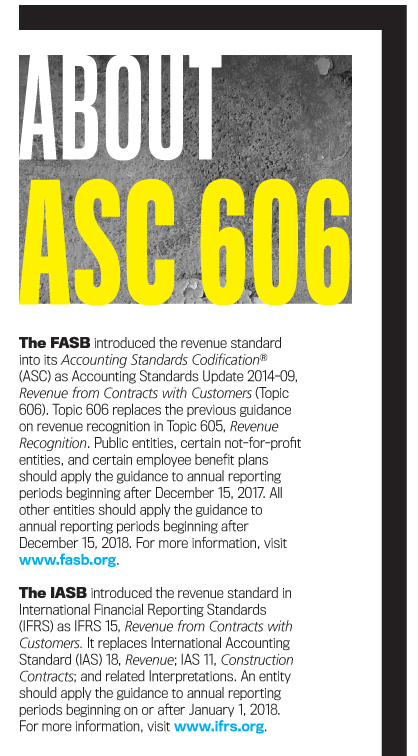

As you know, on May 28, 2014, the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) together issued a converged standard about recognition of revenue from contracts with customers. Known as ASC 606, Revenue from Contracts with Customers, the standard will improve the financial reporting of revenue and improve comparability of the top line in financial statements globally, the Boards say. Under the new revenue reporting regulations, which would establish a common revenue standard for U.S. Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), an entity will have to implement the following five steps:

- Identify the contract(s) with a customer.

- Identify the performance obligations in the contract.

- Determine the transaction price.

- Allocate the transaction price to the performance obligations in the contract.

- Recognize revenue when (or as) the entity satisfies a performance obligation.

These changes will affect every organization, though to what exact extent will differ on a company-by-company basis. Despite the fact that accounting and finance professionals are aware of ASC 606 and its implications in terms of organizational change, what’s surprising from our point of view is how blasé some organizations, particularly those in the private sector, have been about this matter.

Granted, with the Sarbanes-Oxley Act of 2002 (SOX) and the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, there have been a lot of regulatory changes in the past 10 to 15 years, so a certain amount of organizational fatigue is to be expected. Nevertheless, timely, accurate revenue reporting is critical to compliant operations. That means that even with the recently announced deferral of ASC 606 implementation to December 2017 for public entities and 2018 for nonpublic organizations, it’s crucial to start preparing for the upcoming changes. And that involves not only assessing each contract and revenue stream but ensuring that the right talent is in the right place to implement the necessary adjustments while still maintaining the company’s day-to-day operations. Consequently, organizations that aren’t yet preparing for the transition are putting themselves at a disadvantage in terms of acquiring the talent necessary for the change.

DÉJÀ VU?

If your organization is a vendor, ASC 606 will likely impact you in a number of areas—both inside and outside the accounting department—including contracts with customers (plus those with product warranties and returns), bonus plans, expenses, taxes, IT, internal controls, and investor relations. If your company is a customer, you may see changes in how vendors propose contracts or sell products or services to you.

Especially for vendors, multiple departments will be affected, including Accounting and Finance, Internal Audit, Human Resources, Sales and Marketing, Legal, IT, and Operations. Policies and processes will need to be updated, data management will need to be adapted, reporting methods and control will need to be modified, and employees will need to be educated about the changes and how to adhere to the new regulations.

Clearly, all of this will involve change at the organizational level. Yet while the changes are spelled out and the steps are established, companies will still need to use their best judgment in implementing the principles-based approach for determining revenue recognition for their own unique structures. At the same time, it’s important to realize that this required change also presents the perfect opportunity to streamline and optimize methods.

Sound familiar? It should, since we’ve been in this type of situation before.

In 2002, when organizations were required to adapt internal controls to comply with SOX, many companies struggled to implement the necessary changes on time. In fact, according to Paulette Chu in her May 18, 2005, JournalStar.com article, “Delayed corporate filings show effects of Sarbanes- Oxley,” hundreds of organizations didn’t file their annual reports on time for the 2004 deadline. Moreover, an estimated 77 companies, each with revenue of more than $100 million, missed the 2005 deadline for filing quarterly reports, citing ongoing work on their internal controls as well as financial restatements.

How did this happen?

To a large extent, it was because of a low supply of skilled talent combined with misconceptions about how that talent wanted to work. At the time, it became clear that many employers simply assumed the right people would be available—despite widespread warnings to the contrary. Moreover, the general notion was that companies could bring in external consultants to manage the change. There was also a distinct preference for talent with Big 4 experience since the brand recognition stands for quality, safety, and minimized risk.

A SHORTAGE IN THE PRIVATE SECTOR

Unfortunately, though there were many professionals in the Big 4 and other public accounting firms with the necessary expertise pertaining to internal controls, the availability of professionals for the private sector was severely limited—especially because demand suddenly spiked.

To complicate matters, many of those who were available were looking for permanent positions. As a result, a huge market developed for permanent finance and accounting talent with internal controls experience. Additionally, the demand for auxiliary talent to fill lower-level positions increased.

With numerous organizations competing for talent, many were late to start implementing the necessary changes. The ripple effect continued through companies that not only had to implement the changes but also update roles and responsibilities as well as educate the existing workforce about the changes—an area that companies didn’t factor in sufficiently for such a far-reaching regulatory requirement.

The intense scrambling within companies to implement SOX produced a number of clear lessons that may repeat themselves with ASC 606:

- Organizations need to start preparing for change in a timely manner.

- Talent might not be available in all locations or labor categories and may have expectations that don’t match organizational needs.

- High demand for talent is likely to drive up costs.

- Increasingly, more quality professionals aren’t represented by the Big 4’s banners and instead form their own brands as independent contractors and freelancers.

- Provisions need to be made to educate those parts of the workforce that are affected by the change.

As an example, at our own company, Kelly Services, we initiated a three-year change management project to make the adjustment to comply with SOX. Project management consisted of a combination of experienced Kelly talent and select experienced outside vendors, both of whom coordinated the tactical work. Additionally, we brought in talent to perform support roles under the guidance of project management, allowing the core strategic team to focus on the process management changes. Thanks to this clear focus on change management and timely preparation, we were able to adapt our internal controls and adjust our processes in an appropriate and compliant manner.

LOTS OF MOVING PARTS

As we’ve seen, ASC 606 will affect organizations in a number of critical areas—ranging from accounting to contracts to marketing—across a variety of departments, including Accounting, Legal, IT, and Operations. In order to effectively make the necessary adaptations, organizations will have to initiate change management swiftly and accurately, then consistently adjust processes and procedures across the various departments.

Effective change management begins with establishing an “Impact Analysis” team that can in part consist of contracted accounting, operations, legal, IT, and HR talent. In some cases, depending on the complexity of the organization, it may make sense to include internal talent who know the organization through and through. If that’s the route your company chooses, you may need to hire additional people to cover their duties while they’re performing the impact analysis. The impact analysis team should work to gain an overview of the current state of your organization—and the desired future state—to determine how strategy will be impacted. Items to consider include:

- The state of your systems and controls. Will they be able to support the changes to process and reporting?

- Talent mix. What types of talent will you need to work on the implementation? Do you have them on staff, or do you need to supplement with additional talent?

- Daily operations. Who will handle the work of those core team members who are reassigned to work on implementation?

Assuming the organization has an integrated strategy that optimizes each department’s functions to support overall business objectives, it’s logical that revenue reporting changes will have tactical consequences. This means that roles and responsibilities are likely to change. Performing an in-depth impact analysis will clarify where and how these changes need to take place in terms of policies, processes, data, and reporting.

Next, the impact analysis team must secure support from internal stakeholders who can help drive the necessary actions throughout the organization—as well as let people know what sort of negative things could happen if there are delays. In any event, it’s crucial to understand that, regardless of whether the impact analysis identifies a material change or a responsibility to ensure the company is aware of its exposure, the assessment itself, as well as adopting the five steps identified earlier, most likely will be material. Therefore, it’s advisable to get out in front of the change instead of acting too slowly and risking compliance issues and penalties.

MEASURING THE DEGREE OF CHANGE

Determining how to effect the changes identified by the impact analysis team will be different for each organization, depending on the availability of talent and the budget. Here’s what should be taken into account:

- Is there talent in-house to set up a Project Management Office (PMO) to manage the change, or does external talent need to be brought in?

- If appropriate, is there access to talent with global knowledge?

- If in-house talent will spearhead the change management, will external talent need to be brought in to “backfill” positions?

- If external talent needs to be brought in, will this be in the form of consultants and independent contractors, temporary full-time hires for the duration of the transition, or, because there’s a lack of supply in permanent roles, direct hires?

- If external talent will be utilized, will the complexity of the organization impact their ability and time required to determine the gaps and subsequent impact?

- Will external support personnel need to be hired to assist the core team with the transition?

- What is the availability of talent in terms of proximity and labor category?

- What is the budget for the acquisition of talent?

- Will the workforce be trained in the new processes and procedures by external consultants or by an in-house team?

Some of the problems companies might encounter are similar to those they grappled with when adopting SOX. Accounting talent is becoming scarce because of stringent education requirements and the Big 4’s highly aggressive recruitment practices. As a result, accounting talent with the expertise to oversee this type of change is in very high demand. Many professionals with the right skills are senior talent who are currently transitioning from employment with the Big 4 to retirement but who aren’t yet ready to leave the industry completely. It’s highly likely that they will form the backbone of the change management teams on a part-time, consulting basis. But will this be enough to handle the growing demand?

Of course, organizations will need other types of talent as well. Legal talent will be in high demand to assess and adapt contracts, operations talent will be needed to implement changes, and IT talent will have to modify systems and data.

As a result of the high demand, companies need to remain open to sourcing talent from a variety of categories and to consider a full continuum of workforce models.

TIME TO PARTNER?

Transitioning to ASC 606 is likely to be a labor-intensive, drawn-out, and costly process for many organizations. To complicate matters, day-to-day operations need to continue without interruption in order for a company to remain competitive. Consequently, with many operations being very lean today, there’s a risk of shortchanging either one, or both, of these focus areas.

This is where collaborating with a workforce solutions partner that has extensive experience in change management can be helpful. A workforce solutions partner can assist with everything from contract or consulting talent to supply chain management, recruitment process outsourcing, or complete change management. It can advise your company regarding the talent strategy that makes the most sense for the organization, utilizing existing resources where possible and looking for the most cost-effective ways to bring in additional talent. Moreover, when it comes to hiring external talent to handle sensitive financial and IP data, a workforce solutions company can help mitigate risk because of its access to previously vetted, proven, trustworthy talent.

WHAT IT WILL COST

The costs associated with change management will vary per organization. Clearly, companies with a wide range of products, services, or nonstandard contracts will have to assess and adjust each one at every level. Moreover, organization-wide changes will have to be made—from policies and processes to data recording and staff training. The budget for these costs will depend on the overall amount of change needed, as indicated by the impact analysis.

How organizations implement change will also influence costs. For example, companies that have in-house talent capable of managing the change won’t have to budget for external consultants. Yet private contractors may be worth the investment if they’re more experienced and better equipped to optimize certain key processes.

Similarly, organizations that bring in talent to “backfill” positions could be driving up costs if they offer this talent full-time, direct-hire positions without taking into account that they’ll be scaling back this sector of their workforce once the transition is complete. Instead, contingent talent—temporary at first, with the option to bring them on full-time if necessary—would be a more appropriate solution.

When it comes to keeping costs down, timing is also a key factor. Wait too long to attract talent in a highly competitive market, and you might find these people in a much stronger position to negotiate higher pay, better benefits, and more perks.

Partnering with a workforce solutions company can help keep a lid on costs, particularly when it comes to streamlining the talent supply chain and ensuring that the right people are in the right places. With in-depth knowledge of where the talent is, what they want, and how to attract them, it’s more feasible to control costs. At the same time, when it comes to change management, an experienced workforce solutions company can help establish a lean project management team and ensure cost-effective change processes.

It’s vitally important for companies to be compliant with all regulations and reporting requirements. By assessing which processes must be changed, how the changes need to be implemented, and what workforce strategy will be most effective (and cost effective), forward-thinking companies can prepare their organizations properly so that the actual implementation of ASC 606 changes is as smooth and successful as possible.

November 2015