To attract these investors, companies need to develop, communicate, and execute a long-term value-creating strategy. CFOs, finance organizations, and management accountants can play a pivotal role in helping companies refocus their strategic performance measures and deployment of resources toward greater long-term value creation.

LONG-TERM VALUE CREATION

Readers of Strategic Finance are familiar with the continuing research from the Center for Strategy, Execution and Valuation in the Kellstadt Graduate School of Business at DePaul University that focuses on understanding how high-performance companies create long-term sustainable value in spite of the headwinds of disruptive forces, turbulent economic and regulatory conditions, and distractions caused by the pressures of short-termism when companies focus too much on short-term results to the detriment of long-term strategy.

During the last two decades, the Center’s work has focused on high-performance company research defined in terms of companies achieving superior and sustainable return on investment (ROI), disciplined invested capital growth (consistently reinvesting in the business while maintaining superior ROI), and superior relative total shareholder returns (an outcome of the first two criteria). In other words, these are “long-term value-creating companies.”

Research at the McKinsey Global Institute (www.mckinsey.com/mgi) has studied the impact of short-termism and the advantages of long-term value creation. FCLTGlobal, Focusing Capital on the Long Term (www.fcltglobal.com), is a not-for-profit organization that works to encourage a longer-term focus in business and investment decision making by developing practical tools and approaches to support long-term behaviors across the investment value chain. It is dedicated to rebalancing investment and business decision making toward long-term value creation.

Dominic Barton, global managing partner emeritus of McKinsey & Company, leads the firm’s focus on the future of capitalism and the role business leadership can play in creating long-term social and economic value. In this article, he shares some of his insights and ideas about how companies can create greater long-term sustainable value. As he emphasizes, CEOs, CFOs, management teams, and boards must avoid the trap of short-termism and gain a clear focus and commitment to creating long-term sustainable value.

THE CONSEQUENCES OF SHORT-TERMISM

Frigo: How does short-termism affect company decisions that may work against long-term value creation? What are the ultimate consequences of short-termism?

Barton: We know from FCLTGlobal surveys that 61% of executives and directors say they would cut discretionary spending to avoid risking an earnings miss. And 47% would delay starting a new project in such a situation, even if doing so led to a potential sacrifice in value creation. We also know the pressure of short-termism is intensifying, with 65% of executives and directors saying the short-term pressure they face has increased in recent years.

Some of the possible consequences of excessive short-termism are reflected in record levels of stock buybacks in the United States and historic lows in new capital investment.

At the macro level, while we can’t directly measure the cost of short-termism, our analysis gives an indication of just how large the value of what’s being left on the table might be. If all public U.S. companies had created jobs at the scale of the long-term-focused organizations in our sample, the country would have generated at least five million more jobs from 2001 to 2015 and an additional $1 trillion in GDP [gross domestic product] growth (equivalent to an average of 0.8 percentage points of GDP growth per year). Projecting forward, if nothing changes to close the gap between the long-term group and the others, then the U.S. economy could be giving up another $3 trillion in foregone GDP and job growth by 2025. Clearly, addressing persistent short-termism should be an urgent issue, not just for investors, companies, and boards but also for policy makers.

Frigo: At the company level, CFOs can play a leadership role to refocus performance measures and incentives toward long-term value creation and away from a focus on short-termism. After all, it’s at the company level where long-term value creation actually occurs. This can include an initiative CFOs can spearhead to develop and refine disciplined performance measures that are highly aligned with long-term value creation.

KEY FINANCIAL INDICATORS OF LONG-TERM COMPANIES

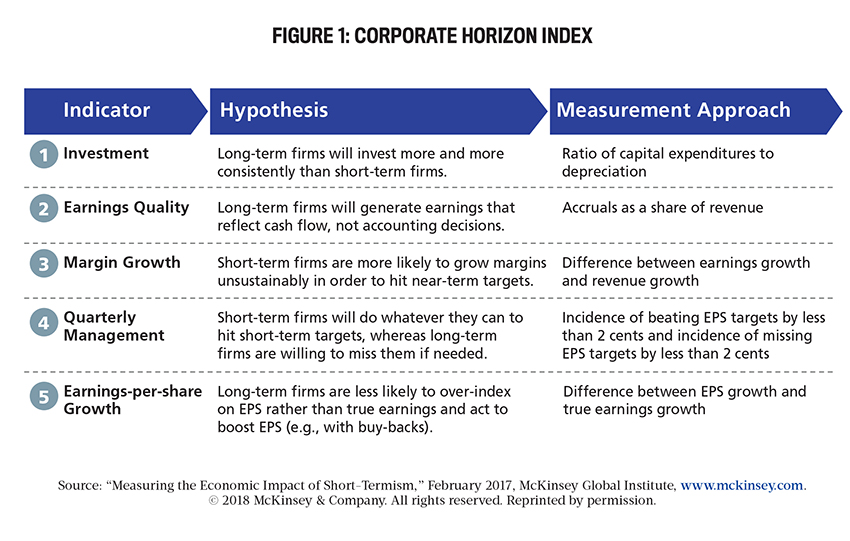

Frigo: In your Harvard Business Review article “Finally, Evidence That Managing for the Long Term Pays Off,” you discuss a Corporate Horizon Index that incorporates five financial indicators for identifying long-term value-creating companies. What are they?

Barton: To develop the Corporate Horizon Index, we identified five key financial indicators, selected because they matched up with five hypotheses we had developed about the ways in which long-term and short-term companies might differ (see “Measuring the Economic Impact of Short-Termism,” McKinsey Global Institute, February 2017). These indicators and hypotheses (see Figure 1) were:

- Investment: The ratio of capex [capital expenditure] to depreciation. We assume long-term companies will invest more and more consistently than other companies.

- Earnings quality. Accruals as a share of revenue. Our belief is that the earnings of long-term companies will rely less on accounting decisions and more on underlying cash flow than other companies.

- Margin growth. Difference between earnings growth and revenue growth. We assume that long-term companies are less likely to grow their margins unsustainably in order to hit near-term targets.

- Quarterly targeting. Incidence of beating or missing EPS targets by less than two cents. We assume long-term companies are more likely to miss earnings targets by small amounts (when they easily could have taken action to hit them) and less likely to hit earnings targets by small amounts (where doing so would divert resources from other business needs).

- Earnings growth. Difference between earnings-per-share (EPS) growth and true earnings growth. We hypothesize that long-term companies will focus less on things like Wall Street’s obsession with earnings per share, which can be influenced by actions such as share repurchases, and more on the absolute rise or fall of reported earnings.

Frigo: The financial indicators and underlying hypotheses reflected in the Corporate Horizon Index are consistent with the research on high-performance companies in the Center for Strategy, Execution and Valuation. We found that the high-performance companies we studied show a commitment to creating maximum long-term value, consistently reinvesting in the business and displaying a clear sense of purpose and attention to creating stakeholder value. Johnson & Johnson is a great example of having a clear purpose as articulated in its famous Credo, which has stood the test of time. The Credo was written in 1943 just before the company became publicly traded.

THE ADVANTAGES OF LONG-TERM VALUE CREATION

Frigo: Your work at McKinsey & Company and FCLTGlobal has studied the impact of short-termism and the advantages of long-term value creation. You have said that management teams need a “long lens” as well as a “short lens” for navigating today’s business environment. What are the advantages of focusing on long-term value creation for the company?

Barton: We found that companies deliver superior results when executives manage for long-term value creation. These companies resist the pressure from analysts and investors to focus excessively on meeting Wall Street’s quarterly earnings expectations. For example, companies such as Unilever, AT&T, and Amazon have succeeded by following a long-term view. Research led by a team from McKinsey Global Institute in cooperation with FCLTGlobal found that companies that operate with a true long-term mind-set have consistently outperformed their industry peers since 2001 across a broad spectrum of financial measures including revenues, earnings, profit, and market capitalization [see “Measuring the Economic Impact of Short-Termism,” McKinsey Global Institute, February 2017].

From 2001 to 2014, the long-term companies identified by our Corporate Horizon Index increased their revenue by 47% more than others in their industry groups and their earnings by 36% more, on average. In addition, their revenue growth was less volatile over this period. The long-term firms also appeared more willing to maintain their strategies during times of economic stress. During the 2008-2009 global financial crisis, they not only saw smaller declines in revenue and earnings but also continued to increase investments in research and development [R&D] while others cut back. From 2007 to 2014, their R&D spending grew at an annualized rate of 8.5%, greater than the 3.7% rate for other companies. In general, long-term companies have a clearer sense of purpose of why they are here and where they are going.

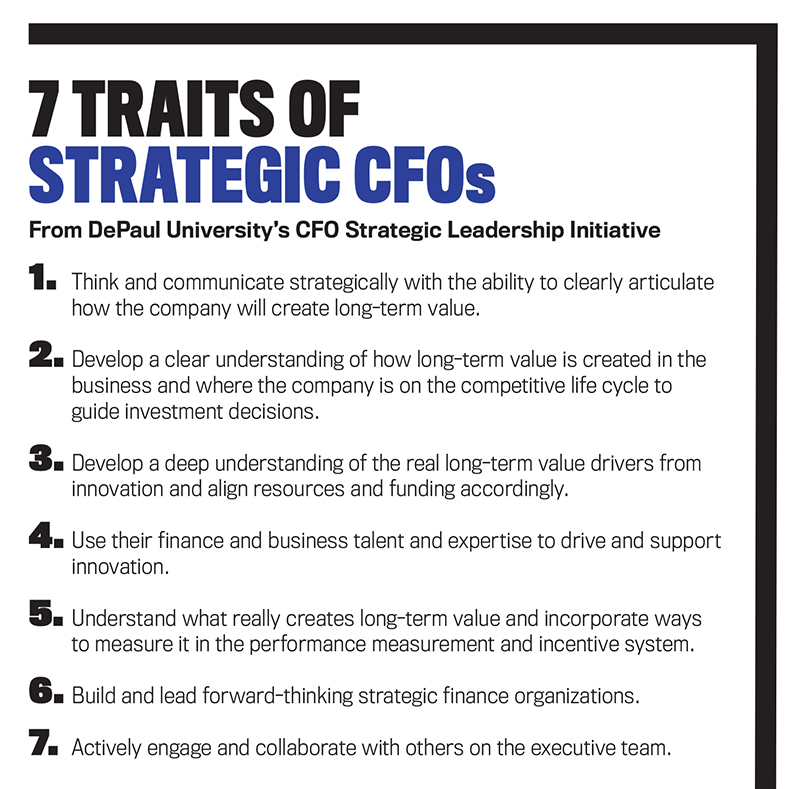

Frigo: CFOs and finance organizations can play a major role in ensuring that a company has the necessary long lens as well as short lens of performance measures and incentives to help it create long-term sustainable value. One of the traits of strategic CFOs is their ability to “Think and Communicate Strategically.” CFOs with this ability can make a clear connection between the strategies of the company, the investments in innovation, and how those strategies and investments will create long-term value. This trait is evident in the way CFOs communicate in earnings calls, investor presentations, and interviews.

The second trait is the ability to “Build and Lead Forward-Thinking Strategic Finance Organizations” with the capabilities and skills needed to enable long-term value creation and innovation. A third trait is the ability of the CFO to collaborate with others on the executive team, including the chief human resources officer (see “CFO + CHRO = Power Pair,” Strategic Finance, November 2015). Another trait, “Value-Creation Thinking,” is critically important and supports the other three traits. Strategic CFOs have the ability to manage the present while co-creating the future. Managing the present focuses on delivering offerings, whereas co-creating the future focuses on innovating offerings (see “Why Innovation Should Be Every CFO’s Top Priority,” Strategic Finance, October 2016).

PERFORMANCE MEASUREMENT AND INCENTIVES

Frigo: How can CFOs reflect long-term value creation in performance measurement? How can incentives in organizations be better aligned with creating sustainable long-term value?

Barton: Let me begin with incentives. There will never be a one-size-fits-all solution to the complex issue of incentive compensation. But companies should think about changing in three key areas.

First, they should link compensation to the fundamental drivers of long-term value, such as innovation and efficiency, not just to share price.

Second, they should extend the time frame for executive evaluations—for example, using rolling three-year performance evaluations or requiring five-year plans and tracking performance relative to plan. This would require an effective board that is engaged in strategy formation.

Third, they should create real downside risk for executives, perhaps by requiring them to put some skin in the game. For example, some experts we’ve surveyed have privately suggested mandating that new executives invest a year’s salary in the company and stay invested for a lock-up period after they exit the role. For performance measures, CFOs should consider how well the performance measures in their organizations are aligned with creating sustainable long-term value.

ECONOMIC PROFIT AND LONG-TERM VALUE CREATION

Frigo: Economic profit is a performance measure familiar to CFOs and finance organizations that some companies use for incentive compensation, decision making, and guiding strategic investment decisions. How have long-term value-creating companies performed in terms of economic profit vs. other companies?

Barton: One way to measure the value creation of long-term-focused companies is to look at the company through the lens of what is known as “economic profit.” Economic profit represents a company’s profit after subtracting a charge for the capital that the firm has invested (working capital, fixed assets, goodwill). The capital charge equals the amount of invested capital times the opportunity cost of capital—that is, the return that shareholders expect to earn from investing in companies with similar risk.

A company is creating value when its economic profit is positive and destroying value if its economic profit is negative. In our research with this metric, the gap between long-term companies and the rest showed a distinct difference. From 2001 to 2014, those managing for the long term cumulatively increased their economic profit by 63% more than the other companies. And by 2014, their annual economic profit was 81% larger than that of other companies, attributed to superior capital allocation that led to fundamental value creation [see “Measuring the Economic Impact of Short-Termism,” McKinsey Global Institute, February 2017].

BARRIERS TO LONG-TERM VALUE CREATION

Frigo: What barriers do management teams face in achieving long-term value creation, and what strategies would you recommend to overcome them?

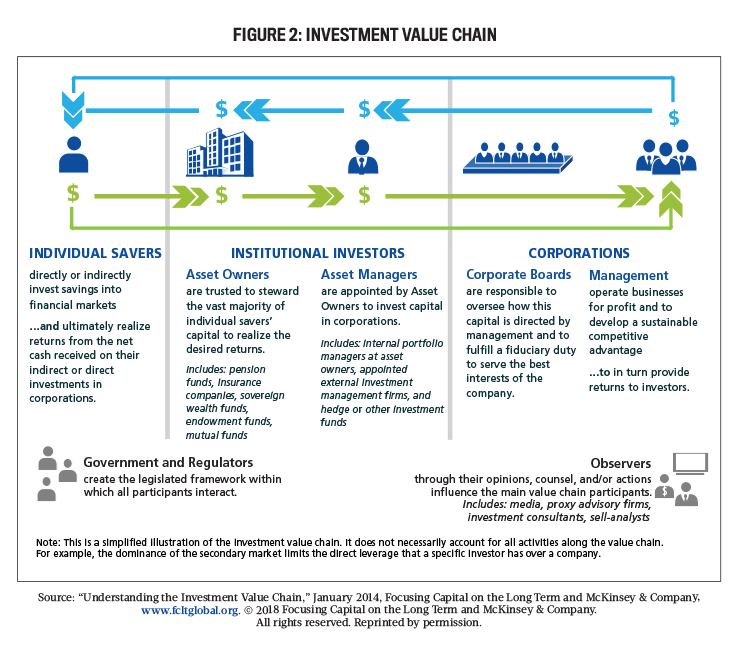

Barton: To break free of the tyranny of short-termism, we must start with those who provide capital. Taken together, pension funds, insurance companies, mutual funds, and sovereign wealth funds hold $65 trillion, or roughly 35% of the world’s financial assets. If these players focus too much attention on the short term, capitalism as a whole will, too. Institutional investors and corporate boards play key roles in the “investment value chain” (see Figure 2). They have the power and duty to act as champions of long-term thinking. This would in turn enable and encourage management teams of corporations to focus on long-term value creation.

Frigo: The investment value chain shows the important role of management to operate the business for profit and develop sustainable competitive advantage as a guiding force for the company’s strategy and its execution. This is where CFOs and financial organizations can play a key role in the virtuous circle of long-term value creation.

ACTING LIKE AN OWNER UNDER ACTIVIST PRESSURE

Frigo: During the 2018 Focusing Capital on the Long Term Summit, you moderated a panel on shareholder activism that identified a number of actionable solutions for companies. Would you describe those?

Barton: One very important action is related to defining and clearly communicating the purpose of the company, especially to investors but also to employees and other stakeholders. Some companies, such as Unilever, have also stopped giving quarterly guidance. Investor communications should also emphasize long-term “health” metrics—for example, innovation rate, quality of talent or organizational health, reputation, etc. Some examples of organizations who have done this include SAP and Westpac. Investor activities should also focus time on long-term shareholders. Long-term value creators should consider ideas such as the United Nations Sustainable Development Goals (SDGs) and ensure board members have relevant industry knowledge, diverse expertise, and a proclivity for thinking independently in both “peace time and war.”

Frigo: CFOs and finance organizations have a great opportunity to lead the process of making the SDGs happen and connect performance with purpose. Given their financial expertise and positioning with organizations, they can contribute significantly to identifying, executing, and monitoring business decisions and strategies for long-term sustainable value creation (see “Sustainable Development Goals: Integrating Sustainability Initiatives with Long-Term Value Creation,” Strategic Finance, September 2017). Integrated reporting is also an area where CFOs and finance organizations can play a valuable role in terms of communicating how companies create long-term sustainable value (see “Leading Practices in Integrated Reporting,” Strategic Finance, September 2014).

TALENT AND LONG-TERM VALUE CREATION

Frigo: In your latest book, Talent Wins: The New Playbook for Putting People First, coauthored with Ram Charan and Dennis Carey, what key takeaways and examples would be most valuable to CFOs and management teams in achieving long-term value creation?

Barton: The talent-driven organization needs a central brain trust, and all that we’ve seen argues for it being at least a “G-3” consisting of the CEO, CFO, and chief human resources officer (CHRO). Why these three executives in particular? Because deploying financial capital and human capital together is key to success. “People allocation is as powerful as financial allocation,” explains Aon CEO Greg Case, who works closely with CHRO Tony Goland and CFO Christa Davies to make sure the company has the right talent to meet the challenges of the future. By putting talent and finance on equal footing, the G-3 will change the way and sequence in which critical matters are discussed [see “An agenda for the talent-first CEO,” McKinsey & Company, March 2018].

Executives also need to ask some key questions, such as: Are my company’s talent practices still relevant? How can we recruit, deploy, and develop people to deliver greater value to customers—and do so better than the competition? The experiences of CEOs at talent-driven companies such as Amgen, Aon, Apple, BlackRock, Blackstone, Google, Haier, Shiseido, Tata Communications, and Telenor suggest that meeting those challenges requires a distinct set of mind-sets. As we show in the book, leaders at talent-driven companies are as focused on talent as they are on strategy and finance. They make talent considerations an integral part of every major strategic decision.

MAKING THE SHIFT FROM SHORT-TERMISM TO LONG-TERM VALUE CREATION

Frigo: What do companies need to do to make a shift from short-termism to long-term value creation?

Barton: For a company to make the shift from short-termism to long-term value creation, there are three important elements to consider. First, business and finance need to redesign incentives and structures to focus or orient their organizations on the long term. This means measuring long-term value creation and performance relative to metrics from the company’s long-term strategy. For example, this could mean establishing reporting metrics that reflect the company’s model for value creation, identifying value drivers and metrics for each reporting unit, and reporting on these consistently.

Second, executives must infuse their organizations with the perspective that serving the interests of all major stakeholders (employees, suppliers, customers, creditors, communities, as well as the environment) is not at odds with the goal of maximizing corporate value; rather, it’s essential to achieving that goal. This means communication with their entire organization from the front line to the chairman of the board.

Third, public companies must cure the ills stemming from dispersed and disengaged ownership by bolstering the boards’ ability to “govern like owners.” Senior management will not be able to make this shift alone; they must engage their investors and their board to embrace a longer-term mind-set through communications and transparency. This involves identifying who the long-term investors are and rebalancing investor engagement to those key stakeholders. An example of a company doing this is Amgen, which, in 2011, outlined the company’s long-term strategy and gave financial guidance four years ahead with a clear capital-allocation plan.

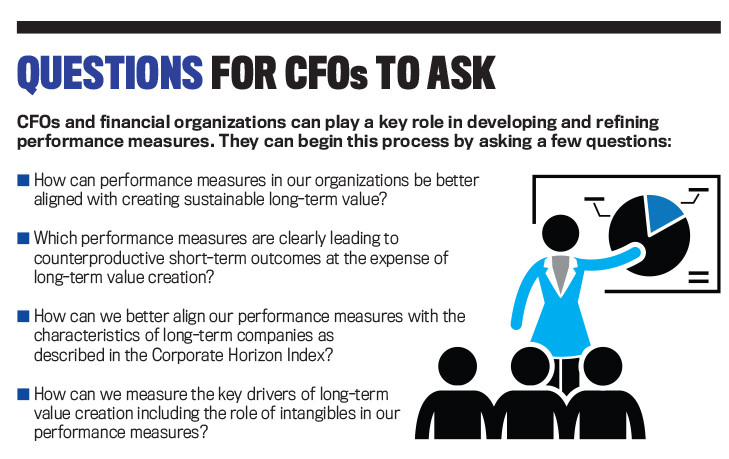

Frigo: CFOs and finance organizations can take a leadership role in reorienting performance measures, incentives, and structures toward the long term, the first element mentioned (see “Questions for CFOs to Ask”). Serving the interests of all major stakeholders as being essential to achieving the goal of maximizing corporate value can guide CFOs and financial organizations as they consider how performance measures and incentives can be better aligned with long-term value creation, the second element. And for the third element, CFOs have the opportunity to develop the type of information boards need to “govern like owners” and use this philosophy as a roadmap for developing strategic performance measures for the organization. This can include focusing performance measures on long-term sustainable return on investment and disciplined reinvestment in the business.

MOVING FORWARD WITH LONG-TERM VALUE CREATION

CFOs and finance organizations have a great opportunity to play a vital role in helping organizations create greater long-term sustainable value. A key first step is to develop a clear understanding of the business strategy and how long-term value is created in your business through innovation and deployment of resources. Develop the ability to articulate clearly how the company intends to create long-term value and long-term value drivers from innovation. Companies need to innovate at an increasingly rapid pace in order to survive and thrive in today’s environment. Use your finance and business expertise to drive and support innovation that will enable your organization to achieve greater long-term value creation. Understand what really creates long-term value in your organization, and develop ways to measure it and manage it. A long-term approach to measuring success is key.

This article begins a series of articles on strategic management and management accounting focused on “Creating Greater Long-Term Value” that will examine how leading practices and ideas in strategic management can help CFOs, finance organizations, and management accountants create greater value. This series will include insights from top business leaders and thought leaders who will share their ideas and perspectives regarding how companies can create long-term sustainable value.

To Learn More

The answers in this interview may reference materials from previously published articles listed here:

Dominic Barton, “Capitalism for the Long Term,” Harvard Business Review, March 2011.

Dominic Barton and Mark Wiseman, “Focusing Capital on the Long Term,” Harvard Business Review, January-February 2014.

Dominic Barton, Jonathan Bailey, and Joshua Zoffer, “Rising to the Challenge of Short-Termism,” FCLTGlobal, 2016.

Dominic Barton, James Manyika, and Sarah Keohane Williamson, “Finally, Evidence That Managing for the Long Term Pays Off,” Harvard Business Review, February 2017.

Dominic Barton, James Manyika, Timothy Koller, Robert Palter, Jonathan Godsall, and Joshua Zoffer,“Measuring the Economic Impact of Short-Termism,” McKinsey Global Institute, February 2017.

FCLTGlobal, “Summary Report: 2018 Focusing Capital on the Long Term Summit,” February 2018.

Dominic Barton, Dennis Carey, and Ram Charan, “An agenda for the talent-first CEO,” McKinsey Quarterly, McKinsey & Company, March 2018.

October 2018