Even digital coins or tokens that are issued or connected to a private or enterprise blockchain model, such as JPMorgan Chase’s JPM Coin, still lack physical substance and exist only in digital form. They also have no termination date, expiration date, settlement date, or defined life. Therefore, the guidance in ASC 350 would seem the most applicable to digital currencies.

Impairment testing after the initial measurement would be undertaken by observing the recent traded prices on various digital currency exchanges. Under ASC 350, if the costs to acquire the digital currencies were greater than the recent exchange prices, the asset would likely be considered impaired and an impairment loss would need to be recorded. Yet the classification as intangible asset requires that if the price on the exchange in future periods exceeds the costs to acquire the digital currencies, no gain is recognized and the asset remains at its acquisition cost.

We believe that, short of any updated standards issued by the FASB, cryptoassets most closely resemble intangible assets other than goodwill and should be classified as such. While cryptoassets share many characteristics with inventories and cash and cash equivalents, there’s the most overlap and least disqualifying factors related to classification as intangible assets.

In terms of measurement, the speculative nature of digital currencies may lead some to believe that fair value measurement, with subsequent changes in fair value recognized in earnings, to be the most appropriate measurement approach. Given the existing FASB guidance, however, we don’t support this for companies that aren’t investment companies. We believe that impairment testing, but not gain recognition, most closely supports accounting conservatism and represents the most appropriate measurement approach given the present guidance issued by the FASB.

REPORTING CONSIDERATIONS

Treating cryptoassets as intangible assets other than goodwill presents challenges related to valuation and collectability risks. Because cryptoassets lack a physical form, they’re stored on the blockchain via a private key either by the company that holds the assets or by the exchange where the assets are offered for trade. There’s no way to recover access to the key if the passcode is lost or the custodian of the passcode becomes unavailable. Without the passcode, the assets are inaccessible and restricted to the blockchain. Because of this unique embedded feature, companies that hold cryptoassets or have the rights to cryptoassets must assess the accessibility to their cryptoassets and understand any restrictions that may arise when they try to utilize their assets. If this assessment identifies recoverability issues, companies may need to consider establishing a valuation allowance.

ASC 210, Balance Sheet, states that “asset valuation allowances for losses such as those on receivables and investments shall be deducted from the assets or groups of assets to which the allowances relate.” Historically, this has applied to receivables, deferred tax assets, and investments. Cryptoassets carried at acquisition cost and subject to amortization may also fit this need if there’s a risk that the asset can’t be fully recovered from the holder. We don’t believe it’s sufficient to merely disclose in the notes to the financial statements that there’s a risk that the asset may not be recoverable. Companies with rights to cryptoassets should assess their ability to access their digital assets by asking the following questions:

- Is the private key stored in a location that can be accessed via alternative means if the storage location is compromised or taken offline?

- Does the company have direct access to the private key, and does more than one person know where the private key is stored?

- If the private key is held by a third-party custodian, does the custodian have controls in place to transfer key access to another party if the custodian is unable to perform his or her duties?

If the answer to one or more of these questions is no, a valuation allowance may be required to account for the risk related to the inaccessibility (similar to collectability in receivables) of the digital tokens and assets.

AN UNCHARTED PATH

Companies that look to possess, transact with, or serve as intermediaries for cryptoassets and digital currencies are entering an undefined area as it relates to these assets’ internal controls over financial reporting and their appropriate presentation on the financial statements. Organizations holding cryptoassets must consider controls and disclosure around the maintenance, access, and possession of these digital-only assets. Companies that possess these digital assets must also determine how they’re going to record the assets on the financial statements.

Consistent with the opinions expressed by the majority of the Big 4, we believe that for the majority of noninvestment companies, cryptoassets are best recorded as intangible assets other than goodwill subject to annual impairment testing. We recognize that there are reasonable arguments to be made for other classifications and other subsequent valuations, but given the current guidance (or lack of) provided by the FASB, this recommendation aligns most closely with the fundamentals of cryptoassets.

Our analysis isn’t meant to be definitive, nor is it intended to firmly establish guidelines for the financial reporting treatment of cryptoassets. But it should give companies entering the digital currency space a reasonable foundation with which to begin their financial reporting policies surrounding these assets. As more information and more uses for the assets become available, we remain open to amending our recommendations and adapting as the technology adapts.

November 2019