The competition is named in memory of Carl Menconi, who held leadership positions in IMA for many years and served as chair of the IMA Committee on Ethics. The objective of the competition is to develop and distribute business ethics cases with specific application to management accounting and finance issues and that use the IMA Statement of Ethical Professional Practice as a reference or guidance tool.

The winning case and teaching notes are available for use in a classroom or business setting. IMA academic members can access and download the teaching notes from the Academic Teaching Notes library via the IMA Educational Case Journal section of IMA’s website: www.imanet.org/educators/ima-educational-case-journal.

Bexley Box Company, Inc., is a privately held firm located in Dearborn, Mich., that was previously a supplier of corrugated shipping boxes to the automotive parts manufacturing sector. The company serviced many producers that were primary parts suppliers to the largest automobile companies headquartered in the United States. Over the past three decades, Bexley’s volume dwindled significantly in correlation with plummeting demand for domestic vehicles by U.S. consumers, creating a mounting overcapacity issue for the company.

In response, Bexley’s CEO, John Easton, sought other opportunities to engage the company’s underutilized capacity and endeavored to become a regional supplier of shipping boxes to SmileNow Distributors, a large U.S.-based internet retailer that established local distribution centers in the Detroit metropolitan area and the Midwest U.S. To become a supplier, Bexley was required to engage in minor retooling of its equipment in preparation for the potential customer’s requirements. To accomplish this, the company’s in-house engineers were able to perform equipment adaptations over the course of months and complete testing during a time of lackluster productivity as a result of decreasing sales orders from its older customer base. The production, engineering, and operations managers then tested the equipment concurrently to ensure it could accommodate the new production schedule for shipping corrugated boxes.

As a result, Bexley’s sales executives successfully presented a supplier proposal to SmileNow. The foremost internet retailer excelling in U.S. market share, SmileNow had just marketed a popular program with the objective of minimizing shipping costs for its loyal customers. The SmileNow! program offered expedited delivery at a reduced annual flat fee. The anticipated increase in sales volume based on projections by SmileNow’s executive team was staggering, representing nearly 400 million corrugated boxes annually.

Bexley’s sales managers were committed to consummating a deal and elevating the company’s capacity to regain status as a sector leader by becoming one of SmileNow’s leading suppliers. Although Bexley wouldn’t be SmileNow’s sole supplier initially, it could eventually achieve this coveted position given a proven success record indicated by quality, performance, and customer satisfaction surveys. Bexley’s independent board of directors was thrilled at the news of this opportunity and commended the executive team, particularly the CEO.

Bexley’s managers and executives were determined to augment the potential of the SmileNow opportunity to the fullest extent. The company’s controller, Harry March, CMA, reports to Easton. March had emphasized the importance of the value chain in providing a methodology to production, engineering, operations, and marketing managers that would allow these business partners to identify the segments that were critical in the maintenance of the customer relationship for the sustainable future.

Managers appreciated the introduction of the value chain ideology and often referred to its tenets when proposing revisions to the engineering and production processes, specifically. March was prepared to provide an extensive and timely feedback loop that would detail efficiency, usage, spending, and production volume variances and result in management behavioral changes if necessary in order to optimize manufacturing. Managers should be incentivized toward achievement and continuous improvement—and guided ethically as well.

March was a seasoned professional who networked frequently with his IMA® (Institute of Management Accountants) colleagues at local chapter meetings in the area. Many controllers who worked in the automobile industry supply chain manufacturing plants in the Detroit area were members of the chapter and shared relevant news regarding financial opportunities. March learned via email from his IMA colleague Tom Sheridan that the state of Michigan was offering property tax relief credits on behalf of manufacturing plants in Wayne County for repurposing facilities formerly dedicated to automotive companies and related industries.

March shared this information with Easton, and together they contacted the state treasurer regarding eligibility requirements. The company was potentially eligible for a 60% property tax credit that would reduce its property tax payments; the state would require Bexley to pay 40% of the property tax bill, and the state would pay the remainder directly to the city of Dearborn.

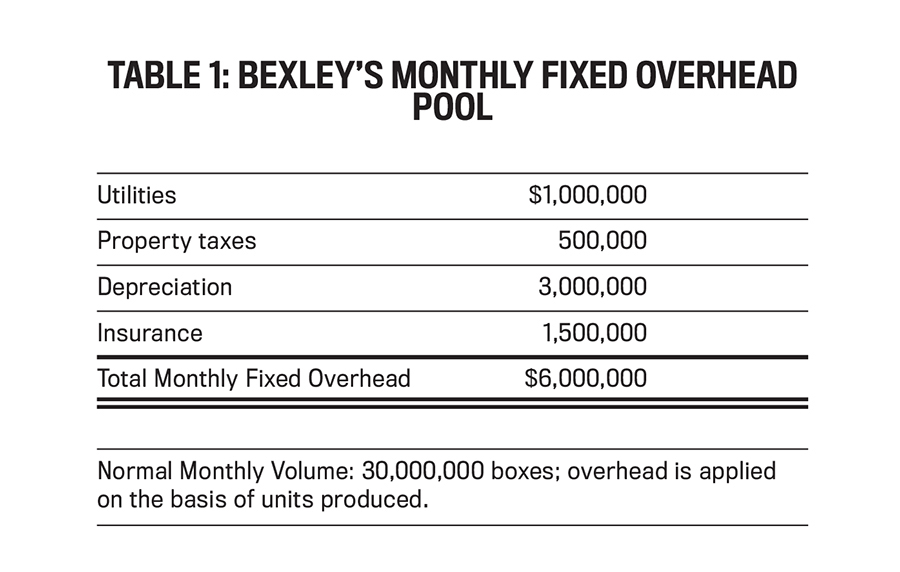

Considering Bexley’s property tax bill was $6 million, it was critical that the fledgling company secure state support. The state requirement stipulated that the company hire at least 500 permanent full-time workers to be eligible for the subsidy; it would be paid and amortized monthly. Although March’s overhead calculations initially excluded the subsidy, Easton assured March that the company would realize the effects of it by year-end vs. the standard cost of SmileNow’s boxes. Easton was certain he would be able to increase the current head count of 1,500 by 500 employees, resulting in the 2,000 employees required to realize the tax relief. (See Table 1.)

PREPARING FOR THE FUTURE

The Bexley management team was convinced that SmileNow would provide the opportunity for growth and was committed to surpassing standard costs. By doing so, the company would not only realize additional profitability but also accumulate resources to augment capacity over time. This would be particularly advantageous since complementary growth alongside SmileNow would ultimately require expansion and capital expenditures, which would be realized after a short time if the standards were successively bested.

Timely reporting thus became a distinct priority for Bexley’s accounting staff. Staff meetings were held with the production area each week to revisit the outcomes of the most recently completed variance analysis reports from completed production runs and to discuss potential process enhancements that would result in incremental efficiency. Since the production runs were lengthy, a possibility existed that a significant amount of production time would elapse without monitoring and variance calculation; the window of opportunity for profitability was thus closed if unfavorable direct manufacturing variances were experienced.

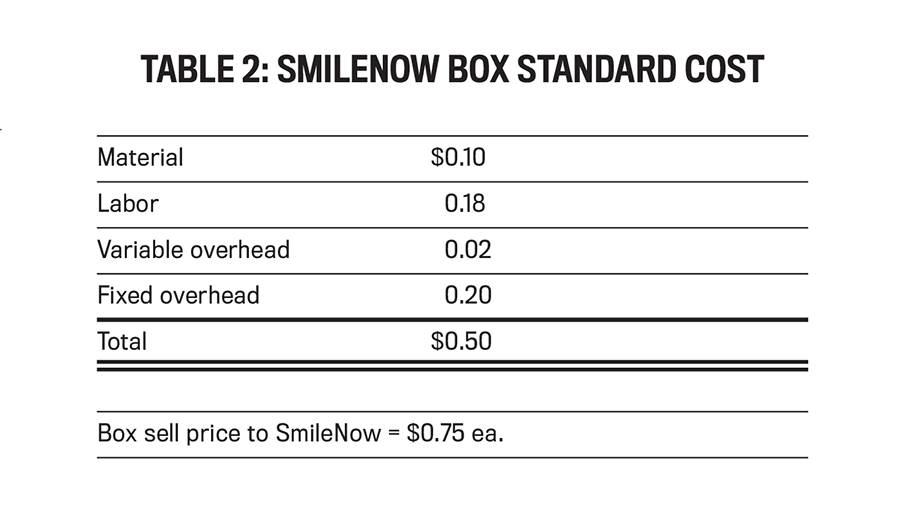

The operations and administrative staff agreed that calculation and dissemination of weekly direct manufacturing variances would be desirable in order to address any inefficiency with alacrity. Accordingly, production and engineering would work toward eliminating and rectifying any problematic manufacturing issues that resulted in underperformance. (See Table 2.)

Stan Kirby, Bexley’s dedicated and valued production manager, was a close colleague of March; together they had weathered the storm resulting from the economic downturn and dearth of demand that affected Bexley’s former sector and that had culminated in a number of middle management layoffs. Kirby had discreetly revealed to March that he was considering leaving the company since he could “hardly afford the mortgage payment, let alone save for my kids’ education and my own retirement if I don’t make my annual 20% bonus.” Yet Kirby was very excited about the potential to meet budgeted operating income totals for the first time in years and once again be eligible for incentive pay.

John Easton was aware of the opportunity to provide an extra incentive for managers due to the procurement of the SmileNow business. A stretch target was established that would provide for an extra 10% bonus for managers if actual operating income exceeded budgeted operating income of $10 million by an additional 10%. Although March was somewhat reticent to agree to this initially, Easton convinced him that it would be advantageous to incentivize the staff and further enhance morale.

As production meetings commenced and regular variance analysis reporting for materials and labor were reviewed for potential improvement, Bexley’s employees became acclimated to the idiosyncrasies of manufacturing the new product line. By the fourth quarter of the calendar year, in October, the challenging learning curve was beaten, and incremental but largely immaterial favorable variances to standard began to periodically emerge despite SmileNow’s exacting standards for quality.

Two months later, March and Kirby were having lunch with Richard Girard, Bexley’s top salesperson, who negotiated the contract between the company and SmileNow. March asked Girard, “What has SmileNow’s reaction been to the new product? Have they been pleased with quality?” Girard replied: “Absolutely! In fact, we are in discussions to potentially add volume in the form of other box sizes to our product line that we manufacture for SmileNow. Talks are in the beginning stages, naturally, but engineering is working on a model and developing a design presently.” Kirby chimed in, “That’s terrific! I’m so pleased that we finally have the opportunity to flourish as a plant again!” Girard agreed: “I believe we all must feel the same way!” March nodded in agreement.

March spent the next week at an IMA regional conference to complete his yearly continuing professional education (CPE) requirements to maintain his CMA® (Certified Management Accountant) designation. While there, he talked once again to Tom Sheridan, who asked if March had been able to apply and realize the tax relief offered through the Wayne County manufacturers’ subsidy. March indicated that the company was working on increasing volume through the new designs, and it was likely that it would be able to take advantage of it in the future. March thanked Sheridan for the information, as it was critical in incentivizing the staff.

AN ETHICAL DILEMMA

The following week was December month-end, and it was time for March and his staff to calculate the monthly variances for fixed overhead. March rationalized calculating fixed overhead variances once a month. Since invoices often arrived late, it was difficult to approximate the applied overhead total and compare it to the fixed overhead components for spending that had been booked either through standard entries for depreciation or estimated monthly utility costs.

But this time, the fixed overhead spending and production volume variances caught March’s attention. He wondered: What happened in the past week while I was at the conference? As he looked at the production volume over the past two weeks, he noted that the SmileNow production runs’ consistent output of 7.5 million boxes per week had increased to 10 million each week over that time. This resulted in millions of additional boxes manufactured for the month and within weeks of year-end.

In disbelief, March went to the finished goods warehouse and found hundreds of pallets of corrugated SmileNow boxes waiting to be shipped. He called Girard and asked whether SmileNow had ordered an increased volume yet as he discussed. Girard replied, “No, we’re still in talks. It wouldn’t be the boxes we’re making currently that would be of interest—we’re responsible for all of that volume, and demand is steady and regulated according to their needs. Any incremental volume would be of another size.”

March’s next question was directed to Kirby, who immediately offered the following explanation: “Yes, after our lunch conversation with Richard, I spoke to John Easton immediately. He agreed that it looked so promising that we could manufacture incremental volume. In fact, I am having my crews work three shifts to keep up with the volume. We even hired more temporary staff to optimize the schedule.” March indicated: “Stan, I just spoke to Richard, and SmileNow is not interested in purchasing more volume of the box we manufacture presently. They are looking to add volume in other sizes. We will have a serious cash flow problem now that the manufacturing schedule has bloated!”

Kirby was adamant in his reply: “Harry, we’ve all waited years to get a bonus again, including you! Most of all, John realizes this and wants us to have a great year-end. That’s why he told me to proceed!”

March walked into his office, locked the door behind him, and collapsed in his chair, pondering his next course of action. As he viewed the paperwork that had accumulated on his desk while he was at the IMA conference, he discovered a note from the payroll manager saying: “Provided the head count of 2,000 employees to state of Michigan for year-end as requested by John Easton.”

Case Questions

- Assume that the tax subsidy was realized initially beginning in December, the company’s year-end. Calculate the fixed overhead spending and production volume variances using a three-way variance theoretical model. Indicate whether the variance results are favorable or unfavorable.

- If the fixed overhead variances were the only differences affecting Bexley’s operating income this period, did the management team achieve its stretch target?

- Given the discovery of additional production so close in proximity to a year-end close and annual audit, why might March be concerned? What should his obligation be regarding the state subsidy?

- Consider March’s role in the organization, the fact that he is a CMA, and the IMA Statement of Ethical Professional Practice. Given the requirements provided by the IMA Statement, what should March do next?

- If Bexley were to “fairly compensate” its managers with incentives given the year-end production levels, how might this be achieved?

July 2019